TL;DR: Self-directed IRAs (SDIRAs) let you invest retirement funds in alternative assets like real estate, precious metals, private equity, and cryptocurrencies—options unavailable in traditional IRAs. While offering diversification and potentially higher returns, these investments require specialized custodians ($295-$595 annually), carry prohibited transaction risks that can disqualify your entire IRA, and demand thorough due diligence since IRS rules prohibit using IRA property for personal benefit.

Can You Actually Invest in Alternative Assets Through Your IRA?

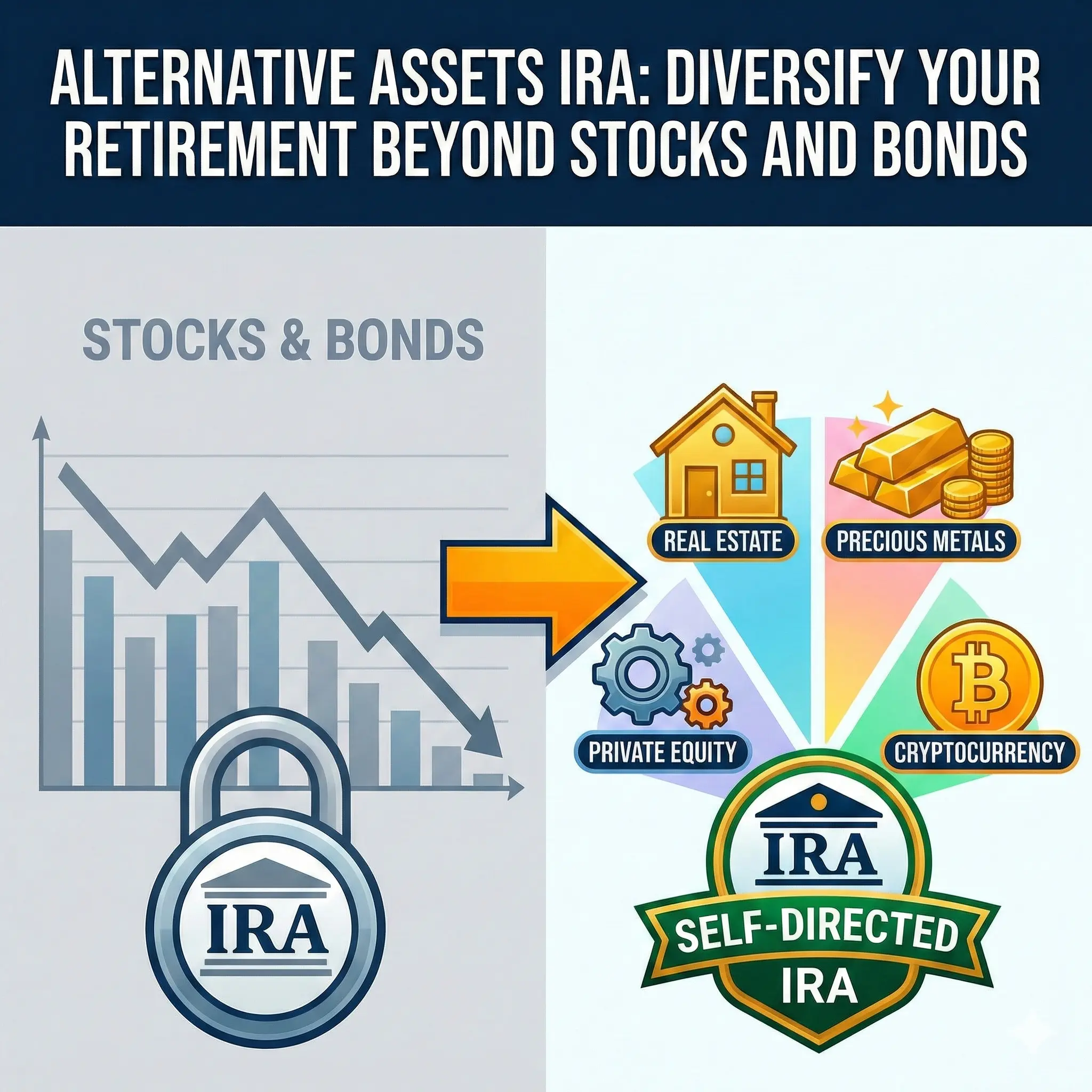

Yes, self-directed IRAs allow you to purchase alternative assets including rental properties, precious metals, private placements, tax liens, cryptocurrencies, and even farmland with your retirement funds. The IRS permits nearly any investment except collectibles (art, rugs, antiques), life insurance, and S-corporation stock. Your IRA holds title to these assets, all income flows back tax-deferred (Traditional) or tax-free (Roth), and you gain diversification beyond the stock-bond mix dominating conventional retirement accounts.

Setting up an alternative assets IRA takes three steps. You open an account with a self-directed IRA custodian specializing in alternatives—not Vanguard or Fidelity, which don’t offer this service. You fund the account through transfers, rollovers, or annual contributions ($7,000 for 2026 if under 50, $8,000 if 50+). Then you direct the custodian to purchase your chosen alternative asset, with all expenses paid from IRA funds and income deposited back to the account.

