What Is a Self-Directed IRA and How Does It Work? A Complete 2026 Investor’s Guide

Quick Answer

A self-directed IRA (SDIRA) is a Traditional or Roth IRA held at a specialized custodian that allows alternative-asset investing. It gives you the same tax wrapper as any other IRA, but lets you hold real estate, precious metals, cryptocurrency, private notes, and most other legal asset classes that brokerages refuse to custody. You direct every investment. The custodian only processes paperwork and holds title.

TL;DR

- What it is: An IRS-approved retirement account that holds alternative assets (real estate, precious metals, crypto, private notes, syndications, LLCs, tax liens, and more).

- How it works: You open the account at a specialized custodian, fund it via contribution or rollover, find your own investments, direct the custodian in writing to buy them, and the custodian holds title in the IRA’s name.

- Tax treatment: Identical to a regular IRA. Traditional or Roth. Same 2025 contribution limits ($7,000 under 50, $8,000 if 50+). Same RMD age (73). Same 10% early-withdrawal penalty before 59½.

- What is allowed: Almost everything. The IRS only prohibits collectibles, life insurance, and S-corp stock by name.

- What is not allowed: Any transaction with a “disqualified person” (you, spouse, parents, kids, or any business they control). Violating this rule disqualifies the entire IRA.

- What it costs: $200 to $500 in annual custodian fees, plus per-asset and per-transaction charges. Worth it for alternative assets. Not worth it for index funds.

- Who regulates it: The IRS under IRC § 408 and § 4975. SDIRA custodians are non-bank trust companies, usually state-chartered.

What is a self-directed IRA and how does it work? A self-directed IRA (SDIRA) is a retirement account that holds the same Traditional or Roth tax status as any other IRA but allows you to invest in alternative assets like real estate, precious metals, cryptocurrency, private equity, syndications, tax liens, and private lending notes that a standard brokerage like Fidelity or Schwab will not custody. The account is “self-directed” because you, not a broker, choose every investment. The custodian’s job is administrative: hold the asset in the IRA’s name, process paperwork you submit, and report to the IRS.

That single shift, from broker-picked to investor-picked, is the entire reason SDIRAs exist. The SDIRA industry now holds an estimated $100 billion-plus in alternative assets, and the largest custodians process tens of thousands of real estate, metals, and crypto transactions every year on behalf of IRA holders who want exposure their brokerage will not give them.

What Is a Self-Directed IRA?

A self-directed IRA is a Traditional or Roth IRA held by a custodian who accepts alternative assets. The IRS has permitted IRAs to invest in alternative assets since the Employee Retirement Income Security Act of 1974 (ERISA). What changed over the decades was custodian willingness. Most major brokerages chose not to offer alternative-asset custody because their business model is built around selling proprietary mutual funds and earning trading commissions. SDIRA custodians filled the gap.

The account is not a separate tax vehicle. It is a regular IRA at a different kind of firm. Same Form 5498 reporting. Same Form 1099-R for distributions. Same 10% early-withdrawal penalty before age 59½. Same Roth conversion rules. Same five-year clock on Roth withdrawals.

What makes the account “self-directed” is that you make every buy and sell decision in writing, and the custodian executes it. They do not screen your investment choices. They do not refuse a deal because they think it is risky. Their compliance team only refuses transactions that violate IRS rules, never ones that simply look unwise.

If you are starting from zero, our overview of self-directed retirement accounts is the cleanest entry point. To compare the structure against a workplace plan, see how the SDIRA differs from a 401(k), and read our self-directed IRA vs. Roth IRA comparison before you choose a tax wrapper.

A Brief History of Self-Directed IRAs

IRAs were created by ERISA in 1974. The statute permitted any asset that was not a collectible (IRC § 408(m)) or a prohibited-transaction asset (IRC § 4975). Brokerages chose to offer narrow menus because they earned commissions on funds and trades. A small number of trust companies decided to accept whatever the IRS permitted, and the SDIRA industry was born.

The early SDIRA market was real estate. In the 2000s, precious metals custody grew sharply after the financial crisis. In the 2010s and 2020s, cryptocurrency became the third major asset class. Today the four asset categories that drive most new SDIRA accounts are real estate, precious metals, crypto, and private lending.

Self-Directed IRA vs. a Regular IRA

The difference shows up in three places: who custodies the account, what assets it can hold, and who picks the investments.

| Feature | Traditional IRA at a Brokerage | Self-Directed IRA |

| Where it lives | Fidelity, Schwab, Vanguard | Equity Trust, Madison Trust, Kingdom Trust, Strata, Entrust, IRA Financial, others |

| What it holds | Stocks, bonds, mutual funds, ETFs | Real estate, gold, silver, platinum, palladium, crypto, private notes, syndications, LLCs, tax liens |

| Tax treatment | Same as IRA (Traditional or Roth) | Identical (same Roth/Traditional rules) |

| 2025 contribution limit | $7,000 (<50), $8,000 (50+) | Same |

| RMD age | 73 (Traditional) | 73 (Traditional) |

| Annual fees | Often $0 | $200 to $500 base, plus per-asset and per-transaction fees |

| Who picks investments | The brokerage offers a menu | You |

| Investment advice | Available (some platforms) | None from the custodian |

| Prohibited-transaction risk | Low (limited menu) | Higher (more flexibility, more rope) |

The fees are real. SDIRA custodians charge for the work they actually do. Recording deeds. Wiring funds to escrow. Holding bullion in a depository. Signing paperwork at closings. If you only plan to buy index funds, do not open an SDIRA. The fee math does not work. SDIRAs make sense when the asset you want to buy is not available at a brokerage at all.

For a deeper read on which IRA type gives you the broadest investment universe, see our breakdown of IRAs with the most investment flexibility.

Who Offers Self-Directed IRAs?

Specialized non-bank trust companies. The largest names in the U.S. market are Equity Trust Company, Madison Trust, Kingdom Trust, Strata Trust Company, The Entrust Group, IRA Financial Trust, Pacific Premier Trust, Provident Trust, and Millennium Trust Company. Most are state-chartered trust companies regulated by their state banking departments and reported to the IRS as IRA custodians under IRC § 408.

A handful of national banks and trust banks offer SDIRA services, but their offerings are generally narrower. Major retail brokerages (Fidelity, Schwab, Vanguard, E*TRADE, Merrill, TD Ameritrade, Charles Schwab) do not custody alternative assets through their public IRA accounts. Picking the right custodian for your asset class matters more than most investors realize. We rank the major players in our 2026 best SDIRA custodian comparison for real estate, precious metals, and alternative assets, and the questions to ask before signing are in our checklist on how to determine the best self-directed IRA custodian for your investment goals.

Why Most Brokerages Don’t Offer Self-Directed IRAs

Two reasons. First, alternative-asset custody is operationally heavy. A brokerage that holds 100,000 IRA accounts in stocks can run on automated systems. The same brokerage holding 100,000 IRA accounts with rental properties would need title clerks, escrow officers, and a deed-recording process in every state. The economics do not work at scale unless the firm specializes.

Second, alternative assets do not generate trading commissions or fund-management fees. A brokerage earns nothing from a real estate IRA after the wire goes out. SDIRA custodians charge flat administrative fees instead, which is a fundamentally different revenue model.

How Does a Self-Directed IRA Work?

A self-directed IRA works in five stages. You open the account, you fund it, you find an investment, you direct the custodian to buy it, and the custodian holds the asset in the IRA’s name. Income and gains flow back to the IRA. You never personally touch the money or the asset.

Here is each stage in detail.

Stage 1. Open the account. You apply with an SDIRA custodian, choose Traditional or Roth, and sign the account agreement. Most custodians open the account in 1 to 3 business days. Our walkthrough on how to open a self-directed IRA covers the documentation list and what to expect.

