Bitcoin Roth IRA: How to Hold Crypto Tax-Free in a Self-Directed Roth IRA (2026 Guide)

Section 1: What Is a Bitcoin Roth IRA

A Bitcoin Roth IRA is a self-directed Roth IRA that holds cryptocurrency as its investment. The “self-directed” part is what makes it different from a standard Roth IRA. A standard Roth IRA at Fidelity or Schwab limits you to stocks, bonds, mutual funds, and ETFs from their approved menus. A self-directed Roth IRA removes that restriction entirely, letting you hold real estate, precious metals, private placements, and, when held with the right custodian, cryptocurrency.

The tax structure is identical to any Roth IRA: contributions go in after-tax, growth is completely tax-free inside the account, and qualified distributions in retirement come out free of federal income tax. You also pay no capital gains tax on intra-account trades. Swapping Bitcoin for Ethereum, rebalancing from SOL to BTC, or accumulating gains over 20 years without touching the account, all of it happens without generating a single taxable event.

Why the Self-Directed Structure Is Required

The IRS has not prohibited cryptocurrency in IRAs. What limits most investors is custodian capability, not regulation. Major brokerages built their IRA infrastructure around publicly traded securities. They haven’t extended that to digital asset custody, which requires entirely different infrastructure: private key management, blockchain-native settlement, and cryptocurrency-specific security protocols.

A self-directed IRA custodian is an IRS-approved trust company specifically built to hold alternative assets. They execute your trade directions, maintain custody of digital assets through secure wallet infrastructure, and handle the IRS reporting (Form 5498 for annual fair market value, Form 1099-R for distributions). You direct the investments. They hold the assets.

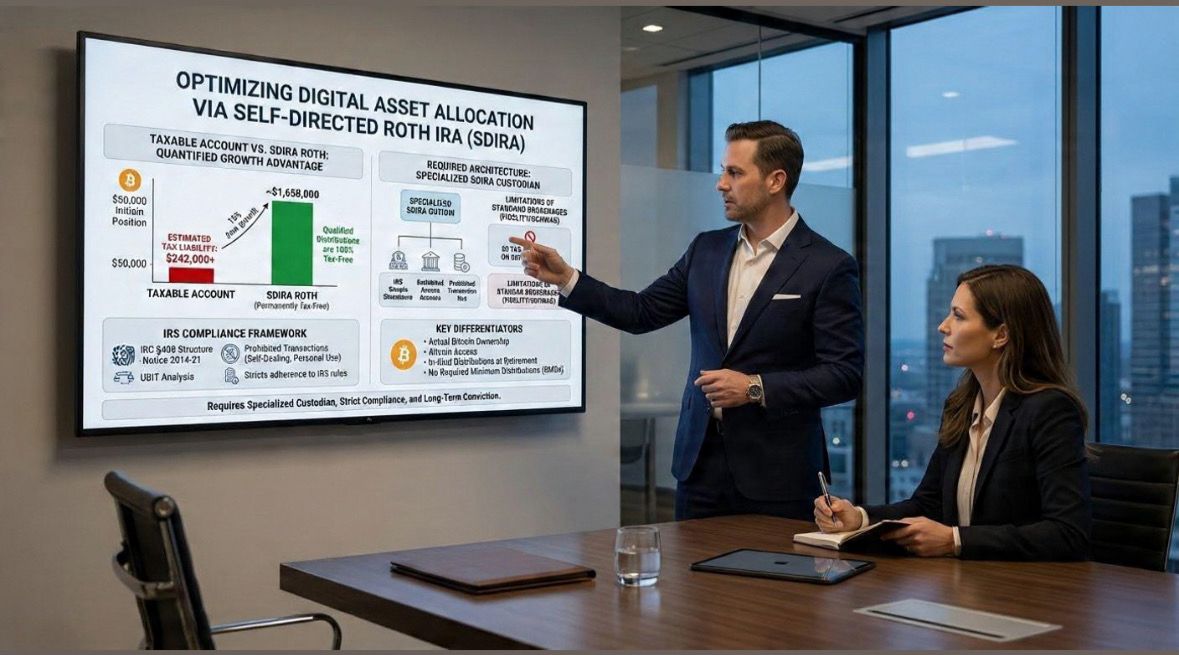

The IRS authority comes from IRC §408 (IRA structure) and Notice 2014-21, which established that virtual currency is property for federal tax purposes. Property can be held in IRAs. The only exceptions in IRC §408(m) are collectibles, life insurance, and precious metals below purity thresholds. Cryptocurrency is none of those.

