Self Directed IRA vs Roth IRA: Complete Comparison Guide

TL;DR

Self directed IRA and Roth IRA are not competing account types they describe two separate dimensions of retirement account design. “Self directed” defines investment flexibility (real estate, cryptocurrency, precious metals, private equity). “Roth” defines tax structure (after-tax contributions, tax-free qualified withdrawals, no required minimum distributions). These two designations are not mutually exclusive: a self directed Roth IRA combines both. Traditional self directed IRAs offer upfront deductions and tax-deferred growth but impose required minimum distributions at age 73. Self directed Roth IRAs eliminate RMDs entirely and generate zero federal tax on qualified withdrawals. Which structure wins depends on your current marginal tax bracket, retirement timeline, alternative asset investment strategy, and long-term income expectations.

Self Directed IRA vs Roth IRA: The Complete 2026 Comparison Guide

The distinction between a self directed IRA vs Roth IRA comes down to two entirely different dimensions of retirement account design investment access and tax treatment and conflating the two is one of the most expensive mistakes retirement savers make. A self directed IRA is not a tax classification. It is an account structure granting access to alternative assets outside the conventional brokerage universe: real estate properties, physical precious metals, cryptocurrency, private placements, tax liens, and private mortgages. A Roth IRA, by contrast, is purely a tax designation: contributions made from after-tax income, zero federal tax on qualified distributions, and no required minimum distributions during your lifetime.

The critical insight that most investors miss: these two designations are stackable. A self directed Roth IRA is a single account that combines alternative investment access with Roth tax advantages. Understanding where these structures diverge and where they intersect determines which account you should open, how to fund it, and what assets generate the most tax efficiency inside each structure. For a foundational overview of self-directed retirement accounts before drilling into this comparison, see our complete self-directed IRA guide.

What Is the Difference Between a Self Directed IRA vs Roth IRA?

The core distinction: “Self directed” defines what you can invest in. “Roth” defines how those investments are taxed. They operate on different axes and can coexist in one account.

Three practical account types exist for investors considering self-direction:

