How to Invest in Precious Metals IRA: A Step-by-Step 2026 Guide to Buying IRS-Approved Gold, Silver, Platinum & Palladium

TL;DR

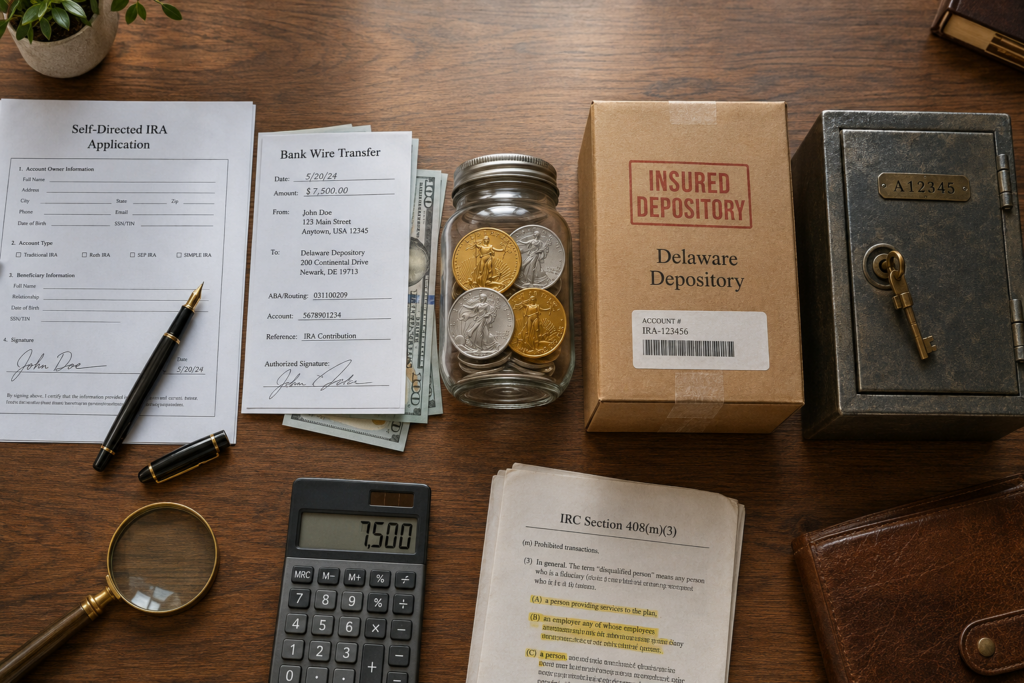

To invest in a precious metals IRA you open a self directed precious metals IRA with a specialized custodian, fund it through a contribution, transfer, or 401k to precious metals IRA rollover, then purchase IRS-approved gold, silver, platinum, or palladium that meets the fineness rules under IRC Section 408(m)(3) and have it shipped directly to an approved third-party depository. The 2026 contribution limit is $7,500 ($8,600 if you are 50 or older). Gold has to be at least .995 fine, silver .999, platinum and palladium .9995. Home storage is treated as a taxable distribution. Expect setup costs of $50 to $200, annual administrative fees of $75 to $300, and storage of $100 to $300 per year.

What Is a Precious Metals IRA?

A precious metals IRA is a self-directed individual retirement account that holds physical gold, silver, platinum, or palladium instead of (or alongside) the paper assets you would find in a brokerage IRA. The IRS classifies physical bullion as an “alternative asset,” so a regular Vanguard or Fidelity IRA cannot custody it for you. You need a self-directed IRA administered by a custodian that is approved to hold physical metal under IRC Section 408(m)(3).

The account itself is the same wrapper you already know. Traditional or Roth, with the same contribution limits, the same required minimum distribution age, and the same early-withdrawal penalty. What changes is what is inside it. Instead of an S&P 500 index fund, you own bars and coins that meet the IRS purity standard, sit in an insured depository under your IRA’s name, and can be physically delivered to you at retirement if you want.

How to Invest in Precious Metals IRA: The 7-Step Setup Process

Here is the exact sequence we walk Bullionite clients through. Every step is mandatory. Skipping any one of them is the most common reason new precious metals IRA investors trigger a taxable event in their first year.