The tax advantages mirror traditional retirement accounts. Traditional self-directed IRAs defer taxes on contributions and gains until withdrawal at 59½. Roth SDIRAs use after-tax contributions but deliver tax-free growth and qualified withdrawals. For a rental property generating $18,000 annually, that’s $18,000 growing tax-sheltered year after year—compounding without the annual tax drag that reduces personally-owned investment returns.

Types of Alternative Assets You Can Hold in a Self-Directed IRA

Real Estate: The Most Popular SDIRA Investment

Real estate dominates self-directed IRA portfolios, with industry data showing it accounts for approximately 68% of alternative asset holdings. Investors purchase single-family rentals, multifamily properties, commercial buildings, raw land, and even real estate notes.

The process requires precision. Your IRA custodian holds legal title recorded as “[Custodian Name] FBO [Your Name] IRA.” You cannot live in the property, rent to family members, or perform repairs yourself—these constitute prohibited transactions under IRC Section 4975. All rental income, property taxes, insurance, and maintenance must flow through the IRA.

For example, a $165,000 duplex purchased through a Roth IRA in 2021 with professional property management (required for IRS compliance) costing 8% of gross rent generates $2,100 monthly. After expenses, net cash flow reaches $14,400 annually—8.7% return entirely tax-free when distributed after age 59½. As of 2026, similar properties appreciate to approximately $198,000, creating total IRA value of $218,000 through appreciation plus reinvested cash flow.

However, leveraged real estate creates complications. If you finance an IRA property purchase, you must use non-recourse loans where the lender’s only remedy upon default is seizing the property itself. Personal guarantees are prohibited. Additionally, debt-financed portions trigger Unrelated Business Income Tax (UBIT) under IRC Sections 511-514, potentially creating taxable income within your IRA despite its tax-advantaged status.

| IRA Real Estate Advantage | IRA Real Estate Limitation |

|---|---|

| Tax-deferred/tax-free rental income | Cannot personally use property |

| No capital gains tax on appreciation | No family members as tenants/contractors |

| Diversification from stocks | All expenses must come from IRA funds |

| Tangible asset control | Professional management required |

| Hedge against inflation | Non-recourse financing only |

Precious Metals: Gold, Silver, Platinum, and Palladium

Self-directed IRAs can hold IRS-approved precious metals meeting specific purity standards: gold (99.5% pure), silver (99.9%), platinum (99.95%), and palladium (99.95%). American Eagle coins qualify regardless of purity. Your metals must be stored with an approved depository—not in your home safe, which triggers immediate distribution and taxes plus a 10% early withdrawal penalty if you’re under 59½.

According to the World Gold Council, gold has delivered 10.4% average annual returns over the past two decades, outperforming inflation and providing portfolio insurance during stock market crashes. In March 2020, while the S&P 500 dropped 34%, gold declined just 12% before recovering to new highs within months.

Typical allocations range from 5-15% of a self-directed IRA to precious metals as portfolio ballast. For instance, a $75,000 transfer from a traditional IRA to purchase 48 ounces of gold in 2019 at $1,480 per ounce would be worth over $127,000 by February 2026 with gold near $2,650 per ounce—a 69% gain growing tax-deferred until retirement withdrawals begin.

Storage fees run $125-$250 annually depending on precious metals value and depository choice. Dealers charge 2-5% over spot price when buying, and you’ll pay a similar spread when liquidating. These costs erode returns compared to gold ETFs, but the physical asset ownership and bankruptcy-remote storage appeal to investors seeking maximum security for retirement wealth.

Private Equity and Private Placements

Accredited investors ($200,000+ annual income or $1 million+ net worth excluding primary residence) can direct IRA funds into private companies, venture capital, and private equity funds. These investments offer exposure to pre-IPO growth companies and alternative strategies unavailable in public markets.

The National Venture Capital Association reports that venture-backed companies returned 13.9% annually over the past 25 years, beating public market indices by 3-4 percentage points. However, individual deal success rates tell a different story—70% of startups fail, 20% break even, and only 10% deliver outsized returns that compensate for the losses.

Private placements in SDIRAs demand extreme caution regarding prohibited transactions. Investing IRA funds in a company where you’re an officer, director, or >10% owner violates IRS rules. Investing in your business partner’s company where you provide services is also prohibited. If your IRA buys shares in a firm that later hires you as a consultant, complications arise requiring immediate professional guidance to avoid IRA disqualification.

Cryptocurrencies and Digital Assets

Bitcoin, Ethereum, and other cryptocurrencies qualify as alternative IRA investments. Specialized crypto-focused self-directed IRA custodians have emerged, though traditional SDIRA providers increasingly add this capability.

Cryptocurrency volatility makes it a high-risk IRA allocation. Bitcoin traded below $20,000 in late 2022, rallied past $69,000 in 2024, and experienced 30-40% drawdowns multiple times. For retirement accounts with decades until withdrawal, some investors accept this volatility for potential long-term appreciation.