Stage 2. Fund the account. Three paths:

- New contributions up to the annual IRS limit ($7,000 if under 50, $8,000 if 50+ for 2025). The current-year figure is in IRS Publication 590-A.

- Trustee-to-trustee transfer from another IRA. No tax. No 60-day clock. No annual cap on the number of transfers.

- Rollover from a 401(k), 403(b), or 457 plan. This is how most SDIRAs get funded. Read our complete 401(k)-to-SDIRA rollover guide, the parallel 403(b) rollover walkthrough, and our paperwork-focused 401(k) rollover guide for the step-by-step sequence. If you take possession of the funds yourself, you have 60 days to redeposit. Miss the deadline and the entire amount becomes a taxable distribution. Our 60-day rollover rule guide covers the trap.

Stage 3. Find the investment. You source the deal yourself. Your custodian does not. If you want a rental property, you find the property. If you want gold, you choose the dealer. If you want a private lending note, you negotiate the terms.

Stage 4. Direct the custodian. You submit a written buy direction with the asset details, the amount, and the wire instructions for the seller. The custodian’s job is to verify the transaction does not violate IRS rules and then execute it. The custodian does not give investment advice. FINRA’s investor alert on self-directed IRAs is worth reading because the lack of broker oversight is exactly why fraudsters target SDIRA holders.

Stage 5. The asset is held in the IRA. Title goes to the custodian for the benefit of your IRA. For a rental property, the deed reads something like “Equity Trust Company, Custodian FBO [Your Name] IRA.” All rent flows to the IRA bank account. All expenses get paid from the IRA. You cannot personally collect rent, repair the property yourself, or live in it, even one weekend. The same FBO-titled-asset structure applies to gold (custodied at an IRS-approved depository under the IRA’s name) and to crypto (custodied by the IRA’s wallet provider, with private keys held by the custodian, not by you).

The Custodian’s Role (and What They Don’t Do)

The custodian is a passive administrator. They do four things:

- Hold legal title to assets

- Process buy and sell directions you submit in writing

- Send IRS Form 5498 (contributions) and Form 1099-R (distributions)

- Refuse transactions that violate IRS rules

They do not recommend investments. They do not vet sponsors. They do not audit deal documents. They do not tell you whether something is a good idea. That is your job. The SEC’s investor bulletin on self-directed IRAs makes the same point in stronger language: SDIRA custodians are not gatekeepers, and investors should not assume they are.

There is a vocabulary issue worth flagging. The terms “custodian,” “administrator,” and “trust company” are sometimes used interchangeably, but they are not the same.

- A custodian has a federal or state trust charter and can hold IRA assets directly.

- An administrator does paperwork but does not have a trust charter, and routes assets to a separate custodian.

- A trust company is a state-chartered entity that can hold assets in trust.

For most investors the distinction does not matter operationally. It matters for due diligence: a self-described SDIRA “administrator” with no underlying custodian relationship is a red flag.

Direct (Custodial) vs. Checkbook Control

Two structures exist for executing transactions inside an SDIRA.

A direct (custodial) SDIRA routes every transaction through the custodian. You submit a buy direction. The custodian wires funds. Slower, but simpler. Best for buy-and-hold strategies where speed does not matter.

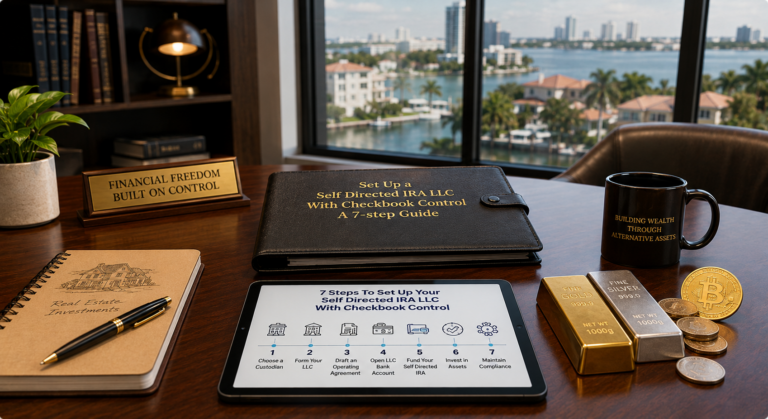

A checkbook control SDIRA has your IRA own a single-member LLC that you manage. The LLC opens its own bank account. You write checks directly from that account to fund investments. Faster execution. Lower per-transaction cost. Higher upfront setup.

Read SDIRA LLC checkbook control for the structural overview, then how to set up an SDIRA LLC with checkbook control for the operational steps. If you go this route, you will likely need an EIN. See does a self-directed IRA need an EIN in 2026.

How an SDIRA Is Taxed

An SDIRA pays tax exactly like the underlying account type:

- Traditional SDIRA. Contributions may be deductible. Growth is tax-deferred. Distributions in retirement are taxed as ordinary income. RMDs begin at age 73.

- Roth SDIRA. Contributions are after-tax. Growth is tax-free. Qualified distributions are tax-free. No RMDs during the original owner’s lifetime.

Two SDIRA-specific taxes are worth understanding before you invest:

- UBIT (Unrelated Business Income Tax) applies when the IRA owns an active trade or business inside a pass-through, such as an LLC running short-term rentals or an operating business.

- UDFI (Unrelated Debt-Financed Income) applies when the IRA buys property using a non-recourse mortgage. The portion of income attributable to the debt is taxable to the IRA.

Most investors with leveraged real estate inside an IRA owe some UDFI. Our SDIRA tax filing requirements page walks through Form 990-T mechanics: who pays it (the IRA, not you personally), when it is due, and how to estimate it before you close on a property. Form 990-T is filed in the IRA’s name. The IRA pays the tax from IRA funds. CPA preparation typically runs $500 to $2,000 per year depending on complexity.

How Distributions Work

Distributions follow standard IRA rules. Before age 59½, withdrawals trigger ordinary income tax (Traditional) plus a 10% early-withdrawal penalty unless an exception applies (first home, education, medical, disability, substantially equal periodic payments under § 72(t)). After 59½, distributions are penalty-free but still taxable for Traditional accounts. Roth distributions are tax-free if the account has been open at least five years.

For Traditional SDIRAs, RMDs begin at age 73 under SECURE 2.0. The custodian calculates the RMD based on the account’s prior-year December 31 value, which for alternative assets requires an annual fair-market-value appraisal. Roth SDIRAs do not require RMDs during the original owner’s lifetime.

The IRS publishes the full distribution rules in Publication 590-B. The IRS individual retirement arrangements (IRAs) page is the cleanest entry point.

What Can You Invest In With a Self-Directed IRA?

A self-directed IRA can hold almost any asset class. The IRS only prohibits three things by name: collectibles, life insurance, and S-corporation stock. Everything else is legal as long as the transaction does not involve a disqualified person.

Here is what investors actually use SDIRAs for, organized by asset class.

Real Estate

Real estate is the largest SDIRA asset class by dollar value. Allowed strategies include single-family rentals, multifamily, commercial property, raw land, fix-and-flip, syndications, REIT shares, tax liens, and mortgage notes.

The four mistakes that disqualify the most real estate IRAs are: living in the property even one weekend, renting it to a lineal relative (parent, child, or grandparent), doing repair work yourself, and paying yourself a management fee. All four are prohibited transactions under IRC § 4975 and result in total disqualification of the IRA. Property management must run through an unrelated third party.

Funding mechanics for IRA real estate: cash purchase from IRA funds (the cleanest path), non-recourse loan (no personal guarantee allowed; lenders typically require 30%–40% down), or syndication co-investment as a passive limited partner. Leveraged property triggers UDFI tax on the debt-financed portion of net rental income, due via Form 990-T filed by the IRA itself.

