Set Up a Self Directed IRA LLC With Checkbook Control | A 7-step guide for real estate, crypto, and precious metals investors

TL;DR

A self directed IRA LLC with checkbook control is an IRA owned LLC that gives the account holder direct control over a business checking account funded by retirement savings. The individual retirement account owns 100% of the limited liability company, you act as the manager llc role without compensation, and you sign every check or wire to buy real estate, hold bitcoin, fund private notes, or buy precious metals. Setup runs around $1,000-$1,500 in one-time legal and setup fees plus state filing fees, takes 2-6 weeks, and is legal under Swanson v. Commissioner (1996), Field Service Advisory 200128011, and Ellis v. Commissioner (2013). The structure usually pays for itself once your IRA balance is above $50,000 and you plan more than two or three ira investments per year.

____________________________________________________________

How to set up a self directed IRA LLC with checkbook control

To set up a self directed IRA LLC with checkbook control, you open a self directed IRA with a passive custodian, form a single member LLC with the IRA listed as the sole member, draft an operating agreement that names you as the non-compensated manager, get an EIN from the IRS, open an LLC bank account, and have your custodian wire IRA funds into that business checking account so you can write checks without asking the custodian first.

What you need before you set up a self directed IRA LLC with checkbook control

You need a funded self directed IRA, a single member LLC structured for IRA ownership, an operating agreement with custodian-approved language, an EIN from the IRS, and a business checking account at a bank that accepts ira owned llc deposits.

Most account owners come in already holding a traditional IRA, Roth IRA, or SEP IRA at a brokerage that only lets them buy stocks and mutual funds. To use the checkbook control IRA structure, you have to move those retirement funds to a self directed ira custodian who allows self directed iras to own an llc ira structure. Mainstream brokerages will not. The custodian becomes a passive custodian, meaning they hold the IRA on the books but every investment decision passes through your llc bank account instead of their compliance desk.

You also need to decide which type of IRA you are converting. A traditional self directed IRA grows tax-deferred. A Roth IRA grows tax free. The setup process is the same either way; the tax treatment is what changes when you eventually take distributions. A SEP-IRA works too if you have self employment income.

If you live in a state with high franchise taxes (California’s $800 minimum is the most common pain point), you can form the LLC in a friendlier state like Wyoming or New Mexico. The LLC just has to be valid in the state where it is registered. Some real estate investors form the llc set up in the state where the real estate sits. There is no single right answer. The choice affects your annual cost, not your investment options.

Annual contributions still follow the regular rules. The current limits are published on the IRS site under retirement topics — IRA contribution limits. Whatever you contribute lands in the IRA at the custodian first, then moves into the llc bank account through a buy direction letter.