From a tax perspective, crypto in an IRA delivers significant advantages over direct ownership. Cryptocurrency trades trigger capital gains taxes in taxable accounts every time you sell or exchange coins. In an IRA, you can rebalance between Bitcoin, Ethereum, and altcoins without immediate tax consequences. All gains compound tax-deferred (Traditional IRA) or tax-free (Roth IRA).

The IRS treats cryptocurrency as property, meaning similar prohibited transaction rules apply. You cannot mine crypto using equipment owned by your IRA if you personally control the mining operation. You cannot stake coins from your IRA if you receive staking rewards into personal accounts. The line between permitted passive investment and prohibited self-dealing requires careful navigation.

How Self-Directed IRAs Work for Alternative Assets

Choosing the Right Custodian

Not all custodians handle all alternative assets. Some specialize in real estate, others in precious metals, and certain providers focus on private placements or cryptocurrency. When evaluating custodians, compare these factors:

Annual fees: Range from $295 to $595 for basic accounts, with sliding scales based on asset value

Transaction fees: $50-$125 per purchase, sale, or payment processed from your IRA

Asset expertise: Does the custodian have experience with your specific alternative investment type?

Funding speed: How quickly can they wire funds for time-sensitive opportunities?

Customer service: Can you reach knowledgeable representatives when prohibited transaction questions arise?

Technology platform: Do they offer online access to account information and transaction history?

Major self-directed IRA custodians include Equity Trust (est. 1974, $39 billion assets under custody), Madison Trust ($495 annual fee), IRA Services ($395 base fee), and The Entrust Group (real estate specialization). Each has strengths depending on your alternative asset focus.

Analysis of IRA property transactions shows custodians with dedicated real estate teams complete purchases approximately 18% faster (average 12 days vs 15 days) than general-purpose providers. When time-sensitive deals require quick closing, that speed difference can mean securing or losing investment opportunities.

The Purchase Process Step-by-Step

Buying alternative assets through your self-directed IRA follows a specific workflow designed to maintain IRS compliance and proper documentation:

Step 1: Identify Investment Opportunity (Week 1-4)

Find your alternative asset—a rental property, private placement, or precious metals dealer. Conduct thorough due diligence since your custodian doesn’t vet investments. If buying real estate, hire independent inspectors and appraisers using IRA funds to pay them.

Step 2: Submit Buy Direction Letter (Week 4-5)

Complete your custodian’s investment authorization form detailing the purchase. For real estate, include property address, purchase price, earnest money amount, closing date, and title company contact information. For private placements, provide company details, share price, and subscription agreement.

Step 3: Custodian Review and Approval (Week 5-6)

The custodian verifies you have sufficient IRA funds, reviews the transaction for obvious prohibited transaction red flags, and prepares to release funds. This typically takes 3-5 business days but can extend to 10 days during busy periods or for complex transactions.

Step 4: Funding and Closing (Week 6-8)

Your custodian wires funds directly to the closing agent or investment sponsor. For real estate, title records in the custodian’s name “FBO” your IRA. For private placements, certificates are issued to your IRA. For precious metals, the dealer ships directly to your approved depository.

Step 5: Ongoing Management

All income flows to your IRA—rent checks deposited to custodian, distributions from private companies sent to custodian, precious metals appreciation realized upon sale. All expenses (property tax, insurance, fund management fees) are paid from IRA funds via custodian-issued checks or wires.

This administrative process creates complexity compared to buying stocks through Fidelity with a few clicks. The trade-off is access to alternative assets offering diversification benefits and potentially superior risk-adjusted returns for investors willing to handle the operational requirements.

Prohibited Transactions: The Critical Compliance Trap

The IRS prohibits “disqualified persons” from benefiting from IRA assets beyond the retirement account’s tax advantages. Disqualified persons include you, your spouse, lineal descendants (children, grandchildren), lineal ascendants (parents, grandparents), and any entities where these individuals hold >50% ownership.

This creates dozens of potential violations:

❌ Buying property from your IRA: Your IRA owns a rental house. You want to purchase it for personal use. This is prohibited—you cannot buy assets from your own IRA except as a distribution at fair market value with full tax consequences.

❌ Renting to family members: Your daughter needs an apartment. Your IRA owns a rental property. Renting to her at any price constitutes a prohibited transaction because she’s a lineal descendant.

❌ Personal repairs and maintenance: Your IRA property needs a new roof. You’re a contractor. You cannot provide labor even at fair market rates—this is self-dealing. You must hire an unrelated third party and pay from IRA funds.

❌ Using IRA property personally: Your IRA owns a vacation condo. You stay there for a weekend, even if you pay fair market rent. This violates the prohibition against personal use of IRA assets.

❌ Mixing personal and IRA funds: Your IRA needs $5,000 more to close a real estate purchase. You cannot loan your IRA money or personally guarantee the shortfall. All funds must come from the IRA or permissible contributions.