Passive structures (syndications, crowdfunding LPs, REIT shares) are friendlier inside an SDIRA because the third-party-management requirement is built into the deal. Active strategies (fix-and-flip you’d self-manage, short-term rentals you’d operate, properties you’d renovate yourself) are nearly impossible to run compliantly. The IRS does not care that you would do the work for free — sweat equity from a disqualified person is itself a prohibited transaction.

Precious Metals

Gold, silver, platinum, and palladium bullion held inside an SDIRA must meet IRS purity requirements: .995 fine for gold, .999 for silver, and .9995 for platinum and palladium. Eligible coins include American Eagle, American Buffalo, Canadian Maple Leaf, and Austrian Philharmonic. Numismatic, rare, and collectible coins are prohibited under IRC § 408(m), even when they contain eligible metal — rare US coins, foreign coins not on the IRS-approved list, and proof sets all fail the test.

Storage is non-negotiable. Physical metals owned by an IRA must be held at an IRS-approved depository. Common ones include Delaware Depository, Brink’s Global Services, Texas Bullion Depository, and IDS Group. Home storage of IRA-owned metals is treated as a constructive distribution under current IRS guidance, regardless of marketing claims by some promoters. The 2021 McNulty v. Commissioner Tax Court decision confirmed this in the context of IRA-owned LLC metal storage at home.

Cost structure for metals SDIRAs runs higher than other asset classes because depository storage layers on 0.5% to 1% of asset value per year above base custodial fees. Segregated storage (your specific bars and coins held separately, identified by serial number) costs more than commingled storage (your IRA owns a fractional claim on a pool of identical bullion).

Funding routes are identical to any other SDIRA: direct contribution up to the annual limit, trustee-to-trustee transfer from another IRA, or rollover from a 401(k), 403(b), or 457 plan. Solo 401(k) holders sometimes prefer to keep precious metals inside the solo plan rather than rolling to an SDIRA, because the solo 401(k) avoids UBIT exposure on certain leveraged transactions; that decision depends on whether the plan supports alternative-asset custody.

Cryptocurrency

Cryptocurrency inside an SDIRA is held by a specialized custodian who controls the private keys on the IRA’s behalf. You do not hold the keys yourself. Bitcoin, Ethereum, XRP, Solana, and most major coins by market cap are supported by the largest crypto IRA custodians; smaller-cap altcoins, stablecoins, and tokens vary by platform.

The Roth structure is particularly powerful for crypto. A position that 10x’s over a decade comes out completely tax-free at qualified-distribution age. The same position in a taxable brokerage account would owe long-term capital gains tax on every realized gain along the way, and the same position in a Traditional SDIRA would defer tax but ultimately be taxed as ordinary income at distribution.

Operational risks specific to crypto SDIRAs: lost private keys (the custodian carries the operational risk, but their fees price it in), exchange counterparty risk for custodians who route through public exchanges, and platform-fee structures that range from 1% to 3% per trade plus annual asset-based fees. Spreads on the same coin can vary by 2%+ between custodian platforms, so compare quotes before funding.

The ETF question matters in 2026. Spot Bitcoin and Ether ETFs approved by the SEC in 2024 can be held inside any regular brokerage IRA without an SDIRA. The reasons to choose a true crypto SDIRA over an ETF are direct ownership of the asset (you own coins, not shares of a fund), access to coins ETFs do not track, and the option to move assets to a self-custody wallet on distribution. The reasons to prefer the ETF are lower expense ratios, faster execution, and no SDIRA custodial fees.

You can mix asset classes inside one account. A single SDIRA can hold gold, silver, real estate, crypto, and private notes simultaneously provided each asset is custodied appropriately and no transaction violates the prohibited-transaction rules.

Private Equity, Lending, and Business Interests

Startup equity, angel investments, secured promissory notes, business loans, and operating-business ownership are all permitted, subject to UBIT and the prohibited-transaction rules. Operating-business income flowing into an IRA triggers UBIT on the active-business portion. See our deep guide on SDIRA business ownership rules for structuring decisions, and SDIRA loans to family: what the IRS actually allows for the family-lending rules — the area where investors most often slip into a prohibited transaction by accident.

Other Alternatives

Agricultural land. Livestock. Water rights. Oil and gas working interests. Equipment leasing. Royalty agreements. Intellectual property licenses. Most are legal under § 408 as long as no disqualified person is involved. Our overview on diversifying your retirement beyond stocks and bonds with alternative assets ties them together.

Self-Directed IRA Rules You Cannot Break

The fastest way to lose an SDIRA is a prohibited-transaction violation. The full balance gets disqualified, treated as a distribution, taxed as ordinary income, and hit with a 10% penalty if you are under 59½. The IRS publishes the rules in IRC § 4975 and IRC § 408. Our deep guide on SDIRA rules and prohibited transactions covers the operational version.

Disqualified Persons

A “disqualified person” cannot transact with your IRA. The list:

- You

- Your spouse

- Your parents and grandparents (lineal ascendants)

- Your children, grandchildren, and their spouses (lineal descendants)

- Any entity owned 50% or more by the people above

- Fiduciaries of the IRA (which includes you as the account holder)

- Any service provider to the IRA, in some cases

Notable exclusion: siblings, cousins, aunts, uncles, and in-laws are generally NOT disqualified. You can lend IRA money to your brother-in-law’s business if the rest of the deal is arm’s length. You cannot lend it to your father-in-law if you also serve as a fiduciary.

Prohibited Transactions

Any transaction between the IRA and a disqualified person is prohibited. Examples drawn from real consultations:

- Buying a property your IRA owns (self-dealing)

- Selling a property you own personally to your IRA (self-dealing)

- Renting an IRA-owned property to your daughter (lineal descendant)

- Lending IRA money to your father’s business (lineal ascendant + 50% entity)

- Doing repair work on an IRA rental yourself (services to a disqualified person)

- Living in an IRA-owned vacation property even one weekend (personal use)

- Paying yourself a management fee for IRA assets

- Pledging IRA assets as collateral for a personal loan

- Co-investing personally and via the IRA in the same deal at non-arm’s-length terms

The Three Most Common Mistakes That Disqualify a Self-Directed IRA

After consulting on hundreds of SDIRAs, three mistakes account for more than 80% of disqualifications:

- The handyman trap. Investor buys a fixer-upper inside the IRA, then spends a weekend painting it. Even unpaid sweat equity is “services to a disqualified person.” Disqualifies the IRA.

- The family rental. Investor buys a property and rents it to a child or parent at any rate, including market rate. Disqualifies the IRA.

- The personal-guarantee mortgage. Investor takes a non-recourse loan but personally signs the guarantee. Once you personally guarantee debt on an IRA asset, you have extended credit to the IRA. Disqualifies it.

The escape valve is that some violations can be unwound under DOL Voluntary Fiduciary Correction Program rules if caught early. Most cannot. Read SDIRA prohibited transactions before you do anything that even looks like it might cross a line.

What Happens If You Violate a Prohibited Transaction (and Whether You Can Fix It)

A prohibited-transaction violation disqualifies the entire IRA effective January 1 of the year the violation occurred. The full balance becomes a deemed distribution. Traditional SDIRAs owe ordinary income tax on the full balance. Roth SDIRAs that fail to meet the 5-year-and-59½ qualification rules owe income tax on earnings. The 10% early-withdrawal penalty applies if you are under 59½. There is no partial penalty. It is total disqualification.

The IRS finds these violations through three channels: routine custodian audits, Form 990-T filings that flag suspicious transactions, and field examinations of the account holder’s personal tax return. The statute of limitations on IRS assessment is generally 3 years from the date the return was filed, but extends to 6 years for substantial under-reporting (greater than 25%) and is unlimited for fraud or no-return-filed cases.