Step 1. Decide which type of account fits your tax goal

Before you open anything, decide between a Traditional and a Roth precious metals IRA. With a Traditional account you deduct the contribution today and pay ordinary income tax on the back end. With a Roth IRA precious metals account you pay tax now and the metals grow tax-free for life. If you expect gold and silver to appreciate substantially over your holding period, the Roth structure is usually the more tax-efficient wrapper.

Step 2. Choose a self-directed precious metals IRA custodian

Open your account with a custodian that is approved to hold IRC 408(m)(3) bullion. This is not a step where you shop on price alone. The custodian is your legal record-keeper with the IRS, processes every buy and sell, and handles the chain of custody between you, the dealer, and the depository. Use our best self-directed IRA custodian comparison for 2026 to vet the leading options on fees, response time, and audit history.

Step 3. Fund the account

You have three legal funding paths:

- New contribution. Up to $7,500 in 2026, or $8,600 if you are 50 or older, per the IRS contribution limits page.

- Direct trustee-to-trustee transfer. Move funds from one IRA to your new self directed precious metals IRA without ever taking constructive receipt. No reporting, no 60-day clock.

- Most clients fund via a 401k to precious metals IRA rollover from a former employer’s plan. A direct rollover is the cleanest route. A 60-day indirect rollover puts the IRS deadline on you and risks 10% withholding. Our walkthrough on how to roll over a 401k into a self-directed IRA covers both routes in full.

Step 4. Pick your dealer and choose IRS-approved metals

Once the funds settle in your IRA, your custodian will let you place a buy order with a precious metals dealer of your choice. The dealer has to invoice your IRA (not you personally) and ship directly to your depository. Choose from gold, silver, platinum, and palladium that meet the fineness rules in the next section. For metal-specific shopping guides, see what is a gold and silver IRA, self-directed IRA gold coins, buy silver in IRA, how to open a platinum IRA, and what is a palladium IRA.

Step 5. Direct the custodian to wire payment

You sign a buy direction letter, the custodian wires the dealer from your IRA cash balance, and the dealer ships the bullion to the depository named on the order. You never touch the metal. Touching it, even for a photo, is a distribution.

Step 6. Confirm storage and delivery at the depository

The depository receives, weighs, and logs the metal under your IRA’s account number. You will get a holdings statement showing serial numbers (for segregated storage) or the pooled inventory (for non-segregated). Bullionite usually recommends segregated storage when the premium is reasonable. You get back the exact bars you bought, not equivalent ones.

Step 7. Track holdings and rebalance over time

Your custodian will value the account quarterly using a market-recognized spot price. You can buy more, sell, or take an in-kind distribution at retirement. If you ever decide to consolidate, you can also convert your IRA to silver, shift into platinum, or rotate out of metals entirely back into cash inside the IRA wrapper.

Which Precious Metals Are IRA Eligible?

Not every bullion product qualifies. Under IRC Section 408(m)(3), the IRS only allows bullion that meets a strict fineness floor and is produced by a national mint or an accredited refiner (NYMEX, COMEX, LBMA, LME, NYSE/Liffe, or ISO 9000-certified).

|

|

|

|

|

Gold |

.995 (99.5%) |

American Gold Eagle*, American Gold Buffalo, Canadian Gold Maple Leaf, Austrian Philharmonic, PAMP Suisse / Credit Suisse / Valcambi bars |

|

Silver |

.999 (99.9%) |

American Silver Eagle, Canadian Silver Maple Leaf, Austrian Silver Philharmonic, Royal Canadian Mint silver bars |

|

Platinum |

.9995 (99.95%) |

American Platinum Eagle, Canadian Platinum Maple Leaf, Australian Platinum Koala, approved bars |

|

Palladium |

.9995 (99.95%) |

Canadian Palladium Maple Leaf, approved bars from accredited refiners |

\*The American Gold Eagle is the only major exception to the .995 rule. It is 22-karat (.9167 fine), but Congress wrote a specific carve-out for it (and the Silver Eagle) directly into the tax code, per IRS guidance on investments in collectibles.

What is not allowed: rare coins, numismatics, graded coins, pre-1933 U.S. gold, South African Krugerrands (below the gold purity threshold), British Sovereigns, jewelry, and any product not produced by a recognized mint or refiner. If a dealer is pushing “rare proof” coins for your IRA, walk away. The Commodity Futures Trading Commission has a long-standing advisory about this exact pitch.