Bitcoin Roth IRA vs Standard Roth IRA: Core Structural Comparison

| Factor | Standard Roth IRA (Fidelity/Schwab) | Bitcoin Roth IRA (SDIRA Custodian) |

|---|---|---|

| What you can hold | Stocks, bonds, ETFs, mutual funds | Cryptocurrency + all other SDIRA-eligible assets |

| Bitcoin exposure available | Spot Bitcoin ETF (price exposure only) | Actual Bitcoin ownership |

| Altcoin access | Very limited | Bitcoin, Ethereum, Solana, XRP, and more |

| In-kind distribution option | No | Yes, receive actual crypto at retirement |

| Staking / yield inside account | No | Possible (with UBIT analysis required) |

| Annual account fees | $0 at most brokerages | Custodian fee + trading/custody fees |

| Tax treatment of growth | Tax-free | Tax-free |

| Required Minimum Distributions | None | None |

| Rollover from existing Roth IRA | Can receive transfers | Can receive transfers from any Roth IRA |

| Account opening complexity | Simple | Requires SDIRA custodian selection |

For a full breakdown of how the SDIRA structure works across all alternative asset classes, see our self-directed IRA complete guide.

Section 2: The Tax Case for a Bitcoin Roth IRA

This section makes the specific, quantified tax case. The numbers are striking enough to warrant the setup cost.

The Taxable Account Problem for Crypto Investors

The IRS classifies cryptocurrency as property under Notice 2014-21. Every taxable event, meaning every sale, every crypto-to-crypto swap, every conversion to stablecoin, and every DeFi interaction that involves disposal of a token, generates a reportable gain or loss. Short-term gains (held under 12 months) are taxed as ordinary income, up to 37% federally. Long-term gains (held over 12 months) are taxed at 0%, 15%, or 20%, plus a 3.8% net investment income tax for high earners.

Active crypto investors holding in taxable accounts get Form 1099-DA from exchanges and face significant tax exposure even before touching cash. An investor who bought Bitcoin at $30,000 and swapped it for Ethereum when Bitcoin reached $100,000 realized a $70,000 taxable gain on the swap, even if they never withdrew a single $.

Inside a Bitcoin Roth IRA, that swap generates no taxable event. Zero. The gain stays inside the account, compounds, and only becomes relevant when you take qualified distributions at retirement, at which point it is tax-free.

The Roth Advantage Quantified

The Roth structure is particularly powerful for volatile, high-appreciation assets like Bitcoin because the tax benefit scales with appreciation. More appreciation means more tax eliminated.

Scenario: $50,000 Bitcoin position at age 40, distributed tax-free at age 65

| Assumption | Roth IRA | Taxable Account |

|---|---|---|

| Starting position | $50,000 | $50,000 |

| Annual growth rate (assumed) | 15% | 15% |

| Value at age 65 (25 years) | ~$1,658,000 | ~$1,658,000 |

| Taxes on growth | $0 | $242,000 at 15% LTCG (approximate, no interim trading) |

| Taxes on active rebalancing | $0 | Significant additional exposure per trade |

| Net at distribution | ~$1,658,000 | ~$1,416,000 or less |

| Roth advantage | +$242,000+ | Baseline |

That $242,000 figure is the minimum advantage, assuming perfect buy-and-hold with no rebalancing in the taxable account. Any active rebalancing in a taxable account generates additional taxable events and reduces that net figure further.

The Roth advantage grows proportionally with: higher starting amounts, higher appreciation rates, longer time horizons, and more frequent rebalancing.

Traditional Crypto IRA vs Roth Crypto IRA: Which Is Better?

The short answer: Roth crypto IRA almost always wins for long-duration, high-conviction Bitcoin positions.

| Factor | Traditional Crypto IRA | Roth Crypto IRA |

|---|---|---|

| Contribution type | Pre-tax (deductible contributions) | After-tax |

| Growth | Tax-deferred | Tax-free |

| Distributions | Ordinary income tax applies | Tax-free (qualified distributions) |

| Required Minimum Distributions | Yes, starting at age 73 | None |

| Inheriting rules | Successor must follow 10-year rule | Beneficiary also receives tax-free growth |

| Best scenario | Rolling over large pre-tax 401k | Long-duration crypto with 15+ year horizon |

| Worst scenario | Taking large distributions in high-income retirement years | Paying conversion tax when you’re already in a low bracket |

The one scenario where Traditional beats Roth: rolling over a very large pre-tax 401k balance, where triggering a Roth conversion creates an immediate six-figure taxable event you can’t absorb. In that case, a Traditional crypto IRA still captures tax-deferred growth and is meaningfully better than holding crypto in a taxable account.

For everything else, the Roth wins. No RMDs means no forced Bitcoin selling on a government timeline. No distribution tax means every $ of decades of compounding is yours.