The penalty for prohibited transactions? Your entire IRA can be deemed distributed as of January 1st of the violation year. You owe income taxes on the full balance plus 10% early withdrawal penalty if under 59½. A $200,000 IRA becomes a $110,000 disaster after federal and state taxes plus penalties—destroying decades of retirement savings over a compliance misstep.

For example, having a family member who is a licensed electrician perform work on an IRA-owned rental property—even at below-market rates—constitutes a prohibited transaction. An IRS audit discovering such violations can trigger full IRA disqualification. A $180,000 IRA reduced to approximately $94,000 after taxes and penalties represents an $86,000 cost for attempting to save on contractor expenses.

Required Minimum Distributions and Alternative Assets

Traditional IRAs require minimum distributions starting at age 73 (as of 2026 under SECURE Act 2.0). For illiquid alternative assets, this creates planning challenges. If your IRA owns a $300,000 rental property and your RMD is $15,000, you can’t simply withdraw 5% of the property—you must distribute the full property or liquidate to meet the requirement.

Options for handling RMDs with illiquid alternative assets include:

Option 1: Maintain Liquid Reserve

Keep 15-20% of your SDIRA in cash or marketable securities to fund RMDs without forced asset sales. This reduces alternative asset exposure but preserves your chosen investments.

Option 2: Generate Sufficient Income

Structure alternative investments to produce income exceeding RMD requirements. A rental property generating 8% cash-on-cash returns on a $200,000 investment produces $16,000 annually, potentially covering RMDs while maintaining the asset.

Option 3: Distribute Assets In-Kind

Transfer ownership of the alternative asset from your IRA to personal ownership, paying taxes on its fair market value. For appreciated assets, this can be tax-efficient if done in low-income years.

Option 4: Convert to Roth

Before age 73, convert traditional SDIRA assets to Roth IRAs. Pay taxes on the conversion value, then enjoy tax-free growth with no RMDs (Roths don’t require distributions during owner’s lifetime). This works especially well for younger alternative assets expected to appreciate significantly.

Tax Advantages and Considerations for Alternative Assets in IRAs

Tax-Deferred Growth Compounds Faster

Alternative assets generating income or appreciation grow faster in IRAs compared to taxable accounts due to eliminated tax drag. Consider two identical rental properties—one owned personally, one in a self-directed IRA—both purchased for $200,000 and generating $16,000 annual net income.

Taxable Account Performance:

- Annual income: $16,000

- Federal tax (24% bracket): -$3,840

- State tax (5%): -$800

- Net after-tax income: $11,360

- 20-year compounded value (6% reinvestment): $417,000

Traditional IRA Performance:

- Annual income: $16,000

- Taxes during accumulation: $0

- Compounded value (6% reinvestment): $588,000

- Difference: $171,000 more wealth created

The IRA investor has 41% more capital before considering the eventual tax bill at distribution. Even accounting for ordinary income tax rates on IRA withdrawals versus capital gains on personally-owned property sales, the compounding benefit typically outweighs the rate differential over multi-decade periods.

Roth IRA Alternative Assets Create Tax-Free Wealth

For younger investors who can accept the upfront tax cost of Roth contributions or conversions, this creates extraordinary wealth-building potential with alternative assets.

For example, maximizing Roth IRA contributions ($7,000 annually) and investing in a real estate crowdfunding platform averaging 11% returns over a decade results in substantial tax-free growth. Cumulative contributions of $70,000 growing to $127,000 over 10 years continue compounding. Continuing this strategy for 25 more years at similar returns could result in accounts exceeding $1.8 million—all withdrawable tax-free after age 59½.

Compare this to investing the same amounts in a taxable account. She’d face annual taxes on distributions and capital gains. Over 35 years, the tax drag would reduce her ending wealth by an estimated $490,000, assuming identical gross returns. The Roth IRA structure transformed her retirement outcome through eliminating decades of tax friction.

Unrelated Business Income Tax (UBIT) Complexity

When alternative assets in your IRA generate “unrelated business income,” you may owe UBIT despite the account’s tax-advantaged status. Two scenarios trigger UBIT:

1. Debt-Financed Income (UDFI)

If your IRA purchases real estate using a non-recourse loan, the debt-financed portion’s income is taxable. A $300,000 property purchased with $180,000 IRA cash and $120,000 non-recourse financing means 40% of net income and eventual gain faces UBIT.

The calculation uses IRS Form 990-T. If the property generates $24,000 net income, $9,600 (40%) is UDFI subject to trust tax rates—10% on first $2,900, 24% on $2,900-$9,850, 35% on $9,850+. Your IRA owes approximately $2,200 in UBIT that year, paid from IRA funds.

2. Active Business Income

Operating an active trade or business through your IRA triggers UBIT. Buying shares in a passive private placement? No UBIT. Investing IRA funds in a business where you’re actively involved (even if permissible under other rules)? UBIT applies to the business income.

Cryptocurrency staking potentially creates UBIT complications. The IRS hasn’t provided definitive guidance, but staking rewards might constitute active income rather than passive investment returns, triggering UBIT obligations. Conservative structuring—using separate custodians for staking activities or avoiding staking entirely in IRAs until clearer guidance emerges—minimizes compliance risks.