The Remediation Paths That Actually Work

Some violations can be unwound, but most cannot. The Department of Labor’s Voluntary Fiduciary Correction Program (VFCP) covers a narrow list of correctable violations, primarily lending and asset-use issues, when self-corrected and reported before IRS detection. Outside VFCP, the IRS Employee Plans Compliance Resolution System (EPCRS) provides Self-Correction (SCP), Voluntary Correction (VCP), and Audit Closing Agreement (Audit CAP) routes — but EPCRS primarily covers qualified plans, not IRAs.

For IRAs specifically, options narrow to:

- Voluntary disclosure to the IRS before audit, paying back-taxes and penalties on the disqualification but potentially avoiding fraud allegations

- Reversing the transaction before the end of the tax year (limited applicability — works for some lending and asset-use issues, not for self-dealing)

- Closing Agreement with the IRS in rare cases, negotiated through tax counsel

What Does Not Work

Backdating documents. Restructuring the LLC after the fact. Claiming the disqualified person did not “really” use the asset. Arguing the transaction was at arm’s length. The Tax Court has consistently rejected these defenses. The most-cited recent ruling is Peek v. Commissioner (T.C. 2013), which confirmed that even an indirect benefit to a disqualified person triggers full disqualification.

The Math on a Disqualification

A $400,000 Traditional SDIRA that violates a prohibited transaction triggers approximately $90,000 to $150,000 in federal income tax depending on bracket, plus state tax (typically $20,000 to $40,000), plus the 10% early-withdrawal penalty if applicable ($40,000), plus potential accuracy-related penalties of 20% on the underpayment. Total exposure on a $400K disqualification is realistically $150,000 to $260,000 — and the IRA itself is gone.

If you suspect you may have committed a prohibited transaction, do not wait. The remediation window is narrow, and the cost of waiting is the difference between a survivable mistake and a six-figure disaster. Talk to an ERISA attorney or qualified CPA before doing anything else, and review our SDIRA rules and prohibited transactions guide to confirm whether the transaction in question actually crosses the line.

How Much Does a Self-Directed IRA Cost?

Expect $200 to $500 per year in base custodial fees for most accounts, plus a per-asset fee of $30 to $300 per year per asset held, plus a per-transaction fee of $30 to $150 per buy or sell. Real estate accounts and crypto accounts run higher. Bullion accounts include depository storage fees on top, typically 0.5% to 1% of asset value per year.

| Cost component | Typical range | Notes |

| Account opening | $0 to $100 | One-time |

| Annual base fee | $200 to $500 | Some custodians use a sliding scale based on account value |

| Per-asset annual fee | $30 to $300 per asset | Real estate and private equity at the high end |

| Per-transaction fee | $30 to $150 | Each buy, sell, wire, or paperwork item |

| Depository storage (metals) | 0.5% to 1% of asset value per year | Segregated storage costs more than commingled |

| Checkbook LLC setup | $1,000 to $3,000 | One-time, plus state filing fees ($50 to $800) |

| Annual LLC state fees | $50 to $800 | Varies by state |

| Form 990-T preparation | $500 to $2,000 per year | Only if UBIT or UDFI applies |

The rule of thumb: if your IRA is below $25,000 and you only want index funds, an SDIRA does not pay for itself. If your IRA is $50,000+ and you want even one alternative asset, the math works.

Benefits of a Self-Directed IRA

A self-directed IRA gives you four advantages that no brokerage IRA can match.

Investment universe. Real estate, metals, crypto, private equity, notes, syndications, tax liens, and hundreds of other categories. The same tax wrapper that limits you to the brokerage menu in a regular IRA puts almost nothing off-limits in an SDIRA.

Diversification beyond market beta. Stocks and bonds are correlated to each other and to broader market sentiment. Real estate, metals, and private credit move on different cycles. An SDIRA is the only retirement account that lets you express that diversification with retirement dollars.

Roth power for high-appreciation assets. Putting a 10x crypto position or a high-appreciation rental property inside a Roth SDIRA means decades of growth come out tax-free at retirement. The same position outside a Roth gets taxed at long-term capital gains every time you rebalance.

Inflation hedge. Physical metals and real estate have historically tracked inflation better than nominal bonds. Holding them inside a tax-advantaged account compounds the benefit.

The case for self-directing is summarized in our long-form post on unlocking self-directed retirement accounts and the practical version in diversifying retirement beyond stocks and bonds.

Self-Directed IRA Risks and Drawbacks

Higher fees. More complexity. No advisor. Higher fraud risk. Liquidity issues. A prohibited-transaction trap that can disqualify the entire account. SDIRAs are not for everyone, and the SEC and FINRA both publish investor alerts on them for good reason.

Fees. Already covered above. Expect $500+ per year of base custodial cost on a meaningful account.

Complexity. You are responsible for compliance, valuation, and transaction sequencing. The custodian will not catch your mistakes.

No advice. A brokerage advisor can be sued for unsuitable recommendations. An SDIRA custodian cannot, because they did not give a recommendation. You are on your own for due diligence.

Fraud. SDIRAs are a frequent target for investment fraud. The FINRA SDIRA fraud alert covers the patterns, and the SEC SDIRA investor bulletin lists the red flags. The most common con is a “guaranteed return” alternative investment promoted to IRA holders specifically because the custodian will not push back on the deal.

Liquidity. A rental property or private note cannot be sold in a day. RMDs at 73 can become difficult to fund if your assets are illiquid.

The disqualification trap. Already covered above. One mistake can cost the entire IRA.

The honest answer to whether the trade-off is worth it is in our piece on whether a self-directed IRA is a good idea.

Common Self-Directed IRA Scams and Red Flags

SDIRAs are a frequent target for investment fraud because the custodian is a passive administrator. They do not vet your investments. They do not verify the seller. They do not check whether returns are real. Fraudsters know this and design pitches specifically for IRA money. The SEC’s Office of Investor Education has flagged SDIRA fraud as a top-10 enforcement priority since 2013.

The most common patterns:

The “Guaranteed Return” Alternative Investment

Promoter pitches a private placement, real estate fund, or note program with promised returns of 8% to 25% annually. The pitch usually includes the phrase “self-directed IRA approved” — a meaningless designation no custodian actually grants. Real investments do not guarantee returns. SEC-registered investments cannot legally promise specific returns. If you hear “guaranteed,” the conversation is over.

The Home-Storage Gold IRA

Promoter sells you precious metals at marked-up prices and tells you that an LLC structure lets you store the metals at home. The 2021 McNulty v. Commissioner Tax Court decision ruled this is a constructive distribution, taxable in full plus penalties. The promoter knows. The buyer usually does not. Any pitch that pairs “home storage” with “IRA-owned gold” is a red flag.

The Promoter-as-Asset-Seller Conflict

Same firm that recommends the SDIRA structure also sells you the asset (a property, a private fund, a coin program). They earn commission on the asset sale, which is why they are recommending the structure. If the asset underperforms, the IRA pays. If it implodes, you lose the IRA and the seller keeps the commission. Always verify the seller is independent of the SDIRA referrer.

The Unregistered Private Placement

Promoter pitches a real estate fund, oil-and-gas program, or startup using a Reg D offering that turns out not to be properly registered or exempted. The SEC’s Form D lookup at sec.gov can verify a real Reg D filing in 30 seconds. Most fraud cases involve no Form D filing at all. Always confirm before investing.

The Affinity-Fraud SDIRA Syndicate

Promoter targets a specific community (church group, professional society, ethnic community, retiree association) with a pitch that “everyone is doing this.” Returns are paid out of new investor money in a Ponzi structure. When inflows stop, the scheme collapses. The custodian will not catch this. The SEC’s investor alerts on affinity fraud apply directly.