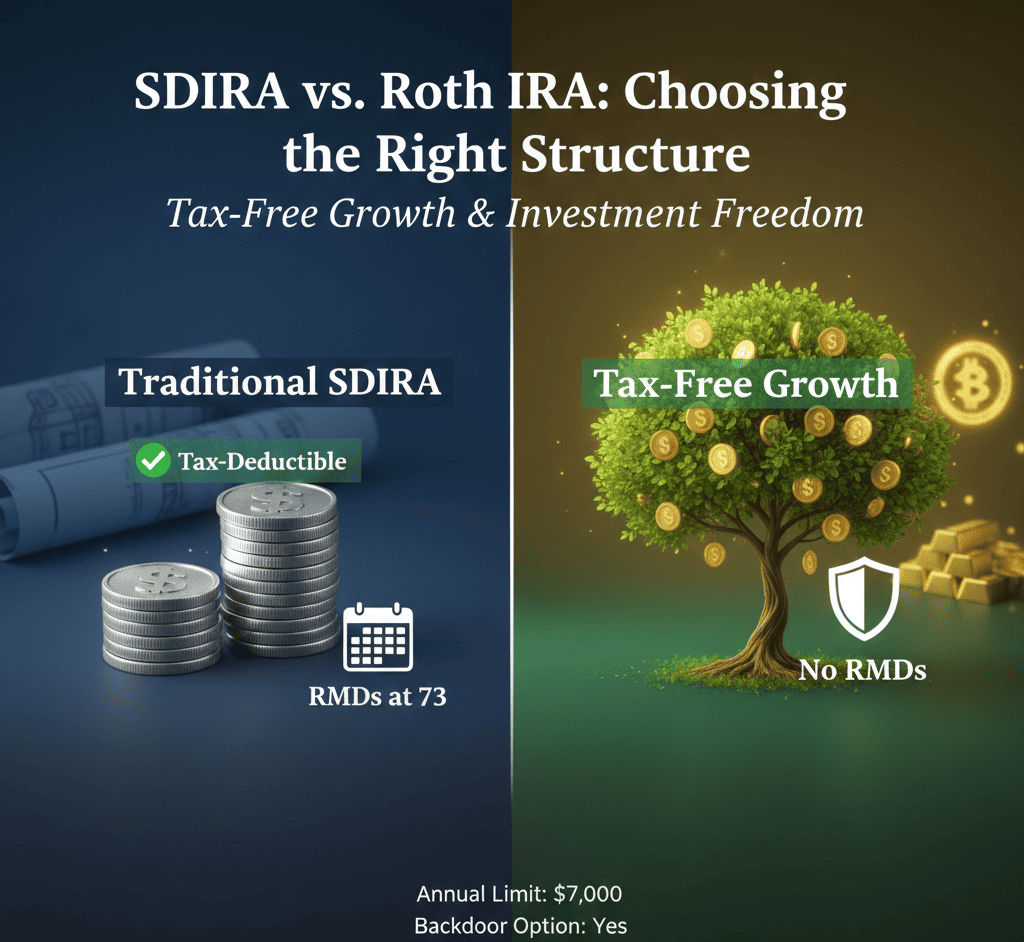

- Traditional Self Directed IRA alternative investment access, pre-tax or non-deductible contributions, taxable distributions at ordinary income rates, required minimum distributions at age 73.

- Self Directed Roth IRA alternative investment access, after-tax contributions, tax-free qualified distributions, no required minimum distributions.

- Standard Roth IRA conventional brokerage-listed investments only (stocks, ETFs, mutual funds), after-tax contributions, tax-free qualified distributions, no RMDs.

Most investors asking about self directed IRA vs Roth IRA are implicitly asking: should I combine self-direction with Roth tax treatment? The answer depends on the tax analysis below.

|

Feature |

Traditional Self Directed IRA |

Self Directed Roth IRA |

Standard Roth IRA |

|

Investment Universe |

Alternative assets (RE, crypto, metals, PE) |

Alternative assets (RE, crypto, metals, PE) |

Stocks, ETFs, mutual funds only |

|

Contribution Tax Treatment |

Pre-tax (potentially deductible) |

After-tax (no deduction) |

After-tax (no deduction) |

|

Growth |

Tax-deferred |

Tax-free |

Tax-free |

|

Distributions |

Taxed as ordinary income |

Tax-free (qualified) |

Tax-free (qualified) |

|

Required Minimum Distributions |

Yes age 73 (IRC §401(a)(9)) |

No RMDs (lifetime) |

No RMDs (lifetime) |

|

Income Restriction |

Deductibility phases out |

Contributions phase out |

Contributions phase out |

|

Early Withdrawal Penalty |

10% + income tax before 59½ |

Contributions: never; Earnings: 10% + tax before qualifying |

Contributions: never; Earnings: 10% + tax before qualifying |

Tax Treatment Compared: Traditional Self Directed IRA vs Self Directed Roth IRA

Tax treatment is the decisive variable in the self directed IRA vs Roth IRA decision. Getting this wrong costs decades of compounding returns on every asset you hold inside the account.

Traditional Self Directed IRA Tax Profile

- Deductibility: Contributions may be fully or partially deductible depending on MAGI and workplace retirement plan participation (IRS Publication 590-A).

- Tax-deferred growth: No annual tax on rental income, capital gains, interest, or appreciation generated inside the account during accumulation.

- Distributions: All withdrawals taxed as ordinary income at your marginal rate in the year of withdrawal including appreciation on real estate, crypto gains, and precious metals.

- Required minimum distributions: Begin at age 73 under SECURE 2.0 Act provisions. Failure to take RMDs triggers a 25% excise tax on the shortfall.

- Early withdrawal: Withdrawals before age 59½ incur ordinary income tax plus a 10% early withdrawal penalty, with limited exceptions under IRC §72(t).

Self Directed Roth IRA Tax Profile

- No upfront deduction: Contributions made from after-tax income. No deduction taken in the contribution year.

- Tax-free growth: All investment growth rental income, Bitcoin appreciation, private equity returns accumulates completely tax-free inside the account.

- Tax-free qualified distributions: Withdrawals meeting both conditions (age 59½ or older AND five-year rule satisfied) generate zero federal income tax, regardless of account size or appreciation magnitude.

- No RMDs: Self directed Roth IRAs impose no required minimum distributions during the original account holder’s lifetime, allowing indefinite tax-free compounding.

- Contribution access: Your original contributions (not earnings) can be withdrawn anytime, tax-free and penalty-free, since taxes were already paid on them.