Advantages and Disadvantages of Alternative Assets in Self-Directed IRAs

Key Benefits

Diversification beyond stocks and bonds: Alternative assets correlate weakly with public equity markets, reducing portfolio volatility. During 2022’s stock bear market (S&P 500 -18%), many real estate markets remained flat or slightly positive, and precious metals provided defensive ballast.

Tax-advantaged growth: Traditional IRAs defer taxes on gains and income until withdrawal. tRoth IRAs deliver completelyax-free growth and qualified distributions. For high-income investors in top tax brackets (37% federal plus state taxes), this creates extraordinary value.

Inflation hedges: Real estate, commodities, and farmland tend to appreciate during inflationary periods when stocks and bonds struggle. The 2021-2023 inflation surge saw rental income and property values climb 15-25% in many markets while bond portfolios declined.

Direct asset control: Unlike stock picking where you own fractional claims on large corporations, alternative asset IRAs let you choose specific properties, businesses, or investments based on your expertise and research.

Potential for higher returns: Alternative assets targeting inefficient markets or leveraging specialized knowledge can outperform public securities. Private equity has historically delivered 3-4% annual excess returns over public equities, though with higher volatility and longer holding periods.

Significant Limitations

Custodial fees and complexity: Self-directed IRA custodians charge $295-$595 annually plus transaction fees. Traditional IRAs at Vanguard cost $0. The administrative burden of directing investments, maintaining records, and ensuring compliance adds time and stress.

Prohibited transaction risks: One mistake—renting to your daughter, personally repairing your IRA property, buying an asset from your IRA—can disqualify the entire account. The penalty (full taxation plus 10% penalty if under 59½) is catastrophic relative to the violation.

Limited liquidity: Alternative assets can’t be sold instantly like stocks. Real estate takes 60-120 days to sell. Private equity locks up capital for 7-10 years. If you need funds for unexpected expenses or RMDs, you may face forced asset sales at unfavorable times.

Valuation challenges: Stocks have real-time pricing. Rental properties? You don’t know the true value until you sell. This creates uncertainty in portfolio management and RMD calculations, which require fair market value assessments.

Due diligence requirements: Your custodian doesn’t vet investments—that’s your responsibility. Fraudulent private placements, overvalued real estate, and dubious cryptocurrency schemes target self-directed IRA investors who lack expertise to evaluate complex alternative opportunities.

Higher risk exposure: Alternative assets often carry greater risk than diversified stock/bond portfolios. A single rental property faces concentration risk. Private companies have 70% failure rates. Cryptocurrency can drop 50% in months. Without proper diversification across multiple alternatives, your entire retirement can be jeopardized by one bad investment.

Common Mistakes to Avoid with Alternative Assets in IRAs

Insufficient Liquidity Planning

Many investors allocate 60-80% of their IRA to illiquid alternatives, creating problems when RMDs begin or unexpected expenses arise. For instance, a traditional IRA with $240,000—$200,000 in a real estate syndication (7-year lockup) and $40,000 in precious metals—faces challenges at age 73 when RMDs require withdrawing approximately $13,800. Insufficient liquid holdings force premature syndication withdrawals at substantial penalties (often 20-25%) to meet distribution requirements.

Best practice: Maintain 20-30% of your SDIRA in liquid assets (money market funds, ETFs, publicly-traded REITs) to handle RMDs and unexpected needs without forced sales of illiquid alternatives.

Inadequate Due Diligence

Self-directed IRA custodians don’t evaluate investment quality—they simply process transactions you direct. Scammers target SDIRA investors with fraudulent private placements offering “guaranteed” 15-20% returns. The Securities and Exchange Commission warns that self-directed IRA fraud costs investors hundreds of millions annually.

For example, an $85,000 IRA investment into a promissory note offered by a “real estate developer” promising 12% annual interest secured by property liens can prove catastrophic if the developer is fraudulent, the liens don’t exist, and the properties are worthless. Such scenarios result in complete investment loss—retirement funds grown tax-deferred for decades, entirely eliminated.

Before investing IRA funds in any alternative asset:

- Verify the sponsor’s background through FINRA BrokerCheck and SEC filings

- Review audited financial statements (if unavailable, that’s a red flag)

- Understand the investment structure and how returns are generated

- Consult with CPAs or attorneys specializing in SDIRAs for complex transactions

- Start small—test new alternative asset classes with 5-10% allocations before major commitments

Violating Prohibited Transaction Rules

The most expensive mistake is triggering prohibited transactions that disqualify your IRA. Even innocent violations carry severe penalties. For instance, personally installing new flooring in an IRA rental property over a weekend to save $1,200 creates a prohibited transaction. The IRS deems the entire IRA distributed, generating approximately $52,000 in federal and state taxes plus $16,500 in early withdrawal penalties on a $165,000 account—a $68,500 cost for $1,200 in attempted savings.