The Offshore “Tax-Free” Pitch

Promoter recommends moving SDIRA assets offshore to “avoid US tax.” This is not a thing. SDIRAs are subject to US tax wherever the assets are held. FBAR and FATCA reporting still apply. The pitch is either fraud or willful tax evasion advice; both can land the account holder in IRS enforcement.

The Fake Checkbook-LLC Promoter

Sells you a “checkbook control” package without setting up a properly chartered IRA-owned LLC. Sometimes the LLC ends up owned personally instead of by the IRA, which is itself a prohibited transaction. Verify the LLC’s operating agreement, member, and bank account titling all read “FBO [Your Name] IRA.”

Red Flags That Should End the Conversation

Any of the following should make you walk away immediately:

- Promised or “expected” returns above 12% on a fixed-income product

- “Limited time” pressure to commit by a specific date

- Pitch references that the investment is “approved” by the IRS or a custodian (custodians do not approve investments)

- Seller is the same party that recommended the SDIRA

- No audited financials on the underlying investment

- No SEC Form D filing for a private placement

- Promoter resists answering whether returns have ever been paid out, or sends only “statements” instead of bank records

- Investment requires moving assets to a custodian you have never heard of and cannot verify with state regulators

If you suspect fraud, report to the SEC Office of Investor Education and Advocacy, your state securities regulator, and FINRA. The IRS does not handle investment fraud directly, but reporting to them protects you on the tax side if the IRA is later disqualified.

How to Open a Self-Directed IRA in 2026 (Step-by-Step)

Opening an SDIRA takes 1 to 4 weeks depending on whether you are funding with new contributions (fast) or rolling over a 401(k) (slow, depends on the old plan administrator). Here is the actual sequence.

Step 1. Decide Roth or Traditional. If you expect to be in a higher tax bracket in retirement or you are buying assets you expect to appreciate significantly (real estate, crypto), Roth usually wins. If you need the deduction now and expect lower retirement income, Traditional. Our SDIRA vs. Roth IRA comparison walks through the decision with examples.

Step 2. Choose your custodian. Match the custodian to the asset class. Real estate investors need a custodian that processes deeds quickly. Crypto investors need one integrated with a regulated exchange. Precious metals investors need a custodian connected to an IRS-approved depository. Our 2026 SDIRA custodian comparison ranks the major players by asset specialization and fee structure, and our checklist on how to determine the best self-directed IRA custodian for your investment goals covers the questions to ask before signing.

Step 3. Decide on direct vs. checkbook control. Direct (custodial) for buy-and-hold simplicity. Checkbook control for speed and lower per-transaction cost. The structural overview is in SDIRA LLC checkbook control, and the operational steps are in how to set up an SDIRA LLC with checkbook control.

Step 4. Fund the account. Submit transfer or rollover paperwork. Trustee-to-trustee transfers from another IRA take 5 to 10 business days. 401(k) rollovers usually take 2 to 4 weeks because the old plan administrator processes the distribution.

Step 5. Direct your first investment. Submit the buy direction in writing. The custodian executes. The asset is now held in your IRA’s name.

Step 6. Annual reporting. Your custodian files Form 5498 (contributions and fair market value) and Form 1099-R (distributions). If your IRA owes UBIT or UDFI, you are responsible for filing Form 990-T on the IRA’s behalf. The IRA pays the tax from IRA funds, not from your personal funds.

How to Vet a Self-Directed IRA Custodian Before You Sign

A custodian holds your IRA assets, processes your transactions, and reports to the IRS on your behalf. Pick badly and you will spend years fighting paperwork delays, paying surprise fees, or worse — discovering the firm was undercapitalized. Vetting takes one afternoon and prevents most of the problems SDIRA holders complain about. Use this checklist alongside our 2026 best SDIRA custodian comparison and our questions-to-ask checklist.

Step 1. Verify the Trust Charter

Every legitimate SDIRA custodian holds either a state trust charter or a federal trust charter under the OCC. Search the firm at the National Information Center (nic.gov) and your state’s Department of Banking or Department of Financial Institutions. If the firm is not in either database, it is not a custodian — it is at most an administrator routing assets to a separate custodian. That is not automatically a problem, but you need to know.

Step 2. Verify Financial Strength

Trust companies are required to maintain minimum capital reserves. Public financial statements should be available on request. Ask for the firm’s most recent audited financials and look at three things: capital reserves, AUM trends (declining AUM is a warning sign), and any going-concern language in the auditor’s opinion. A firm that hesitates to share audited financials is telling you something.

Step 3. Check Regulatory History

Search your state banking department’s enforcement-action database. Cross-reference the firm at the SEC IAPD database (advisorinfo.sec.gov) if they offer any advisory products. Check FINRA BrokerCheck for any associated reps. Pull the Better Business Bureau record for complaint volume and resolution rate. A firm with 50+ unresolved BBB complaints in 12 months is a signal regardless of star rating.

Step 4. Read the Fee Schedule Line by Line

Bring three things to a comparison: the all-in annual cost on your expected portfolio size, the per-transaction fee structure (flat or percentage), and the wire/distribution/termination fees. Termination fees are the trap — some custodians charge $250 to $1,000 to close an account or transfer assets out. If you may want to switch later, that fee determines your switching cost.

Step 5. Time-Test Their Operations

Call the support line. Time how long you wait. Email their compliance team with a complex hypothetical question (for example, “can my IRA invest as a passive limited partner in a syndication where my brother-in-law is a co-general partner?”). Time the response. If a custodian takes 3 weeks to answer a hypothetical, they will take 6 weeks to clear your real estate closing.

Step 6. Confirm Asset-Class Specialization

Ask specifically: how many real estate transactions did you process last year? How many crypto trades? How many wire-transfer-out events for metals delivery? Custodians that handle 100 real estate closings a year process them faster than custodians that handle 5. Match the firm’s specialty to your strategy. A generalist custodian rarely beats a specialist on speed for any specific asset class.

Step 7. Get the Operating Agreement Template

If you plan to set up a checkbook-LLC structure, ask the custodian which operating agreement template they require. Some custodians reject LLC structures their compliance team did not pre-approve. Confirm before paying for an LLC formation. Mismatched templates can delay funding for 60+ days.

Questions to Ask Before You Sign

- What is the all-in annual cost for an account of my size with my asset mix?

- What are the per-transaction fees, by transaction type?

- What is the termination fee?

- What is your typical time-to-close for real estate / crypto / metals transactions?

- Do you carry insurance on uninvested cash balances?

- Are you a custodian or an administrator? If administrator, who is the underlying custodian?

- Has the firm had any regulatory enforcement actions in the last 5 years?

- Will you provide audited financials?

- How do you handle FMV reporting on non-public assets?

- What is your process if a transaction direction may violate IRS rules — do you reject it, ask for clarification, or process and let the IRS sort it out?

A custodian that answers every question without hesitation, in writing, is the right custodian.

Annual Operations: Valuations, FMV Reporting, and RMDs on Illiquid Assets

Owning alternative assets in an IRA creates an operational reality that brokerages do not have to deal with. Every December 31, your IRA needs a fair-market value for every asset it owns. The custodian must report it to the IRS on Form 5498 by May 31 of the following year. For Traditional SDIRA holders age 73+, that FMV also drives the annual Required Minimum Distribution calculation.

Who Provides the Valuation

The valuation source depends on the asset:

- Publicly traded assets (stocks, ETFs held inside the SDIRA): the custodian pulls the year-end close.

- Precious metals: the depository or custodian pulls the spot close from a major exchange (typically COMEX for gold and silver, NYMEX for platinum and palladium).

- Cryptocurrency: the custodian pulls the year-end close from the exchange or wallet provider.