The Five-Year Rule Critical Detail: Roth IRA earnings are only tax-free if the account has been open for at least five tax years AND you are age 59½ or older at withdrawal. The five-year clock starts January 1 of the first tax year for which you made a Roth contribution not the calendar date the account was opened. Each Roth conversion carries its own separate five-year period for penalty-free withdrawal of converted amounts.

For a full breakdown of annual tax obligations across self-directed account structures, including UBIT (Unrelated Business Income Tax) and UDFI on leveraged real estate, see our self-directed IRA tax filing requirements guide.

Contribution Limits and Income Eligibility for Self Directed IRA vs Roth IRA (2026)

Contribution limits apply identically to traditional and Roth IRA structures including self directed variants. Per IRS Publication 590-A, verify current limits at IRS.gov as these are inflation-adjusted annually.

|

Contribution Type |

Under Age 50 |

Age 50 or Older (Catch-Up) |

|

Annual IRA Contribution Limit |

$7,000 |

$8,000 |

|

Combined Limit (Across ALL IRAs) |

$7,000 total |

$8,000 total |

Critical rule: The annual IRA limit applies across all IRA accounts combined. Contributing the full amount to a traditional self directed IRA forecloses additional Roth IRA contributions for that tax year. You may split contributions between account types, but combined contributions cannot exceed the annual cap.

Traditional IRA Deductibility Phase-Outs

For individuals covered by a workplace retirement plan (verify current thresholds at IRS.gov):

- Single filers: Deduction phases out between approximately $77,000–$87,000 MAGI

- Married filing jointly (covered spouse): Phase-out between approximately $123,000–$143,000 MAGI

- Non-covered spouse (covered by plan through work): Phase-out between approximately $230,000–$240,000 MAGI

Roth IRA Contribution Eligibility Phase-Outs

Roth IRA contribution eligibility phases out at the same MAGI thresholds whether the account is self directed or standard (verify current thresholds at IRS.gov):

- Single filers: Phase-out begins around $150,000 MAGI, full ineligibility at approximately $165,000

- Married filing jointly: Phase-out between approximately $236,000–$246,000 MAGI

Backdoor Roth IRA for High Earners: High-income investors above Roth eligibility thresholds can access Roth tax treatment through a backdoor Roth conversion: make a nondeductible traditional IRA contribution, then immediately convert to Roth. The conversion triggers ordinary income tax only on any earnings accrued between contribution and conversion typically negligible for immediate conversions. The IRS does not cap annual conversion amounts. Those rolling over from employer plans should see our 401(k) to self directed IRA complete rollover guide for related mechanics.

Investment Options What Can You Hold in a Self Directed IRA vs a Standard Roth IRA?

This is the structural advantage of self-direction. Standard Roth IRAs at conventional brokerages restrict you to publicly traded securities. Self directed IRAs whether traditional or Roth open the full alternative asset universe permissible under IRC §408:

Real Estate

Rental properties, commercial buildings, raw land, real estate notes, fix-and-flip properties, and real estate crowdfunding platforms. All rental income and appreciation flow back into the IRA tax-deferred (traditional) or tax-free (Roth). A self directed Roth IRA holding an appreciated rental property generates zero tax on that appreciation at distribution. See our self-directed IRA real estate rules guide for compliance specifics. For a broader view, the self-directed real estate IRA 2026 guide covers custodian requirements, UDFI, and prohibited transaction pitfalls specific to property ownership inside IRAs.

Precious Metals

IRS-approved gold (minimum 99.5% fineness), silver (99.9%), platinum (99.95%), and palladium (99.95%) held at an IRS-approved depository home storage of IRA-owned metals is a prohibited transaction. See our precious metals SDIRA diversification benefits guide and what is a gold and silver IRA for metal-specific rules.

Cryptocurrency

Bitcoin, Ethereum, and other cryptocurrencies held directly through a qualified SDIRA custodian or via a checkbook control LLC structure. The tax case for a self directed Roth IRA for cryptocurrency is compelling: Bitcoin appreciation that would generate significant capital gains tax in a taxable account grows completely tax-free inside a Roth structure. A $50,000 Bitcoin position that grows 10× inside a self directed Roth IRA produces $450,000 in gains taxed at exactly zero percent on qualified withdrawal. See our self directed Roth IRA for crypto guide, Bitcoin Roth IRA: hold crypto tax-free, and self directed crypto IRA overview for full setup and custodian details. For a cost-benefit analysis of crypto IRA vs alternative crypto investment structures, see crypto IRA pros and cons.