Common prohibited transaction triggers:

- Self-dealing: Providing services, lending money, or selling assets to your IRA

- Family involvement: Renting, selling, or buying IRA assets involving lineal family members

- Personal use: Using IRA property for vacations, storage, or any personal benefit

- Indirect benefits: Your business renting office space in an IRA-owned building

When uncertain whether a transaction is prohibited, consult with a CPA specializing in self-directed IRAs before proceeding. A $300-$500 consultation fee is cheap insurance against $50,000-$200,000 IRA disqualification penalties.

Alternative Assets IRA vs. Traditional IRA: Making the Right Choice

Not everyone should use self-directed IRAs for alternative assets. The additional complexity, costs, risks, and administrative burden only make sense for specific investor profiles.

Consider Alternative Assets in Your IRA If:

✓ You possess specialized knowledge in real estate, private equity, or other alternative sectors ✓ You’re comfortable conducting thorough due diligence without professional fund managers ✓ You have sufficient net worth ($500,000+ outside retirement accounts) to absorb potential losses ✓ You understand prohibited transaction rules and can maintain strict compliance ✓ You seek diversification beyond publicly-traded securities ✓ You have time to actively manage investments and handle custodial paperwork ✓ Your investment horizon extends 7+ years before needing retirement distributions

Stick with Traditional IRAs and Public Market Investments If:

✗ You lack expertise in evaluating private deals, real estate, or alternative opportunities ✗ You prefer passive, set-it-and-forget-it retirement investing ✗ You have limited assets ($100,000 or less) where fees and complexity outweigh benefits ✗ You need maximum liquidity or anticipate requiring early withdrawals ✗ You’re uncomfortable with illiquid investments and valuation uncertainty ✗ You’re approaching retirement (within 5 years) when RMDs create forced liquidation pressure

For most investors, a traditional IRA holding low-cost index funds (stocks, bonds, REITs) provides sufficient diversification, minimal fees, maximum liquidity, and strong long-term returns without prohibited transaction risks or administrative complexity.

However, for sophisticated investors with alternative asset expertise, self-directed IRAs unlock powerful tax-advantaged wealth-building opportunities unavailable through conventional retirement accounts. The key is matching your capabilities, risk tolerance, and investment timeline to the alternative asset approach.

Key Takeaways

- Self-directed IRAs permit alternative asset investments including real estate, precious metals, private equity, cryptocurrencies, and more—providing diversification beyond traditional stocks and bonds available in conventional retirement accounts.

- Tax advantages remain powerful: Traditional SDIRAs offer tax-deferred growth with distributions taxed as ordinary income at retirement; Roth SDIRAs provide completely tax-free growth and qualified withdrawals after age 59½.

- Specialized custodians are required for SDIRAs, charging annual fees of $295-$595 plus transaction fees of $50-$125 per purchase or sale—significantly higher than $0-cost traditional IRA providers like Vanguard or Fidelity.

- Prohibited transaction rules create severe penalties: Self-dealing, family involvement, personal use of IRA assets, or mixing personal and IRA funds can disqualify your entire IRA, triggering full taxation plus 10% early withdrawal penalties potentially costing $50,000-$200,000.

- Illiquid alternative assets complicate Required Minimum Distributions starting at age 73—maintain 20-30% of SDIRA in liquid investments to fund RMDs without forced sales of real estate or private equity at unfavorable times.

- Due diligence is entirely your responsibility: Custodians don’t vet investments, making SDIRA investors targets for fraudulent schemes offering unrealistic returns—verify every opportunity through independent research before committing retirement capital.

- Alternative assets work best for investors with specialized knowledge, $500,000+ in total assets, 7+ year investment horizons, and willingness to handle administrative complexity—most investors achieve better results with low-cost traditional IRAs holding diversified index funds.

- UBIT (Unrelated Business Income Tax) applies to debt-financed real estate income and active business operations within IRAs—reducing or eliminating tax advantages for leveraged investments and requiring Form 990-T filings with associated compliance costs.

What types of alternative assets can I hold in a self-directed IRA?

Self-directed IRAs can hold nearly any investment except collectibles (art, rugs, antiques, gems), life insurance, and S-corporation stock under IRS regulations. Permitted alternative assets include real estate (residential, commercial, raw land, REITs), precious metals (IRS-approved gold, silver, platinum, palladium), private equity and venture capital, private placements and promissory notes, tax liens and deeds, cryptocurrencies, foreign currency, and energy investments like oil/gas partnerships. Each asset class has specific rules—precious metals must meet purity standards and be stored in approved depositories, real estate cannot be used personally or rented to family members, and private companies cannot be entities where you serve as an officer or director. The IRS permits these investments but doesn’t endorse them, placing full due diligence responsibility on the IRA owner.

How much does it cost to set up and maintain a self-directed IRA for alternative assets?