For a deeper read on the purity standard, see what does IRA-eligible silver mean and self-directed IRA gold coins.

Precious Metals IRA Rules You Cannot Break

A precious metals IRA is generous in what it allows you to own. The IRS is strict about how you own it. These are the core precious metals IRA rules every account holder needs to memorize:

- No physical possession. Section 408(m) requires “physical possession” by a qualified trustee. The day you take the bars home, the IRS treats the entire account value as a distribution.

- No prohibited-party transactions. You cannot buy metal from yourself, your spouse, your parents, your kids, or any entity you control. Same applies on the sell side. See our self-directed IRA prohibited transactions guide for the full list.

- Approved depository only. Storage must happen at a third-party depository approved by your custodian. We unpack this in gold IRA storage rules and why home storage doesn’t work.

- Fineness compliance. Every bar or coin has to meet the .995/.999/.9995 standards (with the Eagle exception above).

- Annual contribution cap. Combined Traditional + Roth contributions in 2026 cannot exceed $7,500 ($8,600 at age 50+).

- Required Minimum Distributions (RMDs) at 73. Traditional precious metals IRAs are subject to RMDs. You can satisfy them in cash or as an in-kind distribution of metal.

- UBIT rarely applies, but file Form 990-T if it does. If your IRA invests through certain leveraged structures, see our notes in self-directed IRA tax filing requirements.

The IRS’s own page on investments in collectibles is the primary source for the bullion exemption. Read it once before you open the account.

How to Fund the Account: Rollover, Transfer, or Direct Contribution

Most precious metals IRA balances are not built from $7,500 contributions. They are built from rollovers of existing retirement money. Here is how each option compares.

|

|

|

|

|

|

|

Direct rollover |

Old 401(k), 403(b), TSP |

No |

1 to 3 weeks |

Job changers, retirees |

|

Trustee-to-trustee transfer |

Existing Traditional or Roth IRA |

No |

5 to 10 business days |

Consolidating IRAs |

|

Indirect (60-day) rollover |

Any qualified plan |

No, if you redeposit within 60 days |

Immediate access |

Avoid unless necessary |

|

New contribution |

Earned income |

Deductible (Traditional) or after-tax (Roth) |

Same day |

Building Roth basis |

|

In-kind transfer of bullion |

Existing precious metals IRA |

No |

2 to 4 weeks |

Switching custodians |

A direct trustee-to-trustee rollover is the route we recommend in 90% of cases. There is no withholding, no 60-day window, and no chance of accidentally tripping the once-per-year indirect rollover rule.

If your funds are currently in a 401(k), the route we cover in detail is the 401k to precious metals IRA rollover. If you are already in an IRA.

How Much Does a Precious Metals IRA Cost? Real Fee Breakdown

Precious metals IRA fees are higher than a vanilla brokerage IRA because someone has to physically hold the metal. They are not unreasonable, but you should know the line items before you open the account.

|

|

|

|

|

Account setup (one-time) |

$50 to $200 |

Some custodians waive this on rollovers above a threshold |

|

Annual custodial / administrative |

$75 to $300 |

Often a flat fee, not percentage-based, so small accounts pay disproportionately |

|

Annual storage (segregated) |

$150 to $300 |

Higher than commingled because your bars are kept separate |

|

Annual storage (non-segregated) |

$100 to $150 |

Pooled storage; the metal returned is “like kind” not exact |

|

Dealer premium over spot |

2% to 8% |

Lowest on standard bars, highest on collectible-style coins (avoid those) |

|

Wire / transfer fees |

$25 to $40 per transaction |

Usually waived on the funding wire |

The premium over spot is where most investors quietly overpay. A reputable dealer should price American Gold Eagles at roughly 4 to 6% over spot in normal market conditions. A 12%+ premium on a “rare proof” coin is a sign you are being pitched a numismatic product the IRS would never accept anyway.

For more on minimizing fees and avoiding upsells, see our silver IRA reviews and sd401k vs SDIRA for precious metals breakdown.

Choosing a Precious Metals IRA Custodian

Among the best precious metals IRA custodians, the differentiators that actually matter are:

- Years in the SDIRA business. A 20-year track record means they have weathered a full audit cycle.