Private Equity, Startups, and Alternative Credit

Private placements, LLC membership interests, venture capital fund interests, angel investment rounds, tax liens, trust deeds, private mortgages, and peer-to-peer lending arrangements are all permissible within both traditional and Roth self directed IRAs. Each carries unique due diligence requirements, liquidity constraints, and regulatory compliance obligations that a qualified SDIRA custodian must facilitate.

For investors evaluating whether self-direction is the right move, is a self-directed IRA a good idea? walks through the suitability framework for different investor profiles. Investors coming from a 401(k) should also understand how a self-directed IRA differs from a 401(k) before initiating a rollover.

Prohibited Transaction Rules Identical for Both Account Types

Prohibited transaction rules under IRC §4975 apply with identical force to traditional self directed IRAs and self directed Roth IRAs. Violating these rules does not result in a penalty you pay and move on from a prohibited transaction disqualifies the entire account, triggering immediate taxation of its full fair market value in the year of violation.

Disqualified Persons Under IRC §4975

- The IRA owner and their spouse

- Lineal descendants and ancestors (children, parents, grandchildren, grandparents)

- Any entity in which the above persons own 50% or more of voting power or beneficial interest

- IRA fiduciaries and service providers with certain relationships to the above

Common Prohibited Transactions to Avoid

- Personal use of IRA-owned real estate even one night of personal occupancy by the IRA owner or a disqualified person triggers disqualification.

- Self-managing IRA properties without fair market compensation services to the IRA must be performed by third parties at arm’s length rates or paid through the IRA at fair market rates.

- Selling a personally owned asset to your IRA regardless of whether the price is fair market value.

- Extending credit between your IRA and a disqualified person including loans from your IRA to a family member or business you control.

- Family members renting IRA property below market rate any below-market arrangement constitutes a prohibited transaction.

There is no cure for a prohibited transaction it retroactively disqualifies the IRA from its establishment date or from the date of the violation. Specialist SDIRA legal guidance is non-negotiable for complex investment scenarios. See our full breakdown of SDIRA rules and prohibited transactions covering every major scenario. For checkbook control structures that give IRA owners more direct investment execution, see self-directed IRA LLC checkbook control explained and note that checkbook control does not exempt you from prohibited transaction rules; it only streamlines transaction execution within those rules.

Distribution Rules and Early Withdrawal Penalties

Traditional Self Directed IRA Distribution Rules

- Before age 59½: Ordinary income tax at marginal rate plus 10% early withdrawal penalty. Exceptions under IRC §72(t) include substantially equal periodic payments, first-time home purchase (lifetime limit $10,000), qualified higher education expenses, and certain medical costs exceeding 7.5% of AGI.

- After age 59½: Ordinary income tax at your marginal rate; no penalty.

- Required minimum distributions: Begin at age 73 under the SECURE 2.0 Act. Annual RMD amounts calculated using IRS life expectancy tables in Publication 590-B. Failure to take RMDs triggers a 25% excise tax on the shortfall (reduced to 10% if corrected promptly).

Self Directed Roth IRA Distribution Rules

- Contributions (not earnings): Withdrawable anytime, tax-free and penalty-free. You already paid income tax on these amounts at contribution.

- Earnings qualified distributions: Tax-free and penalty-free when (1) account holder is age 59½ or older, AND (2) at least five tax years have passed since the first Roth contribution to any Roth IRA. Both conditions must be satisfied simultaneously.

- Earnings non-qualified distributions: Subject to ordinary income tax plus 10% early withdrawal penalty, with the same IRC §72(t) exceptions available to traditional IRAs.

- No RMDs: Roth IRA owners face no required minimum distributions during their lifetime. Assets can compound tax-free indefinitely.

- Inherited Roth IRAs: Non-spouse beneficiaries are generally subject to the 10-year distribution rule under the SECURE 2.0 Act, but inherited Roth distributions remain income-tax-free if the five-year rule was satisfied by the original owner.