The 28% Collectibles Tax Eliminated

Physical gold, silver, and other collectibles held in a taxable account are taxed at 28%, the IRS collectibles rate, which is higher than the standard long-term capital gains rate. Cryptocurrency held in a taxable account does not receive collectibles treatment. It’s taxed at regular long-term capital gains rates.

But this comparison matters for retirement strategy: investors considering both a precious metals IRA and a Bitcoin Roth IRA should know that both assets benefit from being inside a Roth structure, just for slightly different reasons. Gold eliminates the collectibles rate; Bitcoin eliminates capital gains rates and the complexity of trade-by-trade tracking.

Section 3: IRS Rules That Govern Crypto in a Self-Directed Roth IRA

The compliance framework for a Bitcoin Roth IRA is the same framework that governs any self-directed IRA. The penalty for violations is identical: the entire IRA is disqualified, the full fair market value is treated as ordinary income in the year the violation occurred, and a 10% early withdrawal penalty applies if you’re under 59.5. On a $300,000 Bitcoin Roth IRA, that’s a potential $90,000 to $135,000 tax bill from a single mistake.

What the IRS Actually Permits

The IRS has not prohibited cryptocurrency in IRAs. Notice 2014-21 established that virtual currency is property for federal tax purposes. Property can be an IRA investment unless it falls under the explicit exclusions in IRC §408(m): collectibles, life insurance, and precious metals below purity thresholds. Cryptocurrency is none of those.

Additional IRS guidance has addressed NFTs (Notice 2023-27, which flagged certain NFTs as potential collectibles requiring analysis) and digital asset reporting obligations. But for Bitcoin, Ethereum, Solana, and the major established cryptocurrencies, the IRS has issued no guidance treating them as prohibited IRA investments.

The Four Prohibited Transaction Triggers for Crypto IRAs

| Prohibited Action | IRS Basis | Consequence |

|---|---|---|

| Moving IRA Bitcoin to your personal wallet | IRC §4975: personal benefit from IRA assets | Entire IRA treated as distributed, ordinary income tax + possible 10% penalty |

| Buying crypto from yourself at any price | IRC §4975(c)(1)(A): sale between IRA and disqualified person | Same full disqualification |

| Selling personal crypto to your IRA | IRC §4975(c)(1)(A): self-dealing | Same full disqualification |

| Using IRA crypto as collateral for a personal loan | IRC §4975(c)(1)(B): extension of credit | Same full disqualification |

| Paying yourself a management fee from the IRA | IRC §4975(c)(1)(D): indirect benefit to disqualified person | Same full disqualification |

Disqualified persons include you, your spouse, your children and their spouses, your parents, any entity where you own 50%+ equity, and any fiduciary of the IRA. The disqualified person rules are broad. Any transaction between your Roth IRA and a disqualified person at any price triggers prohibited transaction analysis.

UBIT: The Tax That Catches Crypto Roth IRA Investors Off Guard

Unrelated Business Income Tax applies when a Roth IRA earns income from an active business or trade under IRC §§511-514. The Roth structure eliminates income tax on investment returns, but UBIT is a separate tax that can apply even inside a Roth IRA.

For Bitcoin Roth IRA holders, UBIT becomes relevant in these situations:

Staking rewards. When your IRA earns staking rewards from proof-of-stake cryptocurrencies like Ethereum or Solana, the IRS may treat those rewards as income from an active trade or business, generating Unrelated Business Taxable Income (UBTI). UBIT is taxed at trust rates that reach 37% at just $15,650 of income (2026 thresholds).

Lending and yield activity. Crypto lending programs, centralized yield accounts, and DeFi yield strategies inside an IRA can generate UBTI if the activity constitutes an active trade or business.

What does not trigger UBIT: passive price appreciation, capital gains from selling appreciated cryptocurrency, and dividend-equivalent distributions from funds. The vast majority of buy-and-hold Bitcoin investors inside a Roth IRA never encounter UBIT.

Practical guidance: if your Roth crypto IRA strategy is buying Bitcoin, holding it, and eventually selling it, UBIT is not a concern. If you’re planning staking, lending, or DeFi participation inside the IRA, work with a CPA who understands both SDIRA rules and cryptocurrency tax treatment before implementing any yield strategy.

For a complete SDIRA prohibited transaction reference, see our self-directed IRA rules and compliance guide.

Section 4: How to Open a Bitcoin Roth IRA: Step by Step

Step 1: Confirm a Roth IRA Is Right for Your Situation (Week 1)

Before opening a Bitcoin Roth IRA, confirm it’s the right structure:

Roth IRA income limits for 2026: Roth IRA contributions phase out for single filers with modified adjusted gross income above $150,000 and are eliminated above $165,000 (verify current IRS thresholds as these adjust annually). Married filers have higher thresholds. Income limits apply to new contributions only. They do not affect your ability to transfer an existing Roth IRA into a self-directed crypto custodian.