- Insurance behind the depository. Look for Lloyd’s of London or comparable underwriters at the storage facility.

- Transparent fee schedule. Flat-fee custodians beat asset-based custodians once your balance crosses about $50,000.

- Speed of buy execution. A custodian that takes ten business days to wire a buy order will cost you on rising-price days.

- No commission relationship with a single dealer. You want to be free to shop dealers. Custodians who lock you to one dealer are usually being paid by that dealer.

We do not recommend custodians that also act as the dealer. The conflict of interest is structural, and it shows up in premiums.

Can You Open a Precious Metals IRA at Fidelity, Schwab, or Vanguard?

Short answer: not in the way most people think. The big retail brokerages will not custody physical bullion in your IRA the way an SDIRA custodian will. Fidelity, Schwab, and Vanguard offer access to gold through ETFs (GLD, IAU, SGOL), gold mutual funds, and mining stocks inside any standard IRA. None of them act as the trustee for IRA-owned physical bars or coins under IRC 408(m)(3).

Fidelity is the one partial exception. It allows certain bullion products (American Gold Eagles, Silver Eagles, Platinum Eagles) to be transacted through its FideliTrade subsidiary inside a Fidelity brokerage account. That is closer to a metals trading account than a true self directed precious metals IRA with depository storage in your IRA’s name.

|

|

|

|

|

|

Fidelity |

Limited (via FideliTrade, narrow product list) |

Gold ETFs, gold mutual funds, mining stocks |

Roll over to a specialty SDIRA custodian |

|

Charles Schwab |

No |

Gold ETFs, mutual funds, mining stocks |

Roll over to a specialty SDIRA custodian |

|

Vanguard |

No |

Gold ETFs, mining stocks |

Roll over to a specialty SDIRA custodian |

|

Specialty SDIRA custodians (Equity Trust, STRATA, Equity Institutional, Madison Trust) |

Yes |

Physical gold, silver, platinum, palladium under IRC 408(m)(3) |

Open directly |

If your retirement money sits at one of the big three today, the path forward is a trustee-to-trustee transfer or rollover into a self-directed account. The mechanics are walked through in our how to open a self-directed IRA guide.

Best Precious Metals IRA Companies for 2026: How the Top Custodians and Dealers Compare

The precious metals IRA industry has two roles, and they are best kept separate: the custodian (the trust company that holds your IRA) and the dealer (the company that sells you the metal). Some firms try to play both. We do not recommend that setup because the buyer protection you get from arm’s-length pricing disappears.

Top precious metals IRA custodians (trustee role):

- Equity Trust Company

- STRATA Trust Company

- Equity Institutional

- Madison Trust Company

- Kingdom Trust Company

- The Entrust Group

These are trust companies with multi-decade SDIRA records and audited fee schedules. None of them sells metal to you, which is the point.

Bullion dealers you’ll see most often in precious metals IRA reviews:

- Augusta Precious Metals

- Goldco

- APMEX

- Birch Gold Group

- Noble Gold Investments

- US Money Reserve

You will encounter these names in nearly every “best precious metals IRA companies” roundup online. The honest framing is that quality varies by transaction, not by brand. A reputable dealer can still over-charge a specific buyer on a specific coin.

What we look at when vetting any precious metals IRA company:

- BBB rating plus the substance of complaints (not just the count)

- Premium quoted on standard products like American Gold Eagles and Silver Eagles

- A written buyback policy with a defined spread

- Whether the rep pushes you toward “rare,” “premium,” or numismatic coins (a major red flag, since those usually fail IRS purity rules anyway)

- Whether they accept your custodian of choice or insist you use theirs

- Audit history and assets under custody (for the trustee side)

For an apples-to-apples breakdown of the leading custodians on fees, response time, and audit history,

Storage Requirements: Why You Cannot Store a Gold IRA at Home

The “home storage precious metals IRA” pitch is one of the most aggressively marketed and most legally dangerous ideas in this industry. The IRS has been clear, and the Tax Court reinforced it in McNulty v. Commissioner (2021), where a couple was hit with a six-figure tax bill plus penalties for keeping their IRA-owned American Eagles in a home safe.