The absence of RMDs in Roth accounts is a significant retirement planning advantage it allows assets to compound without forced liquidations and supports tax-efficient legacy planning. For rollover rules governing the 60-day window for indirect rollovers, see our 60-day self-directed IRA rollover rule guide.

Self Directed IRA vs Roth IRA: Which Is Right for Alternative Asset Investors?

For investors specifically targeting real estate, cryptocurrency, precious metals, or private equity inside a retirement account, the decision framework is straightforward:

Choose a Traditional Self Directed IRA When:

- Your current marginal income tax rate is high (32%+) and you reasonably expect a lower effective rate in retirement

- You want the upfront deduction to reduce this year’s taxable income and have the discipline to invest the tax savings

- You’re investing in income-producing real estate where tax-deferred compounding over decades provides a structural advantage

- You have significant other retirement income sources and don’t need maximum flexibility around distributions

Choose a Self Directed Roth IRA When:

- You’re in a lower current tax bracket (22% or below) and expect higher rates in retirement through career advancement, larger retirement income, or potential future tax law changes

- You’re investing in high-appreciation assets cryptocurrency, startup equity where future gains will be substantial and tax-free treatment on those gains is enormously valuable

- You want no required minimum distributions and maximum withdrawal flexibility in retirement

- You’re a younger investor (under 45) with 20–40 years for tax-free compounding the Roth advantage compounds dramatically over long timeframes

- You’re focused on tax-efficient legacy planning and want to pass Roth assets to heirs with no income tax consequences

Consider Holding Both Tax Diversification Strategy

Maintaining both traditional and Roth self directed accounts provides flexibility to optimize withdrawal strategy in retirement based on actual income needs and prevailing tax rates. In high-income years, draw from Roth accounts to avoid pushing into higher brackets on traditional IRA distributions. In lower-income years, draw from traditional accounts at lower effective rates while allowing Roth assets to continue compounding tax-free.

For a full suitability assessment across investor profiles, see is a self-directed IRA a good idea? For investors specifically interested in selecting a custodian to facilitate either structure, see the best self-directed IRA custodian comparison 2026.

Roth Conversion Strategy for Self Directed IRA Holders

Roth conversions allow traditional IRA holders to transfer balances to Roth IRA status by recognizing the converted amount as ordinary income in the conversion year. The IRS does not restrict the dollar amount of annual Roth conversions you pay the tax on the converted amount, and those assets permanently enter Roth tax treatment. For self directed IRA holders, this strategy carries timing advantages not available in conventional IRA conversions.

Optimal Conversion Windows for SDIRA Holders

- Low-income years: Early retirement years before Social Security commencement, sabbatical years, or years with large business deductions create conversion windows at depressed effective tax rates.

- Alternative asset valuation downturns: Converting cryptocurrency positions during bear markets or real estate holdings during a downturn minimizes immediate taxable income while maximizing future tax-free appreciation potential. A Bitcoin IRA holding converted at $30,000/BTC, then appreciating to $150,000/BTC inside a Roth, generates zero tax on that $120,000/BTC gain at qualified distribution.

- Years with offsetting deductions: Large charitable contributions, business operating losses, or significant medical expenses in a single year can offset Roth conversion income, effectively enabling conversions at near-zero marginal rates.

Multi-Year Bracket-Filling Strategy

Rather than converting large balances in a single year and triggering a higher bracket, spread conversions across multiple years. Convert up to the top of your current bracket without crossing into the next marginal rate. For example, a married filer in the 22% bracket can convert enough each year to bring total income to the top of the 22% threshold stopping before crossing into 24%. Repeat annually until the traditional IRA balance is sufficiently reduced or fully converted.

Valuation requirement: Converting alternative assets (real estate, private equity, collectibles) requires an independent qualified appraisal establishing fair market value. The taxable conversion amount is fair market value at conversion not original purchase price. The IRS requires qualified appraisals for real estate and certain other alternative assets.

For investors rolling existing 401(k) balances into a self directed IRA as a precursor to Roth conversion, see our 401(k) to self-directed IRA rollover complete guide. For checkbook control structures that can simplify Roth conversion execution with alternative assets, see self-directed IRA LLC with checkbook control setup.