- Real estate: a licensed appraiser, a broker price opinion (BPO) from a licensed real estate broker, or a comparable-market-analysis report. Cost: $300 to $1,500 per property per year. Some custodians accept self-reported FMV from the account holder, but this raises audit risk.

- Private equity and private notes: most custodians require either a third-party valuation, the issuer’s most recent statement of value, or a CPA-prepared FMV memo. Private notes are typically valued at outstanding principal balance plus accrued interest unless impaired.

- Operating businesses and LLC interests: business valuation, typically $1,500 to $5,000 per year.

The Under-Reporting and Over-Reporting Trap

If the custodian reports a low FMV and the IRS later determines the asset was worth more, the difference can become a deemed distribution in earlier years (back-taxes plus interest plus penalties). If the FMV is over-reported, the IRA pays inflated RMDs, generating forced taxable distributions on phantom value. Both are expensive. Get the valuation from a credible source and document the methodology.

RMDs When Assets Are Illiquid

Traditional SDIRA holders must take RMDs starting at age 73. The RMD amount is calculated as December 31 prior-year FMV divided by an IRS life-expectancy factor (Uniform Lifetime Table for most account holders).

If your IRA owns a single rental property worth $500,000 and has $5,000 of cash, your RMD might be $19,500 — and you have only $5,000 of liquidity. Three options:

- Distribute cash first, partial each year, until cash is exhausted. Buys time to plan a liquidity event.

- Take an in-kind distribution of a partial interest in the property (a tenants-in-common interest equal to the RMD value). The custodian deeds out a fractional ownership stake. Complex, expensive, but legal.

- Sell a portion of the asset to generate cash. Forces a transaction at whatever the market is on RMD-deadline day.

The right answer is to plan ahead. By age 70, start positioning the IRA toward a 10% to 20% liquidity buffer to absorb 5 years of RMDs without forced sales.

Roth SDIRAs avoid the RMD problem entirely during the original owner’s lifetime, which is one of the strongest planning arguments for Roth conversion of alternative-asset SDIRAs in your 60s. Walk through the decision with our SDIRA vs. Roth IRA comparison.

The Annual Compliance Calendar

| Date | Item |

| January 31 | Custodian sends Form 1099-R for prior-year distributions |

| April 15 | Form 990-T due if IRA owed UBIT or UDFI for prior year |

| April 15 | Last day to make prior-year contributions |

| May 31 | Custodian files Form 5498 (contributions and Dec 31 FMV) |

| October 15 | Extended Form 990-T deadline |

| December 31 | Year-end FMV snapshot date |

| December 31 | RMD deadline (Traditional SDIRA, age 73+) |

A clean operations year takes about 6 hours of the account holder’s time, mostly gathering FMV documentation. A messy year, with audits or missed RMDs, can cost $5,000 to $50,000 to clean up. Our SDIRA tax filing requirements page covers Form 990-T mechanics in depth.

Self-Directed IRA Exit Strategies: How to Distribute Alternative Assets

Funding an SDIRA is easier than exiting one. The exit is where most investors get surprised by tax bills and operational friction. Plan the exit before you make the entry.

The Four Exit Paths

1. Liquidation distribution. The asset is sold inside the IRA, the proceeds become cash, and the cash is distributed to the account holder. Standard process. Works for any asset. The IRA pays no tax on the sale itself (the sale happens inside the wrapper). The account holder pays ordinary income tax on the distribution amount (Traditional) or nothing if qualified (Roth).

2. In-kind distribution. The asset itself is distributed to the account holder. The custodian deeds the property out, ships the gold from the depository, or transfers the crypto to a personal wallet. The IRA reports the fair-market value at distribution date as a taxable distribution. The account holder receives a cost basis equal to that FMV for future tax purposes. For Roth SDIRAs that are qualified, the in-kind distribution is tax-free and the asset transfers with no income tax consequences.

3. Roth conversion. Convert a Traditional SDIRA holding to a Roth SDIRA. The conversion amount equals the FMV on conversion date and is taxable as ordinary income that year. Future growth and qualified distributions are tax-free. For high-appreciation assets like real estate or crypto, this is often the highest-value move available — converting at a depressed FMV (a temporary market dip) locks in lower tax cost while leaving the upside in the Roth.

4. Beneficiary inheritance. The asset stays inside the IRA and passes to named beneficiaries, who follow the post-SECURE-Act 10-year distribution rule. Covered in detail below.

In-Kind Distribution Mechanics

For a rental property, the custodian executes a deed transfer from “Custodian FBO IRA” to the account holder’s personal name, files the deed at the county recorder, and reports the FMV as a distribution to the IRS on Form 1099-R. Title insurance, recording fees, and any transfer tax are paid by the IRA before distribution (or by the account holder personally if the IRA lacks cash).

For physical metals, the depository releases the bullion to a delivery service (Brink’s or Loomis typically) shipping to the account holder’s address. The IRA reports FMV as of distribution date. Insured transit cost ($150 to $500 per shipment) is paid by the IRA.

For cryptocurrency, the custodian transfers coins from the IRA’s custodial wallet to the account holder’s personal wallet. The IRA reports FMV at the timestamp of transfer.

Tax Timing

Distribution-date FMV is what gets reported. If you take a property worth $400,000 on December 15 and the market drops to $370,000 in January, you owe ordinary income tax on the $400,000 — not the $370,000. If you can choose distribution timing, choose a year your other income is lower (sabbatical year, low-bonus year, retirement transition year). For Roth SDIRAs, timing does not matter — qualified distributions are tax-free regardless.

The Roth-Conversion Strategy for Alternative Assets

Real estate that you expect to appreciate from $300,000 to $1,000,000 over 20 years generates $700,000 of growth. Inside a Traditional SDIRA, that growth is taxed at distribution (potentially $250,000+ in federal tax). Inside a Roth SDIRA, that growth is tax-free.

Converting at the $300,000 FMV costs $60,000 to $90,000 in current-year ordinary income tax, depending on bracket. Compared to $250,000+ down the road, the conversion is the obvious move — provided you have outside (non-IRA) cash to pay the conversion tax bill. Paying the tax with IRA money is itself a partial distribution and triggers more tax.

Time conversions during years your other income is low and during periods when the asset’s FMV is depressed (a soft real estate market, a crypto bear market). The 2017 Tax Cuts and Jobs Act eliminated most Roth recharacterizations, so once you convert, it is permanent.

Inherited Self-Directed IRA Rules: Beneficiaries and the 10-Year Rule

The SECURE Act of 2019 fundamentally rewrote inherited IRA rules. The “stretch IRA” (a non-spouse beneficiary stretching distributions over their own life expectancy) is gone for most inheritors. The replacement is a 10-year forced-liquidation rule that hits SDIRA beneficiaries especially hard because alternative assets are not always sellable on demand.

Who Is Affected

Non-spouse beneficiaries who inherited an IRA after January 1, 2020. The rule applies to all IRAs (Traditional and Roth), including SDIRAs. Spouse beneficiaries are exempt and can roll the inherited IRA into their own IRA.

A small set of “eligible designated beneficiaries” can still use the stretch:

- Surviving spouse

- Minor children of the original account holder (until age of majority, then the 10-year rule begins)

- Disabled or chronically ill beneficiaries

- Beneficiaries less than 10 years younger than the original account holder

The 10-Year Rule

The entire inherited IRA must be distributed by December 31 of the 10th year following the year of the original owner’s death. Under SECURE 2.0 (2022) and the IRS’s 2024 final regulations, beneficiaries of accounts where the original owner had already started RMDs must also take annual RMDs during years 1 through 9 of the 10-year window (this was contested for several years; the 2024 final regs settled it).

Beneficiaries of accounts where the original owner died before reaching their RMD age can wait and distribute everything in year 10.