Here is what is required:

- Metal has to be held by a “qualified trustee” — a bank, a federally insured credit union, or an IRS-approved non-bank trustee.

- Storage has to be at an IRA-approved precious metals depository such as Delaware Depository, Brink’s Global, IDS of Texas, or HSBC London.

- You can choose segregated (your bars, your box, your serial numbers) or commingled (pooled inventory of identical metal). Segregated costs more but gives you back the exact bullion you bought.

If anyone offers you a “home storage IRA” or a “checkbook IRA LLC” with metals stored personally, walk away. The structure has been rejected in court.

Tax Treatment of a Precious Metals IRA (Traditional vs. Roth)

How your gains are taxed depends entirely on which IRA wrapper you choose.

- Traditional precious metals IRA. Contributions may be deductible. Growth is tax-deferred. Withdrawals are taxed as ordinary income, not at the 28% collectibles rate that applies to physical gold held outside an IRA. RMDs begin at age 73.

- Roth IRA precious metals. Contributions are after-tax. Qualified withdrawals after age 59½ (and a 5-year clock) are 100% tax-free, including all appreciation. No RMDs during your lifetime.

The Roth wrapper is especially powerful for an asset class where you expect long-term appreciation. If gold doubles over a 15-year holding period inside a Roth, you owe $0 on that gain. The same gain in a Traditional IRA is taxed at your retirement-year ordinary income rate.

A note on capital gains. Outside of an IRA, the IRS classifies physical bullion as a “collectible” and taxes long-term gains at up to 28% per Topic No. 409. Inside an IRA, that 28% collectibles rate does not apply. Another reason the IRA wrapper is the most tax-efficient way to hold physical metal long term.

Precious Metals IRA vs. Physical Gold vs. Gold ETF: Which Path Wins?

Three legal ways to own gold for retirement. Each one has different tax treatment, liquidity, and access to the actual metal.

|

|

|

|

|

|

Owns physical metal? |

Yes, in approved depository |

Yes, in your possession |

No, paper claim on metal |

|

Tax-advantaged? |

Yes (Traditional or Roth) |

No |

Only if held inside an IRA |

|

Long-term capital gains rate |

Ordinary income on Traditional withdrawal; tax-free on qualified Roth |

28% collectibles rate |

28% collectibles rate (per IRS guidance on physically-backed metal ETFs) |

|

Annual fees |

$250 to $600 plus storage |

$0 (or your safe / insurance cost) |

0.17% to 0.40% expense ratio |

|

Counterparty risk |

Depository risk (fully insured) |

None |

ETF sponsor + custody bank risk |

|

Liquidity |

5 to 10 business days to cash |

Immediate (local dealer) |

Same-day (market hours) |

|

Take physical delivery? |

Yes, at distribution |

Already in hand |

No (most cash-settle) |

The decision usually comes down to two questions. Do you want the tax wrapper? Then it is a precious metals IRA. Do you want immediate physical possession? Then it is bullion outside an IRA. Gold ETFs are best thought of as exposure to the gold price rather than gold ownership. They are convenient and they fail the moment you actually want metal in your hand.

For deeper allocation framing, see our precious metals SDIRA diversification benefits 2026 guide.

Pros and Cons of a Precious Metals IRA

Pros

- Diversification away from stocks, bonds, and the dollar

- Physical asset with no counterparty risk

- Tax-deferred or tax-free growth (Roth)

- Avoids the 28% collectibles capital gains rate that applies outside an IRA

- Hedge against inflation and currency debasement

- Portable, durable, and globally recognized at retirement

Cons

- Higher annual fees than a brokerage IRA

- No yield. Metals do not pay interest or dividends

- Storage requirement removes the “I can hold it” appeal until you take an in-kind distribution

- Dealer premiums and bid/ask spreads reduce short-term liquidity

- Requires a self-directed custodian and dealer due diligence

For our long-form take on whether the wrapper is worth it for your situation, see are gold IRAs a good idea.

Are Precious Metals IRAs Safe? Risk and Volatility Profile

“Safe” depends on what you mean.

Custody safety. When held at an approved depository, your bullion is fully insured (Lloyd’s of London or comparable underwriters), audited, and stored in vaults with armed security. Custody risk inside the IRC 408(m)(3) framework is among the lowest in the financial system.