Authoritative Sources & Further Reading

IRS Publication 590-A Contributions to Individual Retirement Arrangements (IRAs): irs.gov/publications/p590a

IRS Publication 590-B Distributions from Individual Retirement Arrangements (IRAs): irs.gov/publications/p590b

IRC §4975 Prohibited Transaction Rules (IRS): irs.gov/retirement-plans/prohibited-transactions

SEC Investor Education Alternative Investments: investor.gov/introduction-investing

DOL ERISA Fiduciary Overview: dol.gov/agencies/ebsa

Key Takeaways

- Self directed IRA and Roth IRA are not competitors they describe two different axes of account design (investment access vs. tax treatment) and can be combined in a single self directed Roth IRA that delivers alternative asset access with tax-free qualified distributions.

- Traditional self directed IRAs provide potential upfront deductions and tax-deferred growth, but impose required minimum distributions at age 73 and ordinary income tax on every distribution including appreciation on real estate, crypto, and precious metals.

- Self directed Roth IRAs generate completely tax-free growth and zero tax on qualified withdrawals, with no lifetime RMDs advantages that compound most powerfully for high-appreciation assets like cryptocurrency and early-stage private equity over long time horizons.

- Annual contribution limits of $7,000 (under 50) or $8,000 (50+) apply across all IRA accounts combined. Roth eligibility phases out at higher MAGI thresholds; traditional IRA deductibility phases out separately for workplace retirement plan participants.

- Self-direction unlocks real estate, cryptocurrency, precious metals, and private equity within either traditional or Roth tax structures the choice of tax treatment is entirely independent of the decision to self-direct.

- Prohibited transaction rules under IRC §4975 apply with identical force and identical consequences to both account types. A single prohibited transaction disqualifies the entire account, triggering immediate taxation of its full value.

- Roth conversions are most tax-efficient during low-income years, alternative asset valuation downturns, or years with large offsetting deductions. Multi-year bracket-filling strategies minimize conversion tax liability while permanently securing assets in tax-free Roth treatment.

What is the difference between a self directed IRA and a Roth IRA?

A self directed IRA describes investment flexibility allowing alternative assets like real estate, precious metals, and private equity beyond traditional stocks and bonds. A Roth IRA defines the tax structure with after tax contributions and tax free qualified distributions. These terms are not mutually exclusive, as you can establish a self directed Roth IRA combining alternative investment access with Roth tax advantages, or maintain a traditional self directed IRA offering alternative assets with tax deferred growth and potentially deductible contributions.

Can a self directed IRA be a Roth IRA?

Yes, self directed IRAs can utilize either traditional or Roth tax treatment based on your retirement planning preferences. A self directed Roth IRA combines the investment flexibility of self direction with Roth tax advantages including tax free qualified distributions and no required minimum distributions during your lifetime. You contribute after tax dollars to self directed Roth IRAs, then enjoy completely tax free growth and withdrawals on alternative investments including real estate appreciation, cryptocurrency gains, or private equity returns after meeting age and holding period requirements.

Can I convert my traditional self directed IRA to a Roth IRA?

Yes, you can convert traditional self directed IRA balances to Roth IRA status by paying income taxes on converted amounts during the conversion year. This strategy proves particularly valuable during low income years or when alternative assets hold temporarily depressed values minimizing immediate tax liability while maximizing future tax free appreciation potential. Strategic conversions spread over multiple years prevent pushing you into higher tax brackets through single large conversions. The IRS permits unlimited annual conversions without contribution limit restrictions, enabling substantial traditional to Roth transfers for those willing to pay conversion taxes.

Have Questions About Your Self-Directed IRA?

Schedule a free 15-minute consultation with Bullionite Asset Group. No pitch, no pressure, no referral commissions.

FAQ Schema Markup Loaded

As the Founder and Chief Investment Officer of Bullionite and Bullionite Asset Group, I’ve built my career on a simple premise understanding the intersection of macroeconomics, commodities, and digital assets to stay ahead of the curve, not under it. My focus is on navigating the complexities of the world’s largest markets spanning the US, the Middle East, and Asia to identify high-value opportunities for alternative investment.

With a specialized focus on Self-Directed IRAs (SDIRAs), I help investors move beyond traditional 401ks by integrating assets like precious metals and cryptocurrency into their retirement strategies. Based in Newport Beach, California, I am dedicated to bridging the gap between traditional finance and the evolving landscape of new age digital assets, ensuring that every strategic move is backed by deep market insight and a commitment to long-term growth.