Why the 10-Year Rule Is Brutal for SDIRA Assets

A $600,000 inherited Traditional SDIRA holding a single rental property worth $580,000 forces the beneficiary to liquidate or distribute that property within 10 years. They cannot stretch over their lifetime. They cannot keep the property indefinitely inside the inherited IRA.

Three paths:

- Sell the property inside the IRA, distribute cash over 10 years. Forces a sale at whatever the market is in year 10 if not earlier.

- Take in-kind distributions of fractional ownership. Custodian deeds out a tenants-in-common interest each year. By year 10, the IRA has zero ownership and the beneficiary owns the property outright with a cost basis equal to cumulative distributed FMVs.

- Convert the inherited Traditional IRA to a Roth at the time of inheritance. Not allowed. Inherited Traditional IRAs cannot be converted to Roth (this is a common confusion). The 10-year rule applies as a Traditional account.

Step-Up in Basis (or Lack Thereof)

Assets owned personally at death receive a step-up in cost basis to FMV on date of death. Assets inside an IRA do not. The inheritor of a $500,000 rental property held personally by the decedent inherits with a $500,000 cost basis and could sell at $500,000 with zero capital gains. The same property inside an inherited Traditional SDIRA, when distributed, generates $500,000 of ordinary income to the inheritor — and no step-up. This is one of the strongest arguments to keep highly-appreciated alternative assets outside an IRA when estate planning is the primary goal.

Roth Inherited IRAs

Inherited Roth SDIRAs are still subject to the 10-year rule, but distributions are tax-free if the original Roth was qualified (5 years and 59½ on the original owner). For a Roth SDIRA holding crypto or real estate, the inheritor gets 10 years of continued tax-free growth, then distributes the asset (cash or in-kind) tax-free.

Trust-as-Beneficiary Issues

Naming a trust as the IRA beneficiary requires the trust to qualify as a “see-through trust” under IRS regulations. Conduit trusts pass distributions to beneficiaries when received. Accumulation trusts allow the trust to retain distributions. The 10-year rule applies based on the trust’s classification and the underlying beneficiaries. This is a tax-attorney decision, not a DIY one.

Beneficiary IRA Mechanics

The custodian retitles the account from “[Original Owner] SDIRA” to “[Original Owner] SDIRA, FBO [Beneficiary] as Beneficiary.” Beneficiaries cannot contribute to inherited IRAs. The 10-year clock starts in the year following the original owner’s death. RMDs (if applicable) follow the beneficiary’s life-expectancy table for years 1 through 9, with full liquidation by year 10.

If you are an SDIRA holder, name beneficiaries explicitly on the custodian’s beneficiary form — not just in your will. The beneficiary form supersedes the will for IRA assets in every state.

Self-Directed IRA vs. Other Retirement Accounts

Where does an SDIRA fit relative to every other retirement structure?

| Account | 2025 contribution limit | Roth option | Alternative assets allowed | Notes |

| Traditional IRA at brokerage | $7,000 / $8,000 | No (separate Roth) | No (effectively) | Stocks, bonds, ETFs, mutual funds |

| Roth IRA at brokerage | $7,000 / $8,000 | Yes | No (effectively) | Tax-free growth |

| Self-Directed IRA | $7,000 / $8,000 | Yes | Yes | Real estate, metals, crypto, etc. |

| 401(k) | $23,000 / $30,500 | Yes (Roth 401(k)) | No (employer-limited menu) | Employer match available |

| Solo 401(k) | $69,000 (combined) | Yes | Yes (with self-directed solo 401(k)) | Self-employed only |

| SEP IRA | 25% of compensation up to $69,000 | No | Yes (with self-directed SEP) | Self-employed and small business |

| SIMPLE IRA | $16,000 / $19,500 | Yes (Roth SIMPLE under SECURE 2.0) | Limited | Small business |

The detailed comparisons we run on the site:

Who Should (and Shouldn’t) Open a Self-Directed IRA?

A self-directed IRA is the right tool when three conditions are true:

- You want exposure to an asset class your brokerage will not custody (real estate, metals, crypto, private equity, notes).

- Your account balance is large enough that custodian fees do not eat the return (generally $25,000+ to make the fee math work, $50,000+ to feel comfortable).

- You are willing to do your own due diligence on every investment, because the custodian will not.

It is the wrong tool when any of the following apply:

- You only plan to hold index funds. (Stay at a brokerage.)

- You are uncomfortable with paperwork or do not want to review prohibited-transaction rules. (Stay at a brokerage.)

- Your account balance is under $10,000. (Custodian fees will dominate.)

- You want investment advice from your custodian. (They are not allowed to give it.)

- You are likely to want personal use of an asset (a vacation property you might stay in, a coin you want to hold). (Buy it personally instead.)

The honest decision-tree version is in is a self-directed IRA a good idea.

Self-Directed IRA Glossary

The terminology that confuses most SDIRA investors, defined in 50 words or less. Each term is a self-contained passage you can lift directly into a question or share with a co-investor.

Administrator. A firm that handles SDIRA paperwork but does not have a trust charter and does not custody assets directly. Administrators route assets to a separate custodian. Not a problem in itself, but you should know the structure before signing any paperwork or wire-transfer authorization.

Checkbook control. A structure where your IRA owns a single-member LLC that you manage. You write checks directly from the LLC’s bank account to fund investments. Faster execution, lower per-transaction fees, higher upfront setup cost ($1,000 to $3,000).

Custodian. A non-bank trust company chartered to hold IRA assets directly. Distinct from an administrator. Examples include Equity Trust Company, Madison Trust, Kingdom Trust, Strata Trust Company, and IRA Financial Trust. Holds title to your IRA’s assets in the IRA’s name.

Depository. An IRS-approved storage facility where physical metals owned by an IRA must be held. Major depositories include Delaware Depository, Brink’s Global Services, Texas Bullion Depository, and IDS Group. Home storage of IRA-owned metals is not permitted.

Disqualified person. A person or entity whose transactions with your IRA are prohibited under IRC § 4975. Includes you, your spouse, your parents, grandparents, children, grandchildren, their spouses, and any business owned 50% or more by these people. Siblings, cousins, and in-laws are not disqualified.

ERISA. The Employee Retirement Income Security Act of 1974, the federal law that created IRAs and 401(k)s. ERISA permits IRAs to invest in alternative assets, which is the legal foundation of self-directed IRAs and the entire SDIRA industry.

Fair Market Value (FMV). The price an asset would sell for in an arm’s-length transaction on a specific date. SDIRAs must report year-end FMV every December 31. For non-public assets, FMV requires an independent appraisal or comparable valuation costing $300 to $5,000 annually.

FBO. “For the Benefit Of.” Asset titles inside an SDIRA read like “[Custodian] FBO [Account Holder] IRA” — meaning the custodian holds legal title for the benefit of the IRA owner. The deed, certificate, or wallet is FBO-titled, never in the account holder’s personal name.

Fiduciary. A person who has authority over IRA investment decisions. The account holder is a fiduciary. Some service providers can become fiduciaries depending on their role. Fiduciaries are disqualified persons under IRC § 4975 and cannot transact with the IRA they oversee.

In-kind distribution. Distributing the asset itself to the account holder instead of selling the asset and distributing cash. The IRA reports the FMV at distribution date as a taxable distribution. Common for real estate, metals, and crypto exits when the holder wants to retain the asset personally.

IRC § 408. The Internal Revenue Code section that governs IRAs. § 408(m) lists prohibited collectibles. § 408(a)(3) requires a custodian. Most SDIRA structural rules trace to § 408. The section is the legal basis for which assets an IRA can and cannot hold.

IRC § 4975. The Internal Revenue Code section that defines prohibited transactions and disqualified persons. The single most important statutory reference for SDIRA compliance. Violating § 4975 disqualifies the entire IRA on January 1 of the year of violation, with no partial penalty.