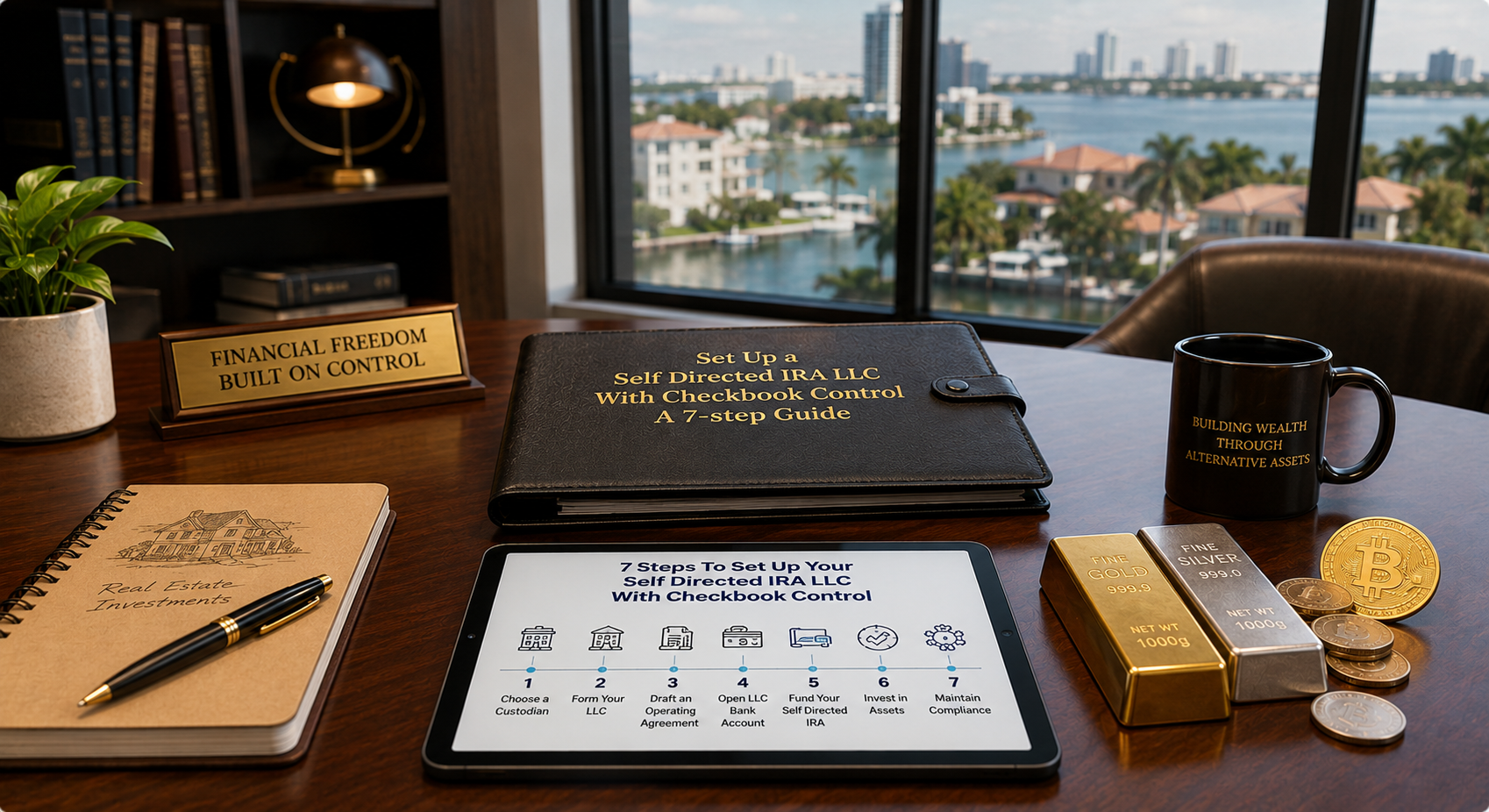

The 7 steps to set up a self directed IRA LLC with checkbook control

The seven steps to set up a self directed IRA LLC with checkbook control are: open the self directed IRA, fund it, form the LLC, draft the operating agreement, get the EIN, open the LLC’s business checking account, and submit the buy direction letter that wires retirement funds from the custodian into the LLC bank.

Step 1 — Open the self directed IRA

Apply with a directed ira custodian that handles ira owned llc structures. The application asks for your account name, beneficiaries, and the source of funds. Approval usually clears in one or two business days. The IRA itself is opened in your name, but the title format that matters later reads “[Custodian Name] FBO [Your Name] IRA #”. That exact wording goes on every ownership document for assets the LLC eventually buys.

Step 2 — Fund the IRA

Money lands in the new ira account through one of three paths: a direct transfer from another self directed ira (or a brokerage IRA), a rollover from a 401(k), 403(b), or other employer plan, or a fresh annual contribution within IRS limits.

- Direct transfer (cleanest). The current custodian wires funds directly to the new ira custodian. Nothing is reported as a distribution. No 1099-R, no 60-day window. Most ira investors choose this method.

- 60-day rollover. The old custodian sends a check to you, and you have 60 days to redeposit it with the new custodian. The IRS will allow only one indirect rollover per 12-month period across all your individual retirement accounts. Miss the 60-day window and the entire amount counts as a taxable distribution.

- Annual contribution. New money up to the IRS annual limit goes to the IRA, not directly into the llc bank account. (See the rules in step 3 of the legal section below — annual contributions are paid to the IRA itself, then moved to the LLC by buy direction letter.)