Price volatility. Gold is not a low-volatility asset. From 2011 to 2015 spot gold lost roughly 40% of its value. From 2018 to 2020 it doubled. From 2020 to 2022 it traded sideways while inflation accelerated. Silver is more volatile than gold. Platinum and palladium are more volatile still, with industrial demand drivers that make them harder to forecast than the monetary metals.

Counterparty risk. Effectively zero on physical bullion held in an IRA-titled depository account. The metal is in your IRA’s name. Compare this to ETFs, where you hold a paper claim on a sponsor’s balance sheet.

Regulatory risk. Low. The 408(m)(3) framework has been in place since 1997 and has only loosened over time, not tightened.

Concentration risk. This is the real one. If you put 80% of your retirement into a single asset class, gold or otherwise, you are running concentration risk. The institutional 5 to 10% allocation guidance exists precisely to manage that.

A precious metals IRA is not “safe” the way a 1-year Treasury is safe. It is a hedge asset. The honest framing is that it zigs when stocks zag, and held in proportion it tends to lower portfolio volatility over multi-decade periods.

How to Take Withdrawals From a Precious Metals IRA

You have two choices when it is time to access the metal:

- Cash distribution. The depository sells the bullion at the prevailing spot price (less the dealer’s bid spread), and your custodian wires you the cash. Same tax treatment as any IRA withdrawal.

- In-kind distribution. The depository ships the physical bars or coins to your home address. You report the fair market value as a distribution on the date of shipment. Now the metal is yours, outside the IRA, and any future appreciation falls under the collectibles rate when sold.

Most retirees take a blend. Partial in-kind for the legacy and portability appeal of holding the metal, partial cash to satisfy the RMD without shipping risk.

For Roth holders, qualified withdrawals are tax-free in either form. For Traditional holders, the value of the in-kind distribution is added to that year’s ordinary income.

How to Sell or Liquidate Bullion Inside a Precious Metals IRA

Selling bullion inside the IRA is different from taking a withdrawal out of the IRA. Sales inside the wrapper do not trigger any tax. Withdrawals do.

To sell metal inside your precious metals IRA:

- Notify your custodian and request a sell direction form.

- Your custodian quotes you a price from the dealer (or from a competing dealer if you’re free to shop).

- You sign the form. The depository releases the metal to the dealer. The dealer wires cash back into your IRA cash balance.

- The cash sits in your IRA. You can buy different metals, hold cash, or take a distribution.

Things worth knowing before you sell:

- Bid/ask spread. You’ll get the dealer’s bid, which is below the spot price. The spread is typically 1 to 3% on standard bars and Eagles, wider on collectible coins (one more reason to avoid them on the way in).

- Buyback policy. Reputable dealers commit to a buyback at a defined spread. Get this in writing before your initial buy, not when you’re trying to exit.

- Settlement time. Cash typically lands in your IRA within 3 to 7 business days of the dealer receiving the metal.

- Partial sales are fine. You can sell one bar and leave the rest. There is no requirement to liquidate the whole position.

Selling is also the route for swapping between metals. Investors often rotate from silver into gold (or the reverse) over time as relative valuations shift. The IRA wrapper makes this rotation tax-free, so long as the proceeds stay inside the account.

If you’re exiting the precious metals IRA entirely, sell to cash inside the IRA first, then take a normal cash distribution under the rules of your IRA type. That sequence is cleaner than an in-kind distribution followed by an outside sale, which exposes you to the 28% collectibles rate on any gain after you receive the metal.

What Happens to Your Precious Metals IRA When You Die? (Beneficiary Rules)

Your precious metals IRA passes to whoever is named on the account’s beneficiary form, not to whoever is named in your will. Get the form right, and review it after every life event.

Under the SECURE Act and SECURE Act 2.0, most non-spouse beneficiaries have to fully distribute an inherited IRA within 10 years of the original owner’s death:

- Spouse beneficiary. Can roll the inherited precious metals IRA into their own IRA and keep the tax shelter for their own lifetime.

- Non-spouse beneficiary (most adult children). Has to empty the account by the end of year 10 after death. If the original owner had already started RMDs, annual distributions are also required in years 1 through 9.