Initial setup fees range from $50 to $300 depending on the custodian and account complexity. Annual maintenance fees typically run $295-$595 for basic accounts, with some custodians charging sliding-scale fees based on total asset value (0.05%-0.50% annually for accounts exceeding $1 million). Transaction fees apply each time you direct a purchase, sale, or payment from your IRA—expect $50-$125 per transaction. Real estate investments incur additional costs: title and closing fees ($800-$2,000), annual property taxes and insurance (paid from IRA), property management fees (8-12% of gross rent), and maintenance costs (all paid from IRA funds). Precious metals storage adds $125-$250 annually plus dealer spreads of 2-5% over spot prices. When comparing costs, a traditional IRA at Vanguard charges $0 in annual fees and $0 per trade for ETFs, while a self-directed IRA might cost $800-$1,500 annually before considering asset-specific expenses—making economic sense only for investors with substantial accounts ($50,000+ minimum, preferably $100,000+) where percentage costs become manageable.

Can I transfer my existing 401(k) or traditional IRA to a self-directed IRA for alternative assets?

Yes, you can transfer or rollover existing retirement accounts to self-directed IRAs while maintaining tax-advantaged status. Direct trustee-to-trustee transfers from an IRA to an SDIRA incur no taxes or penalties and have no time limits—the funds move directly between custodians. Rollovers from 401(k) plans to SDIRAs work similarly once you separate from employment or your plan allows in-service rollovers (check with your benefits department). If your employer 401(k) doesn’t permit in-service distributions, wait until changing jobs or retiring to rollover funds. Roth 401(k) and Roth IRA funds must roll into Roth SDIRAs to preserve tax-free status; Traditional 401(k) and Traditional IRAs roll into Traditional SDIRAs. The process typically takes 5-10 business days for direct transfers and up to 3 weeks for 401(k) rollovers involving paper checks. Critical rule: Never take personal possession of funds during the rollover, as this creates a taxable event and 60-day deadline to complete the rollover. Instead, request direct trustee-to-trustee transfers where your current custodian sends funds directly to your new SDIRA provider. You can rollover unlimited amounts, but annual contribution limits ($7,000 for 2026 if under 50) still apply to new contributions beyond transferred funds.

What happens if I accidentally trigger a prohibited transaction in my self-directed IRA?

Prohibited transactions disqualify your entire IRA retroactive to January 1st of the year the violation occurred, treating the full account balance as distributed. You owe ordinary income tax on the entire amount plus a 10% early withdrawal penalty if you’re under age 59½. For a $200,000 IRA in the 24% federal tax bracket plus 5% state taxes, the penalty totals approximately $58,000 federal tax, $10,000 state tax, and $20,000 early withdrawal penalty—$88,000 total, leaving you with $112,000 after-tax. Common violations include renting IRA property to your children, personally repairing IRA-owned real estate, using an IRA vacation home even briefly, buying assets from your IRA at below-market prices, or providing services to IRA-owned businesses. If you discover a prohibited transaction, immediately consult a CPA specializing in retirement accounts and an ERISA attorney. The IRS Voluntary Compliance Program potentially reduces penalties if you self-report violations before audit. Correction procedures exist for certain violations if caught early: unwinding the transaction, paying excise taxes on the amount involved (15% initially, 100% if not corrected), and restructuring to prevent recurrence. Prevention beats correction—when any transaction seems potentially prohibited, pay $300-$500 for professional guidance rather than risking $50,000-$200,000 in penalties.

How do Required Minimum Distributions work with illiquid alternative assets in my IRA?

Traditional IRAs require minimum distributions starting at age 73, calculated as account balance divided by IRS life expectancy tables—approximately 3.5%-4% at age 73, increasing annually. With illiquid alternative assets like real estate or private equity, you have three options: (1) Maintain sufficient liquid holdings (20-30% in money market funds, stocks, or bonds) to fund annual RMDs without selling alternatives; (2) Generate enough income from alternative assets to cover RMDs—rental properties producing 6-8% cash-on-cash returns can fund distributions while preserving the underlying asset; (3) Distribute assets in-kind, transferring ownership from your IRA to personal ownership and paying taxes on fair market value. The third option works for real estate—your IRA deeds the property to you personally, you owe income tax on its appraised value, but you now own it outright outside the IRA. For private equity or other partnership interests, in-kind distributions may violate fund agreements or be impractical. Roth IRAs avoid this problem entirely—no RMDs during your lifetime, making them ideal for illiquid alternatives if you can afford the upfront tax cost of Roth conversions. Plan ahead: Don’t allocate 100% of traditional IRAs to 7-10 year lockup investments if RMDs begin during that period, or you’ll face forced sales at potentially unfavorable prices to meet distribution requirements.

Are real estate rental properties in self-directed IRAs subject to UBIT (Unrelated Business Income Tax)?