Your IRA will need enough cash to cover the LLC formation expenses and the deal you plan to make. A common setup mistake is funding the IRA with too little, then having to wait weeks for a second transfer. Send more than you think you need. Idle cash sitting in the LLC bank account is fine; an empty account when a closing date hits is not.

Step 3 — Form the single member LLC

File Articles of Organization with the secretary of state in your chosen state. The application typically lists you as the organizer and a registered agent for service of process. The LLC must be a single member llc, with the IRA listed as the sole owner — not you personally. The member field on the filing reads, again, “[Custodian Name] FBO [Your Name] IRA #”.

Many ira llc facilitators and a law group or two (Bergman Law Group, KKOS Lawyers, Mountain West IRA, IRA Financial Group, IRA Services Trust Company among others) handle this filing as part of their package, which is why their flat fees usually include state filing costs. If you are doing this without help, file directly through the secretary of state’s online portal.

Which state to file in. The LLC does not have to be formed in your home state. Most checkbook ira llc structures get filed in one of four places:

| State | Filing fee | Annual report / fee | Franchise tax | Notes |

| Wyoming | $100 | $60 minimum | None | Strong privacy, low ongoing cost, popular for crypto and private notes |

| New Mexico | $50 | None | None | Cheapest long-term, no annual report, common for passive holdings |

| Nevada | $75 | $200 list of officers + $200 business license | None | Higher annual cost than WY/NM, less common |

| Home state | varies $50-$500 | varies | varies (CA $800/yr) | Required if the LLC will buy real estate sitting in that state |

If the IRA llc is going to invest real estate inside one specific state, most attorneys recommend forming the LLC in that state to avoid a foreign LLC registration. For purely financial assets (crypto, notes, mutual funds proxies, precious metals at a depository), Wyoming or New Mexico is usually the cheapest answer per year.

Step 4 — Draft an IRA-compliant operating agreement

A standard limited liability company operating agreement will not work here. The operating agreement has to do five specific things:

- Acknowledge the IRA as the sole member of the llc legal entity.

- Restrict the manager (you) from receiving compensation.

- Prohibit any transactions with disqualified persons.

- Reference the prohibited transaction rules in Internal Revenue Code Section 4975.

- Authorize the manager to sign on behalf of the LLC.

Most self directed ira custodians will require this language in writing before they release any funds. Generic templates from incorporation websites do not include it. This is the single biggest reason people use a facilitator or attorney instead of building the llc trust paperwork themselves.

Step 5 — Get an EIN for your IRA LLC from the IRS

Apply for the EIN online at the IRS website. The form takes about ten minutes. The applicant is the IRA llc, the responsible party is you as the manager, and the type of entity is “Limited Liability Company”. On the question of how many members, you select “single-member LLC” and indicate the LLC is owned by a tax-exempt organization (the IRA).

Save the EIN confirmation letter (Form CP 575). The bank will ask for it in step 6, and most ira custodians will also want a copy for their files.

Step 6 — Open the LLC bank account

Walk into a bank with the Articles of Organization, the operating agreement, the EIN letter, and a copy of the IRA documents. Some banks understand the ira owned llc immediately. Others do not, and you will spend an hour explaining why the LLC is owned by an IRA and not by you personally.

Banks that regularly open checkbook ira llc accounts include Solera National Bank, Titan Bank, and a handful of credit unions and community banks. Bring extra copies of the operating agreement; the banker often has to send pages to compliance for review. A few rules that banks sometimes miss:

- The business checking account must be in the LLC’s name, not yours.

- The first deposit must come directly from the custodian’s wire, not from your personal checking account.

- The signature card lists you as manager, not as owner.

A funded business checking account at the end of this step means you officially have checkbook control.

Step 7 — Submit the buy direction letter

The buy direction letter is the form your self directed ira custodian uses to wire retirement funds from the IRA into the LLC’s checking account. It identifies the LLC’s name, EIN, bank, and the dollar amount being moved. Once the wire clears, the IRA’s cash is sitting in the llc bank account and you can write checks against it.

From this point on, every check, wire, and signed contract is your decision. The custodian’s role drops to a passive role of reporting the IRA’s value once a year to the IRS. You can now invest in real estate, fund a private note, hold bitcoin, or buy precious metals at a bullion dealer who can wire-receive payment in the LLC’s name.