If you’re over income limits for contributions: a Backdoor Roth IRA strategy may still let you fund a Roth IRA. This involves making a non-deductible Traditional IRA contribution and then converting to Roth. The conversion is fully permissible; consult a CPA on the pro-rata rule implications if you have other Traditional IRA balances.

If you have a large pre-tax 401k to roll over: a Traditional crypto IRA avoids a taxable conversion event. Don’t trigger a Roth conversion you can’t absorb just to get the tax-free growth label on the account.

Step 2: Select a Self-Directed IRA Custodian That Supports Crypto (Week 1-2)

The custodian selection is the most consequential decision in this process. You need an IRS-approved trust company with specific cryptocurrency custody capability. Not every SDIRA custodian supports digital assets.

What to evaluate when choosing a crypto Roth IRA custodian:

| Evaluation Factor | What Good Looks Like | Red Flag |

|---|---|---|

| Cryptocurrency coverage | Bitcoin plus meaningful altcoin selection | Bitcoin-only with no expansion roadmap |

| Custody security | Qualified custodian handling, cold storage majority, multi-sig architecture | Vague custody language; no specific security documentation |

| IRS reporting | Form 5498 filed annually with fair market values; Form 1099-R issued on distributions | Can’t confirm their IRS filing procedures |

| Fee transparency | Complete fee schedule in writing before account opening | Fees only disclosed after you’ve started the process |

| Rollover experience | Has processed 401k direct rollovers and same-type IRA transfers | Limited experience with rollover mechanics |

| UBIT guidance | Clearly discloses UBIT risk for staking and yield activity | Promotes staking without UBIT disclosure |

| Customer support | Knowledgeable on both crypto and SDIRA compliance topics | Refers all compliance questions to generic disclaimers |

Step 3: Fund the Account (Week 1-4)

Option A: Transfer from an existing Roth IRA (most common, no tax, no cap) If you already have a Roth IRA at Fidelity, Vanguard, or Schwab, you can transfer it to a crypto SDIRA custodian through a same-type IRA transfer. Your new custodian initiates the paperwork. Funds move as cash. You pay no taxes, no penalties, and there’s no dollar cap because this is a transfer, not a contribution. Timeline: 5 to 10 business days for most brokerages.

Option B: Direct rollover from a Roth 401k If your employer plan has a Roth 401k option and you’re leaving that job, you can roll it directly into a self-directed Roth IRA with a crypto custodian. Direct rollover means funds wire from the plan to the custodian. You never touch the money. No withholding, no taxes, no penalties. Timeline: 10 to 20 business days for most corporate plans.

Option C: Annual Roth IRA contribution Up to $7,000 in 2026 ($8,000 if age 50 or older), subject to income limits. Funded from a personal checking or savings account. The smallest funding route, but suitable for investors starting fresh.

Can I move my Roth IRA into crypto without tax consequences? Yes. Transferring an existing Roth IRA from any brokerage to a self-directed Roth IRA custodian is a non-taxable, same-type transfer. The IRS does not treat this as a distribution or a conversion. You’re moving the same Roth account to a different custodian. Tax consequence: zero.

Step 4: Direct Your Bitcoin and Crypto Purchases (Week 3-6)

Once funds land at the custodian, you submit trade instructions through their platform directing them to purchase specific cryptocurrencies. Most crypto SDIRA custodians have built trading interfaces similar to standard crypto exchanges, except all assets settle into IRA-titled wallets, not personal accounts.

The important distinction: you’re directing the custodian to buy. You are not buying. The transaction is between your IRA and the cryptocurrency exchange or counterparty. That distinction is what makes it a non-taxable IRA transaction rather than a personal purchase.

Typical documents needed to open a crypto Roth IRA:

- Government-issued photo ID (passport or driver’s license)

- Social Security number or Tax ID

- Beneficiary designation form

- Existing Roth IRA account number (if transferring) or funding bank account (if contributing)

- Completed custodian application

How long does it take from account open to first Bitcoin purchase? Account approval: 1 to 3 business days. Funding via transfer: 5 to 10 business days. First trade available: same day or next day after funds are received. Full timeline from application to first Bitcoin purchase: typically 2 to 3 weeks for a transfer, 3 to 4 weeks for a 401k rollover.

Minimum investment for a crypto Roth IRA: Varies by custodian. Some have no account minimums; others require $1,000 to $5,000 to open. Transfer-funded accounts are generally not subject to minimums. Annual contributions are limited by the $7,000 / $8,000 IRS caps.

For a complete rollover walkthrough, see our 401k to crypto IRA rollover guide.