Non-recourse loan. A loan where the lender’s only remedy in default is the IRA-owned collateral asset. The borrower (the IRA) does not personally guarantee the debt. Required for IRAs that take on debt because personal guarantees would be prohibited transactions. Typical down payment is 30% to 40%.

Prohibited transaction. Any transaction between the IRA and a disqualified person under IRC § 4975. Triggers full disqualification of the IRA. Examples: buying from yourself, lending to your parent, providing services to IRA-owned property, paying yourself a management fee, living in an IRA-owned property.

Roth IRA. A tax structure where contributions are after-tax, growth is tax-free, qualified distributions are tax-free, and no RMDs apply during the original owner’s lifetime. A Roth SDIRA combines Roth tax treatment with alternative-asset custody for tax-free growth on real estate, crypto, or metals.

RMD (Required Minimum Distribution). Annual withdrawal Traditional IRA holders must take starting at age 73 under SECURE 2.0. Calculated as prior-year December 31 FMV divided by an IRS life-expectancy factor. RMDs do not apply to Roth IRAs during the original owner’s lifetime, only after inheritance.

Self-Directed IRA (SDIRA). A Traditional or Roth IRA held at a custodian that accepts alternative assets (real estate, metals, crypto, private equity, notes, syndications). Same tax treatment as a regular IRA. Different custodian. Different asset universe. Different cost structure. Same contribution limits.

SECURE Act / SECURE 2.0. The Setting Every Community Up for Retirement Enhancement Act of 2019 and SECURE 2.0 of 2022. Together, they raised the RMD age to 73 (eventually 75), eliminated the stretch IRA for most non-spouse beneficiaries, and created the 10-year inherited-IRA distribution rule.

Trust company. A state-chartered or federally chartered entity authorized to hold assets in trust on behalf of others. Most SDIRA custodians are state-chartered trust companies regulated by their state’s banking department, with a small number federally chartered under the Office of the Comptroller of the Currency.

UBIT (Unrelated Business Income Tax). Tax on active-business income earned inside an IRA. Applies when the IRA owns an operating business or a pass-through entity with active income. Filed by the IRA on Form 990-T, paid from IRA funds. Most passive investments do not trigger UBIT.

UDFI (Unrelated Debt-Financed Income). A subset of UBIT that applies to income from debt-financed property. Most commonly hits IRAs that own rental property purchased with non-recourse mortgages. The portion of net rental income attributable to the debt is taxable to the IRA, even inside a Roth SDIRA.

Voluntary Fiduciary Correction Program (VFCP). A Department of Labor program that allows correction of certain prohibited transactions before IRS detection. Narrow applicability — covers a specific list of violations, not all of them. Self-correction must be made before the IRS opens an audit. Often used in conjunction with ERISA counsel.

Key Takeaways

- A self-directed IRA is a Traditional or Roth IRA at a specialized custodian that holds alternative assets.

- The tax treatment, contribution limits, and RMD rules are identical to a regular IRA.

- The differences are who custodies the account, what assets it can hold, and who decides what to buy.

- You direct every investment. The custodian executes. The custodian does not advise.

- Allowed: real estate, precious metals, crypto, private equity, notes, syndications, tax liens, and most other legal asset classes.

- Prohibited: collectibles, life insurance, S-corp stock, and any transaction with a disqualified person (you, spouse, parents, kids, or any business they control).

- Annual cost runs $200 to $500 plus per-asset and per-transaction fees. Worth it for alternative assets. Not worth it for index funds.

- Roth SDIRAs are particularly powerful for high-appreciation assets (real estate, crypto) because growth is tax-free.

- The single biggest risk is a prohibited-transaction violation, which disqualifies the entire account.

- Suggested reading order if you are starting from zero: unlocking self-directed retirement accounts → is an SDIRA a good idea → how to open one → best custodian for your asset class → asset-specific guide of your choice.

FAQ's

Can I move my 401(k) to a self-directed IRA?

Yes. Most 401(k) plans allow rollovers after you leave the employer. Some allow in-service rollovers after age 59½. Use a direct trustee-to-trustee transfer to avoid the 60-day clock. Walkthrough: 401(k) rollover to a self-directed IRA.

How much does it cost to set up a self-directed IRA?

Account opening: $0 to $100. Annual custodian fee: $200 to $500 base, plus $30 to $300 per asset, plus $30 to $150 per transaction. Checkbook control LLC adds $1,000 to $3,000 in setup costs plus state filing fees ($50 to $800).

Can I put my house in a self-directed IRA?

No. Putting a property you already own personally into your IRA would be a prohibited self-dealing transaction. The IRA can only buy properties from unrelated parties.

Is a self-directed IRA better than a 401(k)?

They are different tools. A 401(k) gives higher contribution limits ($23,000 for 2025, $30,500 with catch-up) and potential employer match. An SDIRA gives broader investment choice. Many investors use both. See SDIRA vs. 401(k).

Do I need an EIN for a self-directed IRA?

Only if you use a checkbook control LLC, or if your IRA owes UBIT or UDFI and needs to file Form 990-T. See does a self-directed IRA need an EIN in 2026.

What transactions are prohibited in a self-directed IRA?

Any transaction between the IRA and a disqualified person. Buying from yourself, selling to your spouse, lending to your parents, providing services to IRA assets, using IRA assets personally. Full list in SDIRA prohibited transactions.

How much can I contribute to a self-directed IRA?

The IRS sets the limit annually. For 2025: $7,000 if under 50, $8,000 if 50 or older. Same as a regular IRA. Check IRS Publication 590-A for the current year.

Item #8Can a self-directed IRA loan money?

Yes, to non-disqualified persons or businesses, secured by collateral or unsecured. The IRA can be the lender on private mortgages, business loans, and personal loans to non-family members. Family lending is the area investors most often slip into a prohibited transaction by accident; see SDIRA loans to family: what the IRS actually allows for the rules.

Who regulates self-directed IRA custodians?

SDIRA custodians are non-bank trust companies regulated under IRC § 408 by the IRS, and most are state-chartered trust companies (or federally chartered under the OCC). They are not regulated by the SEC because they do not give investment advice. The FINRA SDIRA alert and SEC investor bulletin cover the regulatory gap.

What is a self-directed IRA custodian?

A non-bank trust company that holds title to alternative assets on behalf of your IRA. They process paperwork, file IRS forms, and refuse transactions that violate the rules. They do not give advice. Comparison: best SDIRA custodian 2026.

What is a self-directed IRA LLC?

An LLC owned by the IRA, used to give the account holder checkbook control over investments. Setup details: set up a self-directed IRA LLC with checkbook control.

What is the best self-directed IRA company?

There is no single best. Match the custodian to the asset class. Equity Trust and Madison Trust are large generalists. Kingdom Trust is strong on crypto. Strata is strong on real estate. Read best SDIRA custodian 2026 and how to determine the best SDIRA custodian for your goals.

Have Questions About Your Self-Directed IRA?

Schedule a free 30-minute consultation with Bullionite Asset Group. No pitch, no pressure, no referral commissions.

As the Founder and Chief Investment Officer of Bullionite and Bullionite Asset Group, I’ve built my career on a simple premise understanding the intersection of macroeconomics, commodities, and digital assets to stay ahead of the curve, not under it. My focus is on navigating the complexities of the world’s largest markets spanning the US, the Middle East, and Asia to identify high-value opportunities for alternative investment.

With a specialized focus on Self-Directed IRAs (SDIRAs), I help investors move beyond traditional 401ks by integrating assets like precious metals and cryptocurrency into their retirement strategies. Based in Newport Beach, California, I am dedicated to bridging the gap between traditional finance and the evolving landscape of new age digital assets, ensuring that every strategic move is backed by deep market insight and a commitment to long-term growth.