How title should be held on assets your IRA LLC buys

Every asset the IRA llc buys must be titled in the LLC’s name, never in your personal name and never in the IRA’s name directly. The deed, the title, the brokerage account, the crypto exchange account, and the bullion depository ledger all read the same way: the LLC’s full legal name (often “[Your Name] IRA, LLC”) followed by the EIN.

The IRA itself is held one level above. On the custodian’s books, the IRA is titled as “[Custodian Name] FBO [Your Name] IRA #”. That title appears on the buy direction letter when funds move from the custodian to the LLC bank, and on the LLC’s operating agreement where the IRA is listed as the sole member. You will not see “FBO” on a property deed or on a crypto exchange — those documents show the LLC as the legal owner. The chain is: custodian holds the IRA, IRA owns the LLC, LLC owns the asset.

Common titling mistakes that disqualify a checkbook control ira:

- Buying real estate in your personal name and trying to “transfer it later” to the LLC.

- Putting your spouse’s name on a deed jointly with the LLC.

- Opening an exchange account in your personal name and depositing IRA funds.

- Mailing settlement checks to your home address instead of the LLC’s registered address.

If the title is wrong, the IRS treats the purchase as a personal use of IRA funds, and the entire ira llc structure can be treated as distributed. Fix titles before any transaction closes, not after.

How much does it cost to set up a self directed IRA LLC with checkbook control?

Setting up a self directed IRA LLC with checkbook control costs roughly $1,000 to $1,500 in one-time setup fees, plus state filing fees of $50-$500, plus annual fees of $300-$700 per year combining custodian fees, registered agent fees, and any state franchise tax.

Here is a realistic cost breakdown using published 2025-2026 fee schedules from the major ira llc facilitators:

| Cost component | One-time | Annual |

| Custodian setup | $50-$100 | — |

| LLC formation (facilitator or attorney) | $800-$1,495 | — |

| State filing (Articles of Organization) | $50-$500 | — |

| Registered agent | included or $125 | $125 |

| Custodian flat fee | — | $150-$400 |

| State franchise tax | — | $0-$800 |

| Bank account fees | $0-$50 | $0-$120 |

The annual fees stay flat regardless of how much your IRA grows. That is the structural reason the checkbook control llc pays off over time — a passive custodian charging a fixed amount per year does not scale with your account balance, while a non-checkbook ira custodian usually charges based on assets under custody and adds transaction fees on every wire. By year three or four, the ira llc structure usually costs less than a standard self directed IRA on the same balance.

The fees are paid from the IRA, not from your personal funds. The IRS treats fees paid from personal funds for IRA assets as additional contributions, which can blow your annual contribution cap. Pay every IRA-related invoice directly from the LLC bank account.

Rules that keep your checkbook control IRA LLC legal

The rules that keep a checkbook control IRA LLC legal are the prohibited transaction rules in Internal Revenue Code Section 4975, which forbid any deal between the ira llc and a disqualified person, any compensation to the IRA owner from the LLC, and any personal benefit from the LLC’s assets.

A disqualified person includes you, your spouse, your parents, your grandparents, your children, your grandchildren, and any business in which any of these people own 50% or more. Siblings and cousins are generally not disqualified persons. The full rule is at 26 U.S. Code § 4975, and the IRS has a plain-language summary on retirement topics — prohibited transactions.

Three rulings established the legal foundation for the structure:

- Swanson v. Commissioner (1996) — the Tax Court ruled an IRA can form and fund a corporation without triggering a prohibited transaction.

- Field Service Advisory 200128011 (2001) — the IRS confirmed that an IRA-owned entity is permitted as long as the IRA owner does not personally benefit.

- Ellis v. Commissioner (T.C. Memo 2013-245) — the court confirmed forming the LLC was fine, but ruled it was a prohibited transaction for the LLC to pay Mr. Ellis a salary. His entire IRA was disqualified and treated as a distribution.