Section 5: Bitcoin Roth IRA vs the Alternatives

Semantic targets: Bitcoin IRA vs Bitcoin ETF in IRA | crypto IRA vs traditional IRA differences | Roth IRA crypto vs traditional IRA crypto | crypto IRA vs crypto Roth IRA which to choose | holding crypto in IRA vs holding crypto yourself | should I put crypto in my IRA or taxable account | self directed ira vs traditional ira | solo 401k vs self directed ira | crypto or ira | self-directed IRA crypto vs Bitcoin ETF comparison | roth ira and crypto | crypto ira vs roth ira

Bitcoin Roth IRA vs Spot Bitcoin ETF in a Roth IRA at Fidelity

This is the comparison most investors need to resolve first. Both are tax-advantaged. Both give you Roth treatment. But they’re fundamentally different products.

| Factor | Bitcoin ETF in Standard Roth IRA | Bitcoin in Self-Directed Roth IRA |

|---|---|---|

| What you own | Shares in a fund that tracks Bitcoin price | Actual Bitcoin in an IRA-titled wallet |

| Available at | Fidelity, Schwab, Vanguard, most brokerages | Specialized SDIRA custodians only |

| Bitcoin-specific costs | 0.20-0.25% annual ETF expense ratio | Custodian fee + trading/custody fees |

| Other cryptocurrency access | Bitcoin and Ethereum ETFs (very limited) | Bitcoin, Ethereum, Solana, XRP, and more |

| In-kind distribution | Cash only | Can receive actual Bitcoin at retirement |

| Staking participation | Not available | Possible (UBIT analysis required) |

| Security of assets | Trust in ETF issuer and custodian chain | Trust in SDIRA custodian’s custody infrastructure |

| Account setup complexity | Open a standard Roth IRA | Select SDIRA custodian, fund, direct trades |

| Break-even on fees vs ETF | N/A (ETF wins under ~$75,000) | Above $75,000-$100,000, comparable or favorable |

For investors primarily interested in Bitcoin price exposure, with a modest allocation under $75,000, a spot Bitcoin ETF inside a standard Roth IRA at a major brokerage is simpler and cheaper. The SDIRA structure earns its cost above that threshold, for investors who want actual ownership, broader altcoin access, or the ability to take in-kind distributions.

Bitcoin Roth IRA vs Holding Crypto in a Taxable Account

This is the comparison that best illustrates the Roth IRA’s value proposition.

| Factor | Taxable Crypto Account | Bitcoin Roth IRA |

|---|---|---|

| Tax on each crypto-to-crypto swap | Taxable event, capital gains rate | No tax inside the IRA |

| Tax on Bitcoin sale at gain | Short-term or long-term capital gains | No tax (qualified Roth distribution) |

| Annual contribution limit | No limit | $7,000/$8,000 (more via rollover) |

| Tax on distributions | Capital gains + ordinary income mix | Zero for qualified distributions |

| Tax-loss harvesting available | Yes | No (losses have no tax value inside IRA) |

| RMDs | No | No (Roth advantage) |

| Custody | Personal exchange or self-custody | SDIRA custodian holds keys |

| Best for | Active trading, short-term positions | Long-duration buy-and-hold positions |

The taxable account wins in exactly one scenario: active short-term trading where tax-loss harvesting generates meaningful offsets. For buy-and-hold positions spanning 10+ years, the Roth IRA wins decisively on after-tax returns.

Roth Crypto IRA vs Traditional Crypto IRA

This comparison matters most for investors doing a 401k rollover. The question is whether to convert to Roth (pay tax now) or maintain Traditional status (defer tax to distribution).

The framework for deciding:

Choose Roth if: you’re in a lower tax bracket now than you expect to be at distribution, your Bitcoin position has significant appreciation potential ahead, and you can pay the conversion tax without drawing from retirement assets.

Choose Traditional if: the rollover amount is large enough that Roth conversion triggers a major tax event, you’re in your peak earning years now and expect lower income in retirement, or you simply can’t absorb a conversion tax in the current year.

The hybrid approach: some investors roll over into a Traditional crypto IRA and then do a partial Roth conversion in lower-income years (early retirement, gap years, sabbaticals) to move appreciated crypto into Roth status at reduced tax rates.

Section 6: Distributions, RMDs, and Inheriting a Bitcoin Roth IRA

Qualified Distributions from a Bitcoin Roth IRA

A “qualified distribution” from a Roth IRA is completely tax-free and penalty-free. The requirements:

- The distribution occurs at least 5 years after January 1st of the year you first contributed to any Roth IRA (the “5-year rule”)

- You are at least 59.5 years old (or the distribution meets another qualifying exception: disability, first-time home purchase up to $10,000, or death)

If both conditions are met, you receive Bitcoin or the cash value of your Bitcoin completely free of federal income tax. No tax on the original principal. No tax on decades of appreciation. None.