- Eligible designated beneficiaries (minor children, disabled, chronically ill, beneficiaries within 10 years of the decedent’s age). Stretch rules still apply, with restrictions.

For the metal itself, the beneficiary has the same two options every IRA holder has. Liquidate to cash inside the inherited IRA and withdraw cash, or take an in-kind distribution and receive the actual bars and coins.

A common mistake we see: beneficiaries sit on inherited Traditional precious metals IRAs and bunch the entire withdrawal into year 10, blowing themselves into the highest tax bracket for that year. Spreading distributions evenly across the 10-year window almost always lowers the lifetime tax bill.

How Much of Your Retirement Should Be in Precious Metals?

This is the question every PAA chart shows being asked, and the honest answer is that it depends on your age, your other holdings, and your view on inflation. The institutional research is fairly consistent.

The World Gold Council has shown that portfolios with a 5 to 10% allocation to physical gold historically reduced volatility and improved risk-adjusted returns over multi-decade holding periods. State Street and other large asset managers tend to land in the same band. An aggressive inflation-hedge investor might run 10 to 20%. A balanced retiree typically sits at 5 to 10%. A “stocks-only forever” portfolio runs 0%.

What we tell Bullionite clients is this. Do not concentrate the entire retirement in metal. But if you have zero exposure today and you are ten years out from retirement, getting to 5 to 10% through a gradual rollover is rarely a decision people regret.

For deeper portfolio construction, see our precious metals SDIRA diversification benefits 2026 guide.

Common Mistakes to Avoid When Investing in a Precious Metals IRA

- Buying numismatic or “rare” coins. They fail the IRS purity test and trigger a deemed distribution.

- Falling for the home storage IRA pitch. Settled law since McNulty. Don’t.

- Using an indirect 60-day rollover when a direct one was available. You take on withholding risk and a hard deadline for no reason.

- Concentrating in one custodian-dealer combo. Conflicts of interest show up in premiums.

- Ignoring annual fees on a small account. A $200 fixed fee on a $10,000 account is a 2% drag every year. Either contribute more or wait until you can roll over a meaningful balance.

- Forgetting RMDs at 73. Traditional account holders must take them. Failure to take an RMD can trigger an excise tax (reduced from 50% to 25% under SECURE 2.0, still painful).

- Treating gold like a trading vehicle. Bid/ask spreads and dealer premiums make short-term flipping uneconomic. This is a multi-year hold.

Beyond Metals: Diversifying the Self-Directed IRA Wrapper

The same self-directed IRA structure that lets you hold gold also lets you hold real estate, private notes, and cryptocurrency. Investors who treat the SDIRA as a true alternative-asset wrapper often pair metals with one or two other categories:

- Pair physical metals with rental real estate through our self-directed real estate IRA 2026 guide.

- Pair physical metals with digital assets. See can you hold gold and cryptocurrency in a self-directed IRA.

The cap is the IRS contribution limit, not the asset menu.

Can You Convert a Precious Metals IRA Into a Bitcoin or Crypto IRA?

Yes. Both sit inside the self-directed IRA framework, so converting between them is a sell-and-buy transaction inside the IRA wrapper. No tax event.

The mechanics:

- Sell your bullion inside the precious metals IRA. The proceeds land in your IRA cash balance. No tax event because the funds never leave the wrapper.

- Either transfer the cash to a self-directed crypto IRA at a custodian that supports digital assets, or (if your existing custodian supports both asset classes) place a buy order for Bitcoin, Ethereum, or other supported coins.

- The crypto sits in IRA-titled cold storage at a qualified custodian.

Some self-directed IRA custodians now support both physical bullion and cryptocurrency under the same account, which removes the transfer step entirely. If you’re considering a partial allocation, you can also hold metals and crypto side by side without choosing between them. The mechanics are walked through in our cross-cluster guide on whether you can hold gold and cryptocurrency in a self-directed IRA.

The same logic runs in reverse. You can convert a Bitcoin IRA into a precious metals IRA using the same sell-cash-buy sequence inside the wrapper.

Key Takeaways

- A precious metals IRA is a self-directed IRA that holds physical gold, silver, platinum, or palladium (not paper proxies) in an IRS-approved depository.