The Ellis case is the one to remember. You can buy real estate, hold bitcoin, fund private loans, or buy precious metals through your IRA llc. You cannot pay yourself, live in IRA-owned property, vacation in it, or use it for a single weekend. You cannot store IRA-owned gold silver coins at home (the McNulty case in 2021 reinforced this point on home-stored metals). You cannot run a side business out of an IRA-owned property where you draw self employment income. If the LLC’s investments produce unrelated business income above $1,000 per year, the ira llc files Form 990-T and pays UBIT on it. UBIT is a separate concern from prohibited transactions, but easy to forget.

A short list of the most common prohibited transactions in a checkbook control ira:

- Paying yourself or any disqualified person a fee or salary from the LLC.

- Buying property from a disqualified person.

- Selling property to a disqualified person.

- Lending IRA funds to a disqualified person.

- Personally guaranteeing a loan made to the LLC.

- Using IRA-owned property personally, even briefly.

The penalty for any of these is severe. The IRS treats the entire IRA as distributed on January 1 of the year the violation happened, with full income tax owed plus a 10% early withdrawal penalty if you are under 59½. There is no fix once the distribution lands on your record.

Common mistakes when you set up a checkbook control IRA LLC

Most disqualifications do not come from exotic transactions. They come from setup errors made in the first thirty days. The mistakes below cost real ira investors their tax-advantaged status:

- Using a generic LLC operating agreement. A standard limited liability company llc template will not include the Section 4975 language or the manager-non-compensation clause that the custodian needs. The check book ira will not fund without it.

- Listing yourself as the LLC owner instead of the IRA. The Articles of Organization must show “[Custodian Name] FBO [Your Name] IRA #” as the member. If your name appears as owner on the state filing, the entire structure is broken from day one.

- Commingling personal funds. Depositing your own money into the LLC bank account, even to “front” a closing, is a prohibited transaction. The same goes for paying LLC bills with a personal credit card and reimbursing yourself.

- Wiring funds to the LLC before the operating agreement is signed. The custodian needs the signed agreement on file before the buy direction letter clears. Skipping this step leaves the wire in limbo.

- Forgetting the EIN type on the IRS form. When you apply for the EIN, select “owned by a tax-exempt organization.” Selecting the wrong entity type means you may have to file for a corrected EIN later.

- Opening the bank account in your personal name “to make it easier.” A few banks will let you do this. Doing it disqualifies the IRA. The business checking account name has to match the LLC exactly.

- Forgetting the BOI report. Most LLCs filed in 2024 onward have to file a Beneficial Ownership Information report with FinCEN. Whether IRA-owned LLCs are exempt has gone through several court rulings; ask your custodian or attorney about the current rule for your state and filing date.

- Acting as a paid manager. You can use the LLC’s checkbook to direct investments. You cannot pay yourself for that work. Ellis v. Commissioner is the cautionary tale.

How long does the whole setup take?

A typical self directed IRA LLC with checkbook control takes 2-6 weeks from application to a funded business checking account. Custodian onboarding takes a few business days. IRA funding takes 5-15 business days depending on your old custodian. LLC formation takes 1-3 weeks depending on the state. EIN approval is same day. Bank account opening takes 1-2 weeks once the EIN letter arrives.

You can compress this timeline. Some directed ira custodians offer expedited filings that finish the LLC formation in a week. The slowest piece is almost always the IRA funding step, since old brokerages take their time releasing cash for a transfer to a new custodian.

Key takeaways

- A self directed IRA LLC with checkbook control is an ira owned llc where the ira holder serves as the unpaid manager of a limited liability company and signs checks directly from an LLC bank account.

- The structure is supported by Swanson v. Commissioner (1996), FSA 200128011 (2001), and Ellis v. Commissioner (2013), all confirming the IRA can own and fund an llc legal entity as long as Section 4975 prohibited transaction rules are followed.

- Setup takes 2-6 weeks and costs roughly $1,000-$1,500 in one-time legal and setup fees plus state filing fees and $300-$700 in annual fees.

- The seven setup steps are: open the self directed IRA, fund the IRA, form a single member LLC owned by the IRA, draft an IRA-compliant operating agreement, get an EIN, open the LLC’s business checking account, and submit a buy direction letter to wire IRA funds into that account.

- The IRA owns the LLC, the LLC owns the assets, and you act as a non-compensated manager. Never an employee, never a beneficiary of the LLC’s cash, never a personal user of LLC-owned property.