In-Kind Distributions: Receiving Actual Bitcoin

One of the unique advantages of a self-directed crypto Roth IRA over a Bitcoin ETF is the ability to take in-kind distributions. Rather than selling your Bitcoin and receiving cash, you can request that the actual Bitcoin be transferred from your IRA-titled wallet to your personal wallet.

The in-kind distribution is still treated as a distribution for IRS purposes. The fair market value of the Bitcoin on the distribution date determines the “amount distributed.” For a qualified Roth distribution, that fair market value is tax-free. You receive the Bitcoin. You owe nothing.

Why this matters: if you believe Bitcoin will continue appreciating significantly after you retire, you may not want to sell. An in-kind distribution lets you receive actual Bitcoin into your personal custody, continuing to benefit from any appreciation, without the IRA structure you no longer need.

No Required Minimum Distributions

Traditional IRAs and Traditional crypto IRAs require annual minimum distributions starting at age 73 under SECURE 2.0. That means forced liquidation of your Bitcoin position on a government-mandated schedule, potentially in a down market, generating ordinary income tax in the year of distribution.

A Roth IRA has no RMDs. You can let your Bitcoin compound inside the Roth IRA indefinitely, passing it to heirs without ever being forced to sell. This is one of the most underappreciated advantages of the Roth structure for volatile long-duration assets.

Early Withdrawals: What Happens Before 59.5

Roth IRA early withdrawal rules have two components: contributions and earnings.

Contributions to a Roth IRA can be withdrawn at any time, at any age, tax-free and penalty-free. Since contributions went in after-tax, the IRS has no claim on them.

Earnings withdrawn before the account is both 5 years old and before you’re 59.5 are subject to income tax plus a 10% penalty. For a Bitcoin Roth IRA with a large appreciated position, this is the primary risk of early withdrawal.

Ordering rules: the IRS uses a specific ordering for Roth withdrawals. Contributions come out first (always tax and penalty-free), then converted amounts (subject to specific rules), then earnings (taxable and penalized if the conditions aren’t met).

The practical implication: if you contributed $50,000 over several years and your account is now worth $200,000, the first $50,000 you withdraw before 59.5 is completely tax-free and penalty-free. The remaining $150,000 of gains would face taxes and a possible 10% penalty if withdrawn early.

Inheriting a Bitcoin Roth IRA

Inheriting a Roth IRA that holds Bitcoin or other cryptocurrency is both a financial opportunity and an administrative responsibility.

Spouse beneficiary: A surviving spouse can treat the inherited Roth IRA as their own. No RMDs. Continued tax-free growth. The most favorable outcome.

Non-spouse beneficiary (children, other heirs): Under the SECURE Act and SECURE 2.0, most non-spouse beneficiaries must distribute the entire inherited IRA within 10 years of the original owner’s death (the “10-year rule”). The distributions can come in any amount and at any time within those 10 years, with no annual RMD requirement in years 1-9. All distributions from an inherited Roth IRA remain tax-free if the 5-year rule was satisfied by the original owner.

The Bitcoin Roth IRA for estate planning: because Roth IRAs pass to heirs with no income tax on distributions, a heavily appreciated Bitcoin Roth IRA is one of the most tax-efficient assets to pass on. Heirs receive the full appreciated value without an income tax bill, subject only to the 10-year distribution window.

Section 7: Is a Bitcoin Roth IRA Worth It?

The Honest Investment Case

The tax-free compounding argument for a Bitcoin Roth IRA is mathematically strong. The risk profile of the underlying asset is not.

Bitcoin has produced 70% to 80% drawdowns in previous bear markets. An investor who moved a significant portion of their Roth IRA into Bitcoin at the November 2021 peak faced a 77% decline by November 2022. That’s not a paper loss you can tax-harvest in a Roth IRA. There’s no tax offset. It’s just a loss.

The Roth structure doesn’t reduce volatility. It doesn’t protect against Bitcoin-specific risks. It eliminates taxes on gains. For that benefit to materialize, the gains have to exist.

The Allocation Framework

There is no universally correct Bitcoin allocation for a retirement account. The framework below reflects a range of risk profiles:

| Risk Profile | Bitcoin Roth IRA as % of Total Retirement Assets | Rationale |

|---|---|---|

| Conservative | 2-5% | Asymmetric upside exposure without catastrophic impact if Bitcoin declines 80% |

| Moderate | 5-10% | Meaningful exposure while keeping primary retirement assets in diversified holdings |

| Aggressive | 10-20% | High conviction on Bitcoin as long-term store of value; full volatility accepted |

| Speculative | 20%+ | Only reasonable when total retirement assets are large enough that maximum downside is survivable |

The guiding principle: size your Bitcoin Roth IRA position such that an 80% decline in Bitcoin would not materially impair your retirement security. Treat it as the asymmetric, high-conviction position it is, not as the core of your retirement plan.