Real estate rental income is generally NOT subject to UBIT when properties are purchased entirely with IRA funds without financing. The IRS considers rental real estate a passive investment producing tax-deferred income in IRAs. However, debt-financed real estate triggers UBIT under IRC Sections 511-514 on the leveraged portion. If you purchase a $300,000 property with $200,000 IRA cash and a $100,000 non-recourse loan, 33% of net rental income and eventual capital gains face UBIT. The calculation uses average debt percentage during the year. For example: property generates $24,000 net income with 33% average debt = $8,000 subject to UBIT taxed at trust tax rates (10% on first $2,900, 24% on $2,900-$9,850, 35% on $9,850+), resulting in approximately $1,900 UBIT owed by the IRA. Your IRA files Form 990-T and pays this tax from IRA funds, reducing tax-advantaged growth. Strategic planning minimizes UBIT: purchase properties entirely with IRA funds when possible, pay down debt over time to reduce the leveraged percentage, or accept UBIT as worthwhile if leverage significantly improves returns (earning 12% gross returns with UBIT might outperform 6% unleveraged returns after accounting for the tax). Note: Operating an active real estate business (frequent flips, development, property management services) could trigger full UBIT even without debt, but passive buy-and-hold rental properties avoid this issue.

Can I invest my self-directed IRA in a business I own or operate?

No—investing IRA funds in businesses where you’re an owner, officer, director, or employee constitutes a prohibited transaction under IRC Section 4975. You cannot use your IRA to invest in your own LLC, corporation, partnership, or any entity where you have more than 10% ownership or provide substantial services. This extends to businesses owned by your spouse, children, grandchildren, parents, or grandparents—all disqualified persons under IRS rules. The rationale: IRAs exist for retirement savings, not current self-dealing benefits. If your IRA invests in your business, you’re essentially using tax-advantaged funds to support your own commercial activities while extracting benefits (salary, control, business value growth you influence directly). Violation penalties include full IRA disqualification, immediate taxation of the entire account balance, and 10% early withdrawal penalties if you’re under 59½. Indirect violations also occur: your IRA cannot invest in a friend’s business if you later join as an employee or consultant, creating a prohibited transaction retroactively. However, you CAN invest IRA funds in businesses where you have no ownership, fiduciary role, or employment relationship—private placements in companies you don’t control, crowdfunding opportunities in third-party ventures, or shares in corporations where you’re a passive investor. Always consult an ERISA attorney before investing IRA funds in any business where you might have current or future connections.

What are the best alternative assets for a Roth IRA versus a Traditional self-directed IRA?

Roth IRAs work best for high-growth alternative assets expected to appreciate significantly, since qualified withdrawals are completely tax-free after age 59½ and five years of account ownership. Ideal Roth SDIRA investments include: early-stage private equity or venture capital (high risk but potential 10x-50x returns, all tax-free if successful), cryptocurrency (volatile but historically explosive growth, avoiding capital gains taxes on trading), high-appreciation real estate markets (converting $200,000 properties into $800,000 assets over 20-30 years tax-free), and growth-focused alternatives over income-producing assets (since you pay no tax on withdrawal regardless). Traditional SDIRAs suit alternative assets generating substantial current income you want to defer taxation on until retirement when you might be in lower brackets. Ideal Traditional SDIRA investments include: rental real estate in stable markets (deferring 6-8% annual rental income, paying tax at retirement when income may drop), private debt or lending (interest income taxed at ordinary rates anyway, deferring to retirement), and income-focused alternatives over pure appreciation plays. Strategic consideration: pay Roth taxes now on $50,000 that might grow to $500,000, or defer Traditional IRA taxes on $50,000 that might grow to $150,000? Higher potential growth justifies Roth’s upfront tax cost. Also consider: Roths have no RMDs during your lifetime, making them superior for illiquid alternatives you plan to hold long-term or pass to heirs through inherited IRAs with continued tax-free growth.

Disclaimer

This article provides educational information about self-directed IRAs and alternative assets for general knowledge purposes only. It does not constitute financial, tax, legal, or investment advice tailored to your specific situation. Self-directed IRA rules are complex, and prohibited transaction violations carry severe penalties including full account disqualification and substantial tax liabilities. Before investing in alternative assets through an IRA, consult with: (1) a Certified Public Accountant (CPA) specializing in self-directed retirement accounts for tax implications, UBIT considerations, and IRS compliance; (2) an ERISA attorney for prohibited transaction guidance and legal structuring; (3) a Certified Financial Planner (CFP) or registered investment advisor for suitability analysis and portfolio allocation recommendations. Investment returns mentioned in examples are historical and do not guarantee future results. Alternative assets carry significant risks including illiquidity, valuation uncertainty, total loss of capital, fraud, and opportunity costs. The IRS permits alternative IRA investments but does not endorse them or verify their quality. Due diligence is solely your responsibility. Last updated February 8, 2026.

As the Founder and Chief Investment Officer of Bullionite and Bullionite Asset Group, I’ve built my career on a simple premise understanding the intersection of macroeconomics, commodities, and digital assets to stay ahead of the curve, not under it. My focus is on navigating the complexities of the world’s largest markets spanning the US, the Middle East, and Asia to identify high-value opportunities for alternative investment.

With a specialized focus on Self-Directed IRAs (SDIRAs), I help investors move beyond traditional 401ks by integrating assets like precious metals and cryptocurrency into their retirement strategies. Based in Newport Beach, California, I am dedicated to bridging the gap between traditional finance and the evolving landscape of new age digital assets, ensuring that every strategic move is backed by deep market insight and a commitment to long-term growth.