- The structure pays off most clearly above a $50,000 IRA balance and for self directed investors running multiple deals per year in real estate, precious metals, private notes, or crypto.

- Pay every IRA-related fee out of the LLC bank account, never from your personal checking account or a separate business checking account.

If you want help walking through whether a checkbook control ira llc fits your retirement accounts and the kind of investments you have in mind, Bullionite Asset Group consults with self directed investors across Newport Beach California and the rest of the country on real estate IRAs, precious metals, and crypto IRA structures. We can also coordinate the directed ira custodian, the ira llc facilitator

FAQ's

Is a self directed IRA LLC with checkbook control IRS approved?

The IRS does not formally “approve” any IRA structure or any specific investment. The legal foundation rests on Swanson v. Commissioner, FSA 200128011, and Ellis v. Commissioner. Each ruling treated the structure as legitimate as long as the prohibited transaction rules in Section 4975 are followed.

Can I be the manager of my own IRA LLC?

Yes. The IRA holder can serve as the manager of an ira owned llc and sign every check on the LLC bank account. You cannot draw a salary, take a fee, or accept any compensation for that role. Ellis v. Commissioner is the controlling case on this point.

Can my IRA LLC buy real estate?

Yes. Buying real estate is one of the most common uses of a checkbook ira llc. The deed has to be titled in the LLC’s name. You cannot live in the property, and any rental income flows back to the LLC bank account, not to your personal checking account. Real estate investors with three or more properties tend to favor the IRA llc structure because each closing happens on the buyer’s timeline instead of the custodian’s queue. The check book ira can also invest real estate through partnerships, syndications, and private placements as long as no disqualified person sits on the other side of the deal.

Can I hold bitcoin in a checkbook control IRA LLC?

Yes. The LLC can open an account at a crypto exchange and hold bitcoin or other digital assets. The exchange account has to be in the LLC’s name with the LLC’s EIN, not your personal account. The same rule applies for precious metals — the LLC, not you, has to hold title and physical custody at an approved depository.

What is the minimum IRA balance worth setting up a checkbook control LLC?

Most facilitators and CPAs treat $50,000 as the rough breakeven point where flat-fee setup and annual costs work out cheaper than transaction-based fees from a non-checkbook self directed ira custodian. Below $50,000, a standard SDIRA is usually cheaper. Above $100,000, the savings compound quickly per year.

Can a checkbook IRA LLC have a member other than the IRA?

A single member llc with only the IRA as owner is the cleanest structure. Multi-member llc structures exist (often a husband and wife pooling two retirement accounts into one llc, sometimes called an llc owned ira partnership), but they require careful operating agreement language and are easier to mess up. Most account holders should stick with the single member llc.

Do I file a tax return for the IRA LLC?

A single member llc owned by a tax-exempt entity (the IRA) is generally treated as a disregarded entity and does not file its own income tax return. The ira llc only files Form 990-T if it earns unrelated business income or unrelated debt-financed income above $1,000 per year. The custodian handles annual IRA reporting (Form 5498).

Can I move my existing self directed IRA into a checkbook control LLC?

Yes. The transfer is the same step-2 funding move, just from one self directed ira custodian to another, or from a standard SDIRA into the new ira llc. No tax consequences if you do a direct transfer.

Have Questions About Your Self-Directed IRA?

Schedule a free 15-minute consultation with Bullionite Asset Group. No pitch, no pressure, no referral commissions.

As the Founder and Chief Investment Officer of Bullionite and Bullionite Asset Group, I’ve built my career on a simple premise understanding the intersection of macroeconomics, commodities, and digital assets to stay ahead of the curve, not under it. My focus is on navigating the complexities of the world’s largest markets spanning the US, the Middle East, and Asia to identify high-value opportunities for alternative investment.

With a specialized focus on Self-Directed IRAs (SDIRAs), I help investors move beyond traditional 401ks by integrating assets like precious metals and cryptocurrency into their retirement strategies. Based in Newport Beach, California, I am dedicated to bridging the gap between traditional finance and the evolving landscape of new age digital assets, ensuring that every strategic move is backed by deep market insight and a commitment to long-term growth.