Dollar-Cost Averaging Into a Bitcoin Roth IRA

Rather than moving a lump sum into Bitcoin on a single date, many investors use their annual contribution limit ($7,000 / $8,000) to add to their Bitcoin Roth IRA in regular increments. This reduces timing risk on an asset with Bitcoin’s volatility profile.

For rollover-funded accounts, phasing purchases over 6 to 12 months accomplishes the same goal, though it requires the custodian to hold uninvested cash during the accumulation period.

Rebalancing Without Tax Consequence

Inside a taxable account, selling Bitcoin to rebalance into Ethereum triggers a capital gains event. Inside a Bitcoin Roth IRA, rebalancing between Bitcoin, Ethereum, Solana, or stablecoins generates no taxable event. The entire rebalancing decision is made on portfolio strategy, not tax timing.

This is practically valuable for volatility management. If Bitcoin has a significant runup and now represents 90% of your crypto IRA position, rebalancing back to 60/40 Bitcoin/Ethereum incurs no cost. You manage the allocation based on what makes sense, not based on tax minimization.

Who Should Open a Bitcoin Roth IRA

Strong candidate if:

- You have a 15+ year investment horizon

- You have an existing Roth IRA to transfer (no contribution limits apply)

- You have strong, informed conviction on Bitcoin’s long-term value

- You want actual Bitcoin ownership rather than ETF price exposure

- You’re specifically attracted to no RMDs and the estate planning advantages

Probably not your best move if:

- You’re within 5 years of retirement and can’t absorb significant drawdown

- You’re buying because of a high-pressure sales pitch rather than considered strategy

- Bitcoin would represent more than 20-25% of your total retirement assets

- You’ve never owned cryptocurrency before and don’t understand the volatility

- Your total Roth IRA balance is small enough that fees would represent more than 1-2% annually

Key Takeaways

- A Bitcoin Roth IRA is a self-directed Roth IRA that holds actual cryptocurrency, not a Bitcoin ETF.

- The Roth structure is the most tax-efficient vehicle for long-duration crypto positions: all appreciation is permanently tax-free, no RMDs exist, and qualified distributions come out completely free of federal tax.

- You cannot open a Bitcoin Roth IRA at Fidelity, Schwab, or Vanguard. A specialized SDIRA custodian is required.

- IRS Notice 2014-21 classifies virtual currency as property. No IRS provision prohibits cryptocurrency in a Roth IRA.

- UBIT applies when your Roth IRA earns income through staking, lending, or DeFi yield activity. Passive price appreciation is not subject to UBIT.

- Transferring an existing Roth IRA to a crypto SDIRA custodian is a tax-free, no-penalty process with no dollar cap.

- A Roth IRA has no Required Minimum Distributions. That means you can let Bitcoin compound inside the account indefinitely without forced liquidation.

- In-kind distributions are possible: at retirement, you can receive actual Bitcoin rather than cash.

Disclosure: Nothing in this article constitutes tax, legal, or personalized investment advice. Consult a qualified professional before making any retirement account decisions.

About BullioniteAssetGroup BullioniteAssetGroup specializes in self-directed IRA advisory across real estate, precious metals, Crypto IRA and alternative assets.

Primary Sources:

- IRS Notice 2014-21: Virtual Currency Guidance: irs.gov/pub/irs-drop/n-14-21.pdf

- IRS Notice 2023-27: NFT and Digital Asset Guidance: irs.gov/pub/irs-drop/n-23-27.pdf

- IRS IRC §4975: Prohibited Transactions: irs.gov/retirement-plans/prohibited-transactions

- IRS IRC §§511-514: UBIT Rules: irs.gov/charities-non-profits/unrelated-business-income-tax

- IRS Publication 590-B: Roth IRA Distributions: irs.gov/publications/p590b

- SECURE 2.0 Act: RMD and Inherited IRA Rules: congress.gov/bill/117th-congress/house-bill/2954

- IRS Publication 590-A: Roth IRA Contributions and Income Limits: irs.gov/publications/p590a

Published February 2026 | BullioniteAssetGroup.com

Can you buy crypto in a Roth IRA?

Yes. You can hold Bitcoin, Ethereum, and other cryptocurrencies inside a Roth IRA. The key is that you need a self-directed Roth IRA (SDIRA) held with a specialized custodian that supports digital assets. Standard Roth IRAs at Fidelity, Schwab, and Vanguard don’t offer actual cryptocurrency custody, though they do offer spot Bitcoin and Ethereum ETF exposure.