- The 7-step process: pick the wrapper (Traditional or Roth), choose a custodian, fund via rollover/transfer/contribution, pick your dealer, buy IRA-eligible metals, ship to depository, monitor and rebalance.

- Fineness rules are non-negotiable. Gold .995, silver .999, platinum and palladium .9995, with the American Eagle as the one carve-out.

- 2026 contribution limits: $7,500 base, $8,600 if you are 50+. Most balances are built from rollovers, not contributions.

- Total annual cost for a properly run precious metals IRA is roughly $250 to $600 plus the dealer premium on the initial buy.

- Home storage is illegal under IRC 408(m). Period.

- Tax efficiency is the underrated benefit. The 28% collectibles capital gains rate is bypassed inside the IRA wrapper, and a Roth structure makes long-term appreciation entirely tax-free.

- Allocation guidance. 5 to 10% of retirement assets is the institutional consensus for a hedge allocation. Aggressive inflation hedgers run higher.

FAQ's

Is a precious metals IRA a good idea?

For investors who want a non-correlated hedge inside their retirement wrapper, yes, at a measured allocation (typically 5 to 10%). It is a portfolio insurance vehicle with tax-advantaged compounding, not a get-rich vehicle.

Can I put silver in my IRA?

Yes. Any silver bar or coin meeting the .999 fineness standard, produced by an approved mint or refiner, is eligible. American Silver Eagles are eligible by congressional carve-out even though they are slightly under that threshold by content.

Can I roll my 401k into a precious metals IRA?

Yes, if you have separated from the employer or your plan permits in-service rollovers. A direct trustee-to-trustee rollover is non-taxable and has no 60-day deadline. See our full 401k to precious metals IRA rollover guide.

Can I store my gold IRA at home?

No. The IRS requires bullion to be in the physical possession of a qualified trustee at an approved depository. Home storage was rejected in McNulty v. Commissioner. Storing IRA-owned metal at home is treated as a full distribution.

How are gold IRAs taxed?

Inside a Traditional IRA, withdrawals are taxed as ordinary income. Inside a Roth IRA, qualified withdrawals are tax-free. Importantly, the 28% collectibles capital gains rate that applies to physical gold held outside an IRA does not apply to gold held inside an IRA.

Can I own physical gold in my IRA?

Yes. That is the entire purpose of a precious metals IRA. The metal has to meet the IRS fineness rules and be stored at an approved depository under your IRA’s name.

Can I cash out a gold IRA?

Yes. The depository sells the metal at spot, your custodian wires the proceeds to you, and the distribution is taxed under the rules of your IRA type. After 59½ there is no 10% early-withdrawal penalty.

Do you pay taxes when you sell precious metals inside an IRA?

No tax event occurs when you sell metal inside the IRA. Tax is owed only when funds (or metal) are distributed out of the account.

What is the difference between a Roth IRA and a precious metals IRA?

A Roth IRA is a tax wrapper. A precious metals IRA is a self-directed account that holds physical metal. The two overlap. A Roth IRA precious metals account is a Roth IRA whose investments happen to be physical bullion, so you get Roth tax treatment on metal gains.

How quickly can I open a precious metals IRA?

Account opening takes 1 to 3 business days. Funding via direct rollover or transfer typically clears in 5 to 15 business days. The full sequence (open, fund, buy, deliver to depository) usually completes in 3 to 5 weeks.

Have Questions About Your Self-Directed IRA?

Schedule a free 15-minute consultation with Bullionite Asset Group. No pitch, no pressure, no referral commissions.

As the Founder and Chief Investment Officer of Bullionite and Bullionite Asset Group, I’ve built my career on a simple premise understanding the intersection of macroeconomics, commodities, and digital assets to stay ahead of the curve, not under it. My focus is on navigating the complexities of the world’s largest markets spanning the US, the Middle East, and Asia to identify high-value opportunities for alternative investment.

With a specialized focus on Self-Directed IRAs (SDIRAs), I help investors move beyond traditional 401ks by integrating assets like precious metals and cryptocurrency into their retirement strategies. Based in Newport Beach, California, I am dedicated to bridging the gap between traditional finance and the evolving landscape of new age digital assets, ensuring that every strategic move is backed by deep market insight and a commitment to long-term growth.