The IRS has not prohibited cryptocurrency in IRAs. Notice 2014-21 classifies virtual currency as property, and property is an eligible IRA investment. What the IRS requires is that all IRA assets be held by a qualified custodian, not personally by the account holder.

To buy Bitcoin in a Roth IRA: select an SDIRA custodian with crypto capability, open or transfer a Roth IRA to that custodian, fund the account, and direct the custodian to purchase specific cryptocurrencies on your IRA’s behalf. The entire process takes 2 to 4 weeks for a transfer-funded account.

What are the tax benefits of a Bitcoin IRA?

The primary tax benefit depends on account type. In a Roth Bitcoin IRA, all growth is completely tax-free. A $50,000 Bitcoin position that grows to $500,000 over 20 years distributes tax-free at retirement with zero federal income tax on the $450,000 gain. No capital gains tax. No ordinary income tax. In a taxable account, that same gain at 15% long-term capital gains rates would cost $67,500 in federal taxes before factoring in any state tax.

In a Traditional Bitcoin IRA, growth is tax-deferred: no annual taxes on gains, trades, or rebalancing, but distributions are taxed as ordinary income in retirement.

Both structures eliminate the transaction-level tax complexity that makes crypto so challenging in taxable accounts. Every crypto-to-crypto swap, every rebalancing trade, and every accumulation of gains over the years happens inside the IRA without generating a Form 1099.

Is a crypto IRA legitimate?

Yes. A properly structured crypto self-directed IRA is a fully compliant retirement account under IRS law. The IRS has not prohibited cryptocurrency in IRAs. Properly licensed SDIRA custodians file Form 5498 annually with fair market values and issue Form 1099-R on distributions, exactly as any other IRA custodian does.

What makes a crypto IRA legitimate: an IRS-approved trust company as custodian, compliance with prohibited transaction rules, accurate IRS reporting, and proper custody of digital assets separate from any personal holdings.

What makes a crypto IRA problematic: self-custody arrangements where the account holder takes personal possession of IRA-held crypto, transactions with disqualified persons, promoters who market “home storage” compliance, and platforms that don’t file required IRS forms.

Do your due diligence on the custodian. Ask specifically who holds the private keys to IRA-titled wallets, what their Form 5498 filing process looks like, and whether they’re an IRS-approved trust company. Those are the legitimacy markers that matter.

Can you take in-kind distributions from a Bitcoin Roth IRA?

Yes. One of the genuine advantages of a self-directed Roth IRA over a Bitcoin ETF in a standard IRA is the ability to take in-kind distributions. Rather than selling Bitcoin and receiving cash, you can request that the custodian transfer actual Bitcoin from your IRA-titled wallet to your personal wallet at distribution.

For a qualified Roth distribution (account at least 5 years old, you’re at least 59.5), the fair market value of the Bitcoin on the distribution date is the amount of the distribution. For a Roth, that amount is completely tax-free. You receive the Bitcoin. No taxes owed.

This is particularly valuable for investors who believe Bitcoin will continue appreciating after retirement. You can receive actual Bitcoin into personal custody, continuing to benefit from future appreciation without the IRA structure you no longer need.

Can you rebalance a Bitcoin Roth IRA without paying taxes?

Yes. One of the most practical advantages of holding cryptocurrency inside a Roth IRA rather than a taxable account is the ability to rebalance without tax consequences. Selling Bitcoin and buying Ethereum inside the IRA generates no taxable event. Neither does moving from crypto to stablecoins during volatile periods, or shifting allocations among Bitcoin, Solana, and other holdings.

In a taxable crypto account, every sale creates a reportable gain or loss that affects your annual tax return. Inside the IRA, none of those intra-account transactions appear on your tax return. You manage the allocation based entirely on strategy, not tax minimization.

The only caution: if the rebalancing involves staking or yield-generating activity, UBIT analysis is needed before implementation.

Have Questions About Your Self-Directed IRA?

Schedule a free 30-minute consultation with Bullionite Asset Group. No pitch, no pressure, no referral commissions.

As the Founder and Chief Investment Officer of Bullionite and Bullionite Asset Group, I’ve built my career on a simple premise understanding the intersection of macroeconomics, commodities, and digital assets to stay ahead of the curve, not under it. My focus is on navigating the complexities of the world’s largest markets spanning the US, the Middle East, and Asia to identify high-value opportunities for alternative investment.

With a specialized focus on Self-Directed IRAs (SDIRAs), I help investors move beyond traditional 401ks by integrating assets like precious metals and cryptocurrency into their retirement strategies. Based in Newport Beach, California, I am dedicated to bridging the gap between traditional finance and the evolving landscape of new age digital assets, ensuring that every strategic move is backed by deep market insight and a commitment to long-term growth.